Stock Market Today (LIVE): BridgeBio’s Blockbuster Sales; Aehr Pops 20% on New AI Customer; Is Apple Finally Closing the AI Gap?

📌 Top story — scroll down for more updates

Did BridgeBio Just Secure Longer Blockbuster Sales?

3:11 pm — BBIO +7.44%

By Karl Thiel

Team Rule Breakers

BridgeBio’s (BBIO +7.84%) Attruby has crushed all expectations since it was launched in late 2024. The drug, for a heart disease called ATTR-CM, can boast several advantages over competitors like Pfizer’s (PFE +0.97%) Vyndamax (tafamadis) and Alnylam’s (ALNY +4.62%) Amvuttra, not the least being its competitive price tag. One thing the company couldn’t claim before today, however, was that it had a long-term mortality advantage.

That just changed.

Today’s Change

(7.84%) $5.44

Current Price

$74.80

Key Data Points

Market Cap

$13B

Day’s Range

$71.21 – $74.87

52wk Range

$28.32 – $84.94

Volume

67K

Avg Vol

2.9M

Gross Margin

95.28%

Aehr Adds Customer In AI Data Center Market

2:43 pm — AEHR +22.50%

Shares of Aehr Test Systems (AEHR +23.56%) surged more than 20% after the chip-testing equipment maker revealed a “major” new customer—an undisclosed global networking leader building silicon photonics transceivers for data centers. The initial order is slated for shipment in fiscal Q4 2026, with management signaling potential follow-on demand as hyperscalers scale AI infrastructure. The win reinforces Aehr’s positioning in AI-driven semiconductor capex, particularly in fiber-optic interconnects.

- A Foot In The Fiber Future: Aehr’s silicon photonics exposure ties it directly to next-gen AI data center buildouts—an emerging, high-growth niche.

- Expectations Check Ahead: With shares up ~355% over the past year, upcoming earnings (April 7) will test whether momentum can match elevated investor expectations.

