Economists warn that the finance ministry’s projected gross domestic product (GDP) growth of 6.3% to 6.8% for FY26 could come under pressure as global headwinds, rising geopolitical tensions, volatile capital flows, trade disruptions and weak private investment intensify.

On the domestic front, India must address challenges in private sector investment and weak urban demand.

Trump’s tariffs hit export-heavy Asian economies like China and Vietnam harder than India, which leans more on domestic consumption.

Also read: CBDT probes crypto-related tax evasion

Still, headwinds at home led chief economic advisor V. Anantha Nageswaran to urge India Inc. in February to step up domestic investment to sustain long-term growth.

Reviving demand

While benign inflation and a manageable current account deficit have been a buffer against global headwinds, economists said sustaining momentum will require deeper demand-side support and a sharper pickup in private capital spending.

Devendra Kumar Pant, chief economist at India Ratings & Research, said private sector investment will pick up once demand is broadly revived.

“Earlier, rural demand was an issue, but in the last year, urban demand has been struggling. On top of it, sluggish global demand makes it difficult for across-the-board demand and thus investment revival,” he added.

A recent report by Axis Securities stated that fast-moving consumer goods (FMCG) companies reported a muted performance in Q4 FY25 due to continued weakness in the urban market, subdued demand environment and increased competition.

Also read: What 16th Finance Commission’s thinking on giving higher tax share to states

Urban markets account for about 50-60% of total FMCG sales, the report added.

