Global Commercial Insurance Rates Fall 5% as Property Declines Offset US Casualty Pressure

Global insurance rates declined for the seventh consecutive quarter in early 2026, driven by property rate drops and persistent insurer competition, Marsh reports.

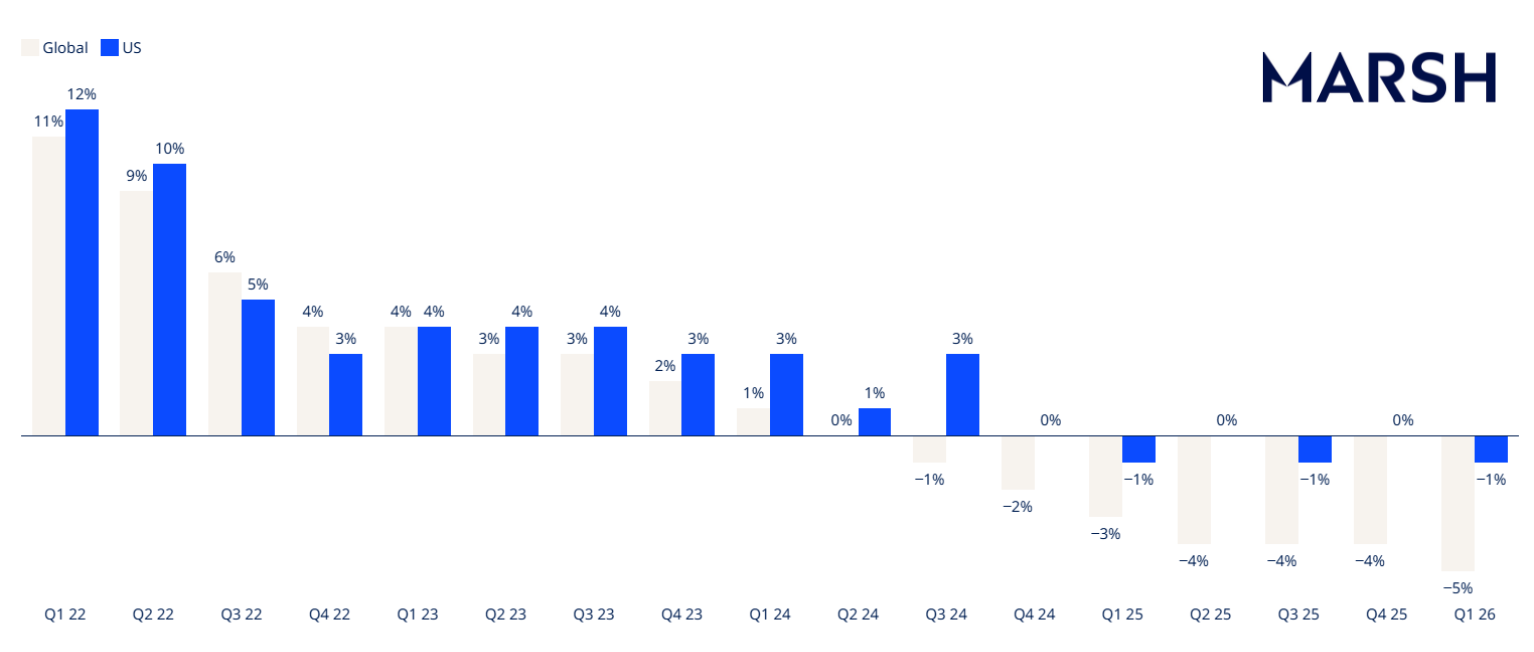

Global commercial insurance rates fell 5% in the first quarter of 2026, with property rates declining 9% and casualty rates rising 3%, according to Marsh’s Q1 2026 Global Insurance Market Index.

The divergence between softening property markets and a stubborn U.S. casualty environment defined the quarter, as available capacity and intense competition continued to push most lines downward while U.S. litigation dynamics kept casualty costs climbing.

“While the Middle East conflict is being carefully observed for its potential impact on insurance markets, the current competitive environment is expected to persist as insurer profitability remains strong. This is especially true in lines such as property, which is supported by favorable reinsurance terms and significant capacity, commented John Donnelly, president, Global Placement, Marsh Risk. “Given broad economic uncertainty and inflationary pressures, clients have the opportunity to optimize their program structures, increase limits, or adjust retentions to improve the resilience of their programs in the year ahead.”

Property Markets Extend Soft Streak

Property Markets Extend Soft Streak

The global property rate decline was fueled by favorable reinsurance terms and significant capacity oversupply, the report said. Insurers broadened their appetite to target more complex industries and the middle market, intensifying competition.

In the U.S., property rates dropped 10%, compared with an 8% decrease the prior quarter. Catastrophe-exposed programs saw 16% rate declines, while non-catastrophe programs fell 7%, the report found. Insurers showed greater willingness to offer policy enhancements and long-term arrangements, and submission requirements relaxed as underwriters increasingly accepted historical and alternative data sources. However, insureds with unfavorable loss histories or mitigation efforts did not experience similar decreases.

Some organizations used program savings to enhance coverage, invest in advisory services, or pursue alternative structures including captives and insurance-linked securities, according to the report.

U.S. Casualty Remains an Outlier

U.S. casualty rates rose 9% in the first quarter, unchanged from the prior quarter, the report said. Excluding workers’ compensation, the increase was 12%. Globally, casualty rates declined in every other region, particularly for companies without U.S. exposure.

The U.S. umbrella and excess liability market saw risk-adjusted rates rise 18%, with some insurers capping individual risk capacity at $10 million due to the adverse U.S. litigation environment. Rising claim frequency and severity — including nuclear verdicts and large settlements — continued to push attachment points higher, the report found. U.S. auto liability remained especially challenging amid continuing large jury verdicts and rising repair costs.

Underwriting tightened for emerging liability exposures including PFAS and human trafficking, leading to higher costs and increased retentions. Buyers increasingly explored alternative risk transfer and captive solutions, according to the report.

U.S. Financial Lines, Cyber See Modest Declines

U.S. financial and professional lines rates declined 2%, though underwriting grew more selective, the report said. U.S. directors and officers liability rates ranged from flat to 5% decreases, but capacity tightened in some segments as certain insurers exited the market. High excess layers proved more challenging to place than in previous quarters. U.S. fiduciary liability rates rose 3%, driven by ongoing ERISA excessive fee litigation.

U.S. cyber rates fell 2% in the first quarter, compared with a 3% decline in the prior quarter. Cyber was the only major line seeing notable expansion of both supply and demand, as many organizations purchased coverage for the first time or sought higher limits, the report found. Underwriters scrutinized aggregation risk from interconnected technologies, AI exposure, and privacy concerns related to tracking technology.

The generally decreasing rate environment is expected to persist as long as insurer profitability remains strong, the report said.

Obtain the full report here. &

{kind=link}

{kind=link}

{kind=link}

{kind=link}