Today’s Change

(23.56%) $7.09

Current Price

$37.21

Key Data Points

Market Cap

$922M

Day’s Range

$33.00 – $37.52

52wk Range

$6.27 – $46.95

Volume

2.6M

Avg Vol

1.5M

Gross Margin

33.28%

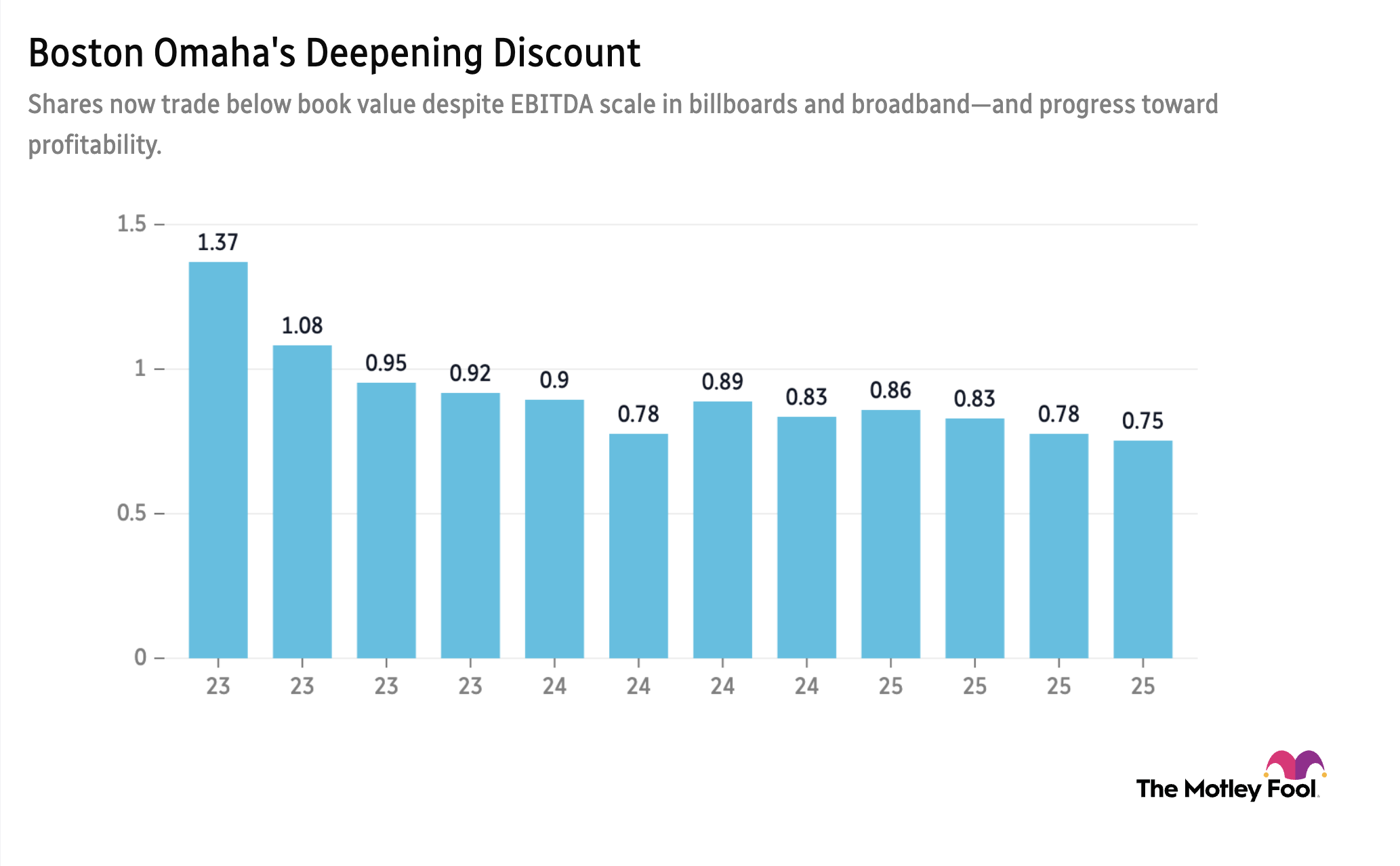

Boston Omaha Begins Buying Back Stock

2:28 pm — BOC -3.10%

By Buck Hartzell

Boston Omaha (BOC 1.93%) has achieved scale in two of its businesses. The billboard business and mature broadband businesses generated a combined $31.3 million in adj EBITDA. They invested $25.9 million in fiber capex (down 12% YoY) and the cash burn from Fast Fiber Homes was reduced to ($3.8 mil) adj EBITDA. The surety business is growing, but posted higher loss rates. They need to prove they can adjust and scale premiums profitably. BOC spent $5.8 mil on buybacks in 2025 and $4.8 mil already in 2026. Sky Harbour (SKYH +1.79%), their largest investment, is also scaling nicely. The stock remains attractive.

iOS 27 To Feature Siri Chatbot App

1:10 pm — AAPL +2.6%

Apple (AAPL +2.98%) is testing a significant Siri upgrade for iOS 27 that allows the assistant to process multiple commands within a single query. Historically a laggard compared to Google (GOOG +4.69%) and OpenAI, Siri is being overhauled into a chatbot-style interface with a standalone app and “World Knowledge Answers” for web summarization. Shares rose 2.6% on the news as investors look toward the Worldwide Developers Conference on June 8 for a full reveal. This modernization effort aims to integrate personal context and on-screen awareness, potentially driving higher user engagement and hardware upgrades this fall.

- The Productivity Play: By enabling complex, multi-step strings like “edit this photo and text it,” Apple is attempting to transform Siri from a simple voice trigger into a functional “agent” that keeps users locked into the ecosystem.

- Engineering Redemption: After multiple delays since its 2024 preview, the successful deployment of these features is critical for Apple to prove its “Apple Intelligence” branding can compete with established LLM leaders.

Today’s Change

(2.98%) $7.34

Current Price

$253.97

Key Data Points

Market Cap

$3.6T

Day’s Range

$247.12 – $254.12

52wk Range

$169.21 – $288.62

Volume

1.3M

Avg Vol

48M

Gross Margin

47.33%

Dividend Yield

0.42%

Today’s Lunchtime News

1:05 pm

Amazon (AMZN +4.09%) announced Tuesday that its Leo satellite internet service will power in-flight Wi-Fi on Delta Air Lines (DAL +5.60%) flights starting in 2028, marking a significant win against SpaceX’s Starlink in the race to connect commercial aviation.

- Speed leap: Delta planes will feature antennas supporting download speeds up to 1 gigabit per second and upload speeds of 400 megabits per second — fast enough for video calls and streaming at cruising altitude. Amazon’s Leo satellites orbit 370 miles above Earth, 50 times closer than older geostationary systems, which dramatically reduces the lag that has plagued in-flight Wi-Fi for years.