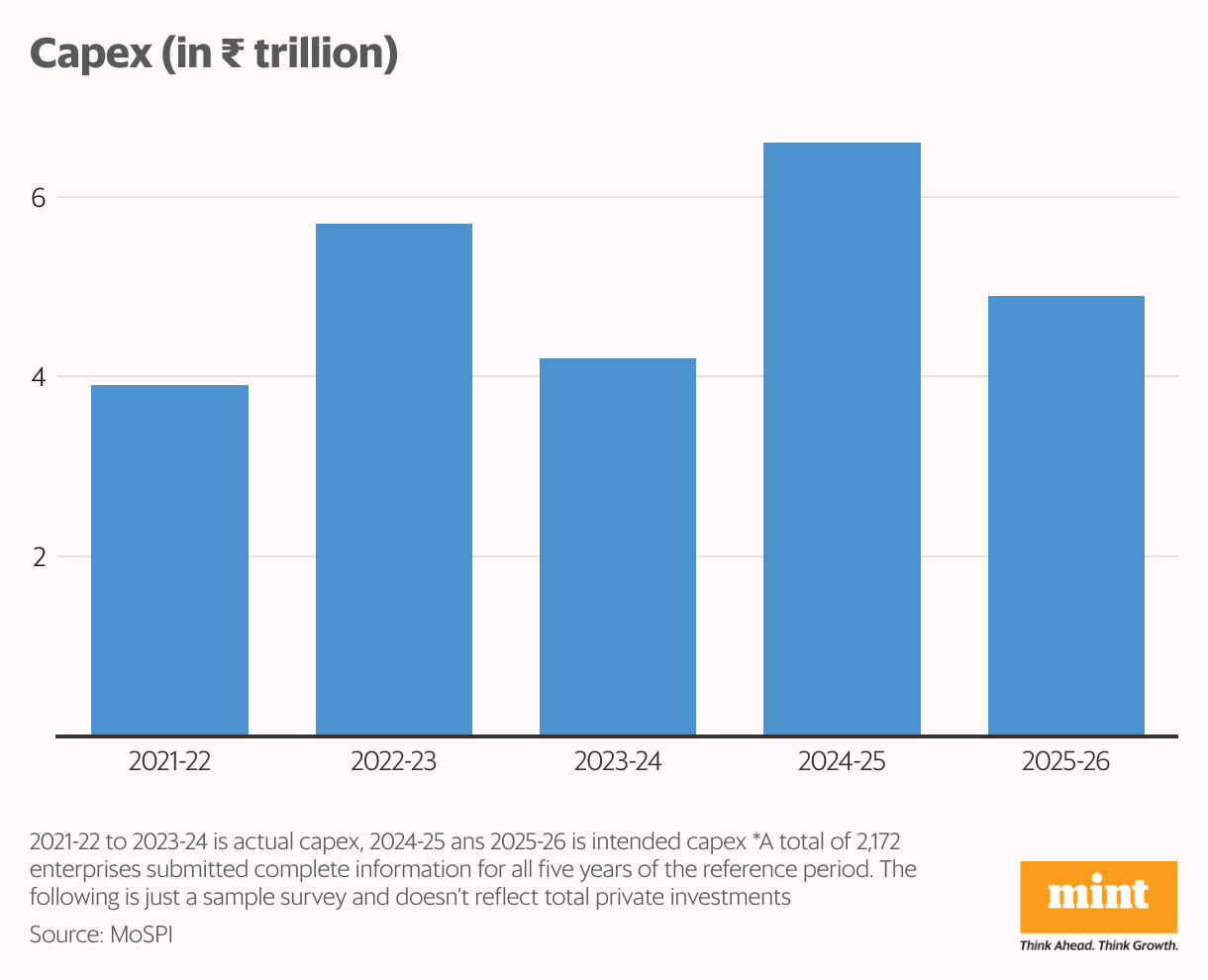

Government capex

According to the ministry of statistics & programme implementation data, Gross Fixed Capital Formation (GFCF), which indicates investment demand, picked up pace to 9.4% in Q4 FY25, as against 5.2% in Q3 FY25 and 6% in the year-ago period.

However, much of India’s recent capital expenditure has been powered by the government, with central capex doing the heavy lifting in the absence of a broad-based private investment revival.

For FY26, the Centre has pegged capex at ₹11.21 trillion, a slight uptick from ₹11.11 trillion (budget estimates) in FY25.

Sustaining 7%+ growth on government capex alone is mathematically possible in the short term but structurally unsustainable beyond the near term, said Rishi Shah, partner and economics advisory lead at Grant Thornton Bharat LLP.

Shah said while India’s consumption challenge runs deep, with household spending making up nearly 60% of GDP—and urban consumption remaining held back by weak jobs and uneven income growth—consumption and investment must grow together to sustain long-term growth.

“The realistic path to 7%+ growth involves using the current government-led (capex) phase to create conditions for private sector revival while ensuring consumption support through employment generation,” he said.

“It’s a delicate balance, but one that needs to be successfully navigated,” he added.

Meanwhile, foreign portfolio investors (FPIs) pulled out $3.2 billion in June (till 10 June), undoing May’s $3.6 billion inflow, rating agency CareEdge said in a report last week.

Also read: Retail inflation cools to a six-year low of 2.82% in May on moderating food prices

So far in 2025 (till 10 June), net outflows stood at $9.8 billion, driven by $11.2 billion in equity exits, partly offset by $1.6 billion in debt inflows, with volatility likely to persist in FY26, it added.

Spotlight on policy agility

The finance ministry’s latest economic review, released last month, flags mounting global headwinds, from rising policy uncertainty and volatile trade shifts to escalating geopolitical tensions, demographic pressures and climate-related disruptions.

The International Monetary Fund’s latest World Economic Outlook warned that the global outlook remains clouded by inflation, debt burdens and shrinking labour forces in advanced economies.

India’s growth momentum will hinge on strong domestic demand, driven by consumption, investment and exports, with key engines being private spending, capital formation and a steady export push, said D.K. Srivastava, chief policy advisor, EY India.

“There would remain an atmosphere of uncertainty regarding the contribution of net exports. Both monetary and fiscal policy should be continuously calibrated to minimize the volatility of growth,” he said.

Srivastava said government-led capex is likely to remain India’s key growth engine for at least two more years and with rising geopolitical tensions, a greater share may shift toward defence.

“At any rate, infrastructure deficiencies in India must be overcome to make Indian industry more competitive. As global demand picks up, the contribution of net exports to India’s GDP growth will become stronger and reliance on government capex may be eventually reduced,” he added.

Policy bets

To be sure, policymakers are betting on an above-normal monsoon, easing interest rates, and robust government capex to drive growth and shield the economy from global headwinds.

“There’s cautious optimism for FY26, with India projected to grow between 6.3% and 6.8%. Even if global headwinds intensify, 6.3% appears to be the lower bound, while 6.8% is achievable if global conditions remain supportive,” said a senior official who did not wish to be named.

The official cited opportunities from upcoming trade deals (with the US and EU), a growth-friendly monetary policy stance, middle-class tax relief (announced in the latest budget), and a well-distributed monsoon as key tailwinds for the economy.

The World Bank projects India’s economy to grow at 6.3% in FY26, while the International Monetary Fund pegs it slightly lower at 6.2%.

In its Global Economic Prospects-June 2025 report released last week, the World Bank emphasized that global risks are intensifying, with the spectre of further trade barriers and heightened policy uncertainty looming large.

It also highlighted concerns about higher-than-expected global inflation, which could lead to tighter financial conditions, potentially weakening regional currencies and spurring capital outflows.

India’s growth is robust, but global shocks now outpace policy responses, squeezing margins and shaking markets, warns Grant Thornton Bharat’s Shah.

“Our economy has built substantial buffers and adaptive capacity, but even the most resilient systems face stress when global policy uncertainty becomes the dominant variable,” he added.

{kind=link}

{kind=link}

{kind=link}

{kind=link}