- Playing catch-up: Starlink already has thousands of satellites in orbit and serves airlines including Southwest (LUV +4.02%) and United (UAL +8.06%), while Amazon currently has just over 200 satellites in orbit with 20 more launches planned this year. The Delta deal is a meaningful commercial proof point for Leo, but closing the gap with Starlink will require significant execution on Amazon’s ambitious launch schedule.

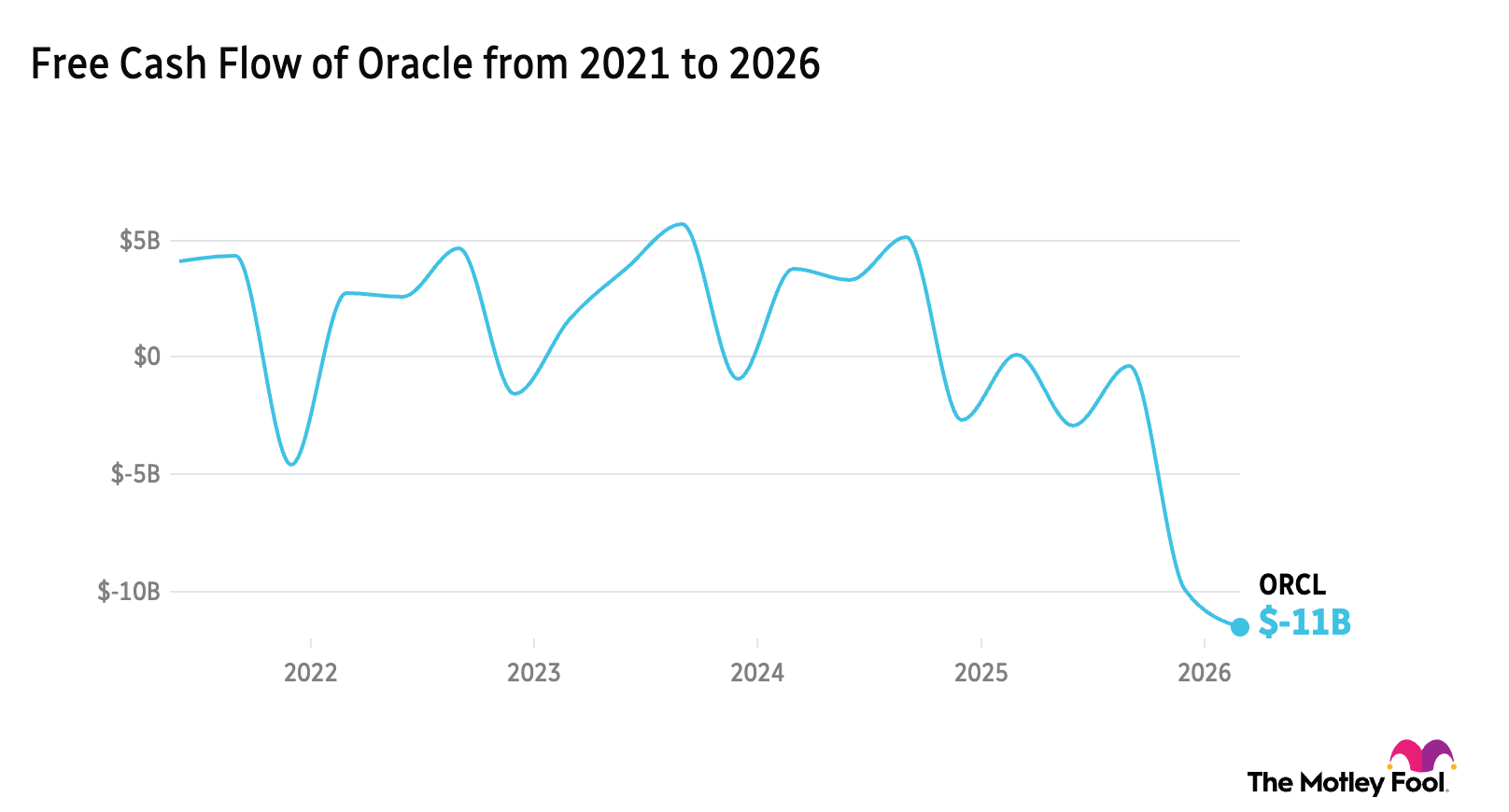

Will Layoffs Save Oracle’s Cash Flow?

12:15 pm — ORCL +2.8%

Oracle (ORCL +5.81%) is terminating thousands of employees as it aggressively reallocates capital toward artificial intelligence infrastructure. Shares have slid 27% this year as investors worry that massive data center investments are crimping cash flow, despite a staggering $455 billion in remaining performance obligations. This backlog was fueled by a recent $300 billion agreement with OpenAI, a partnership that has fundamentally altered the company’s trajectory. Under the fresh leadership of Mike Sicilia and Clay Magouyrk, Oracle is opting for a leaner headcount to offset the soaring capital expenditures required to maintain its status as a primary cloud provider for generative AI workloads.

- The Backlog Paradox: While the $300 billion OpenAI deal provides massive long-term revenue visibility, the immediate cost of building the physical infrastructure to service those contracts is forcing immediate, painful cuts to the legacy workforce.

- Capital Discipline Test: These layoffs signal that management is prioritizing margins over scale, attempting to prove to Wall Street that it can fund its transition into an AI powerhouse without further degrading its balance sheet.

Amazon MGM’s New Gold Standard

11:40 am — AMZN +2.7%

Amazon (AMZN +4.09%) MGM has officially found its theatrical “proof point” as Project Hail Mary surpassed $300 million globally, becoming the studio’s highest-grossing film ever. The Ryan Gosling vehicle showed remarkable staying power with a tiny 5% international dip in its second weekend, propping up a first-quarter domestic box office that is up 23% year-over-year. As traditional giants like Disney (DIS +2.54%) and the pending Paramount Skydance (PSKY +2.41%) and Warner Bros. Discovery (WBD +1.35%) merger lead to fewer annual releases, Amazon’s $1 billion annual commitment to cinema is positioned to capture a larger slice of the cultural zeitgeist and theatrical revenue.

- Filling the Content Vacuum: With Hollywood consolidation threatening to slash 15 releases annually, Amazon’s diverse 14-title slate for 2026 exploits a thinning marketplace to build a new theatrical “gold standard.”

- The Built-In Audience Advantage: Following the success of this Andrew Weir adaptation, Amazon is doubling down on literary hits like Colleen Hoover’s Verity to guarantee opening-weekend momentum through existing fanbases.

Nvidia’s $2B Marvell Bet Sparks 8% Pop

10:30 am — MRVL +7.6%

Shares of Marvell Technology (MRVL +12.19%) surged 8% Tuesday after Nvidia (NVDA +5.47%) announced a $2 billion investment to accelerate AI infrastructure. CEO Jensen Huang characterized the deal as an “expansion of our ecosystem,” specifically targeting the semi-custom ASIC market used by hyperscalers. This follows a string of identical $2 billion bets by Nvidia on firms like Synopsys (SNPS +3.16%), Coherent (COHR +7.90%), and Lumentum (LITE +6.51%). The partnership focuses on silicon photonics and telecommunications, providing Marvell with a massive capital infusion to “turbo-charge” its 2027 revenue outlook despite ongoing Middle East tensions.

- The ASIC Power Play: By aligning with Marvell, Nvidia is effectively colonizing the custom chip space, ensuring its architecture remains the foundation even as cloud giants attempt to design their own specialized silicon.

- Network Effect Dominance: This investment spree creates a formidable moat; as Nvidia embeds its capital into every layer of the AI stack — from optical components to cloud providers — it becomes nearly impossible for competitors to displace.

Top of the Morning

9:45 am — MCK +0.5%, UL -3.4%

By Emily Flippen, CFA

Team Rule Breakers

McCormick (MKC 5.57%) and Unilever (UL 5.50%) appear to be on the verge of finalizing what would be one of the largest deals in consumer staples history. Unilever confirmed this morning that it is in advanced discussions to combine its Foods division with McCormick in a transaction that could be announced as early as today. The deal would give Unilever nearly $16 billion in upfront cash and a 65% stake in the combined entity, which analysts estimate could be valued north of $46 billion. This comes after prior talks with Kraft Heinz over a similar combination reportedly fell through earlier this year, making McCormick the presumed backup bidder.

The question investors should be asking is not whether the deal makes strategic sense for Unilever. It clearly does.

CEO Fernando Fernandez has been moving aggressively to reshape Unilever into a beauty, wellness, and personal care company. He wants those categories to make up roughly two-thirds of Unilever’s sales, up from around 52% today. The company has already spun off its ice cream business, sold off The Vegetarian Butcher, Graze, and a handful of smaller local food brands. It might sound strange for Unilever to be selling off its food division (the division generates nearly 13 billion Euros in sales and has 22% operating margins, which are strong for the consumer packaged goods industry) but Unilever’s food brands, despite being healthy businesses, are growing in the low single digits and sitting inside a conglomerate that management thinks is worth more divided. The idea is relatively simple: should this deal go through, shareholders and management get a tax-efficient exit, collect a lot of upfront cash, and the market (hopefully) revalues the remaining “better growth” Unilever at a higher rate.

However, for McCormick and its shareholders, the story is more complicated. McCormick’s current market capitalization is about $14 billion today. The Unilever food division it is absorbing is valued at more than double that. McCormick is a company with organic sales growth projected at just 1% to 3% this year, sizable tariff exposure, and shares that have fallen 35% over the past twelve months as fears over margin compression have weighed on the industry. McCormick reported first quarter earnings today, and while the headline numbers were fine-meeting expectations- and management reiterated yearly guidance, ultimately McCormick is a business that has been dealing with headwinds in its commercial sales, slowing volume growth, and a consumer that has become increasingly price-sensitive. In fact, in its first quarter volume growth across the entire business was negative, with sales driven purely from acquisitions and price increases. And it is about to take on a food portfolio more than twice its size during this challenging operating environment.

While this clearly warrants caution, there’s also reasons that the market is optimistic. After all, McCormick shares were up around 3% premarket after the deal was rumored. It’s hard to not see value in combining great consumer goods franchises that just make more sense together than not: putting Hellmann’s and Knorr with Frank’s RedHot, French’s, and Cholula all in one portfolio creates a genuinely formidable condiments and seasonings business with global exposure. It makes more sense for McCormick to own these brands than Unilever. There is clear category overlap, and the potential for cost savings and distribution synergies across retail, foodservice, and industrial channels is significant. If this business can be run as a focused, stand-alone food company rather than a neglected division inside a beauty conglomerate, there’s a reasonable argument that you unlock “synergies” in the form of simpler and better capital allocation, innovation, or just simply a tighter operating environment.

This being said, there are still risks even if the bull case plays out for McCormick. They’d be funding the deal in large part with external capital, which could put its already fairly levered balance sheet at further risk. Also, some Wall Street analysts have speculated that Unilever shareholders that would own 65% of the combined entity might sell out of their McCormick shares after the deal goes through, given the fact that they never bought shares of Unilever for its food service exposure, which could put downward pressure on McCormick stock in the nearer-term. It doesn’t help that many investors might be reminded of other deals with similar structures, like the 2021 deal between International Flavors & Fragrances (IFF +2.79%) and DuPont’s nutrition business, which also used a Reverse Morris Trust to merge and whose stock fell roughly 70% over the following two years, weighed down by heavy debt and integration challenges.

That’s what makes this merger so challenging to evaluate: neither company is broken or truly struggling today. Unilever’s food business is profitable and stable, and would be a net asset to McCormick’s existing portfolio. The merger would let Unilever refocus its business on higher-growth segments. At the same time, McCormick is a well-run company with over a century of operating experience and strong operational discipline and investors who are comfortable with trading growth for cash, dividends, and profits. The question is whether combining them creates a business that is better positioned for the next decade of packaged food, or whether McCormick is biting off more than it can chew at precisely the moment when its own organic growth is under pressure and consumer habits are shifting in unpredictable ways, including the still-unclear impact of GLP-1 medications on food consumption volumes.

If the combined business can execute on integration, maintain the margin profile of both portfolios, and prove that being a dedicated food company with global scale creates real value, this could look like a smart transaction in hindsight. But history suggests that deals of this size and complexity rarely go smoothly in the near-term. I’d encourage investors to stay patient, watch how the market digests the combined entity’s capital structure, and look for early signs of whether McCormick’s management team is up to the task of running a business that might have just tripled in size overnight before buying into the hype.

Opening Bell

9:35 am — MSFT +2.1%, NVDA +2.2%

The Dow surged nearly 500 points Tuesday following reports that President Trump may end military hostilities even if the Strait of Hormuz remains restricted. The S&P 500 and Nasdaq followed suit, gaining 1.2% and 1.4% respectively as tech giants Microsoft (MSFT +3.48%) and Nvidia (NVDA +5.47%) led a broad rebound. Despite the optimism, Brent crude futures spiked 4% to $117 after an Iranian strike on a Kuwaiti tanker. While March is on track for its worst performance since 2022, analysts suggest this 10% pullback is a “normal” reset required for long-term equity returns.

{kind=link}

{kind=link}

{kind=link}

{kind=link}