Lots of monopoly related news, as usual. Apple CEO Tim Cook retired, Sam Altman and Elon Musk’s blood feud in a courtroom is about to start, Trump is considering bailing out oil-rich Arab states, and California Attorney General Rob Bonta exposed Amazon’s economy-wide price-fixing with other major online retailers.

Before getting to that, today I want to spend a little time discussing the economic dilemma that prevents any meaningful political change. I’m thinking about this problem, what I call the Chinese finger trap economy, because I’m watching how the Democrats are preparing, or rather, not preparing, for their likely victory in six months in the midterm elections.

There were two events this week that led me to think about why all our political leaders seems so terrified to change anything in our economy. Both have to do with artificial intelligence.

First, Maine Governor Janet Mills vetoed a widely supported bill temporarily banning the construction of more data centers in the state, a proposal put forward by Senator Bernie Sanders and populist Democrats that has broad popular appeal. Mills is a Democratic candidate for Senate handpicked by Chuck Schumer.

Second, the House Foreign Affairs Committee quietly passed something called the Full Stack AI Export Promotion Act, which codifies a Trump executive order and turns the State, Defense, and Commerce Departments into a marketing arm for Google, Anthropic, and OpenAI. You’d think it would encounter some opposition, if for no other reason than mindless partisanship. But it went through 37-7. Why? The top Democrat on the committee, Greg Meeks, is a money-driven leader of the Queens machine in New York City. The only votes against were left-leaning populists.

This pro-AI stance among elites is something of an oddity, if you imagine politicians try to do things that are broadly appealing. After all, over the past three years, generative artificial intelligence has become terribly unpopular. In Virginia, approval of data centers dropped from 69% in 2023 to 37% in 2026, which is a massive decline. Eighty percent of Americans are at least somewhat concerned about AI.

But the political class is still boosting these giant AI firms. Donald Trump has made his main economic policy to subsidize data centers, and many establishment Democrats are, at best, quite reluctant to impose any sort of limits on these dominant firms. Why? It’s not as simple as saying “corruption,” because Mills and Meeks have broad support from voters, as does Trump.

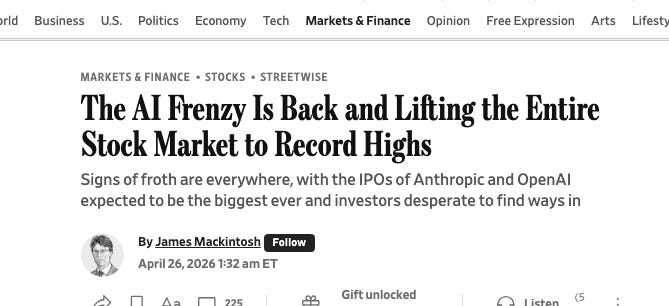

The limiting factor, in fact, is the stock market. There are many ways to talk about AI, as the technology itself is interesting. But most AI ‘policy’ is a proxy for juicing the stock market. As the Wall Street Journal just reported, “Exclude the AI version of the Magnificent Seven stocks—Broadcom alongside Alphabet, Amazon, Apple, Meta, Microsoft and Nvidia—and the market value of the S&P is actually down. Put another way, these seven are lifting the entire market.”

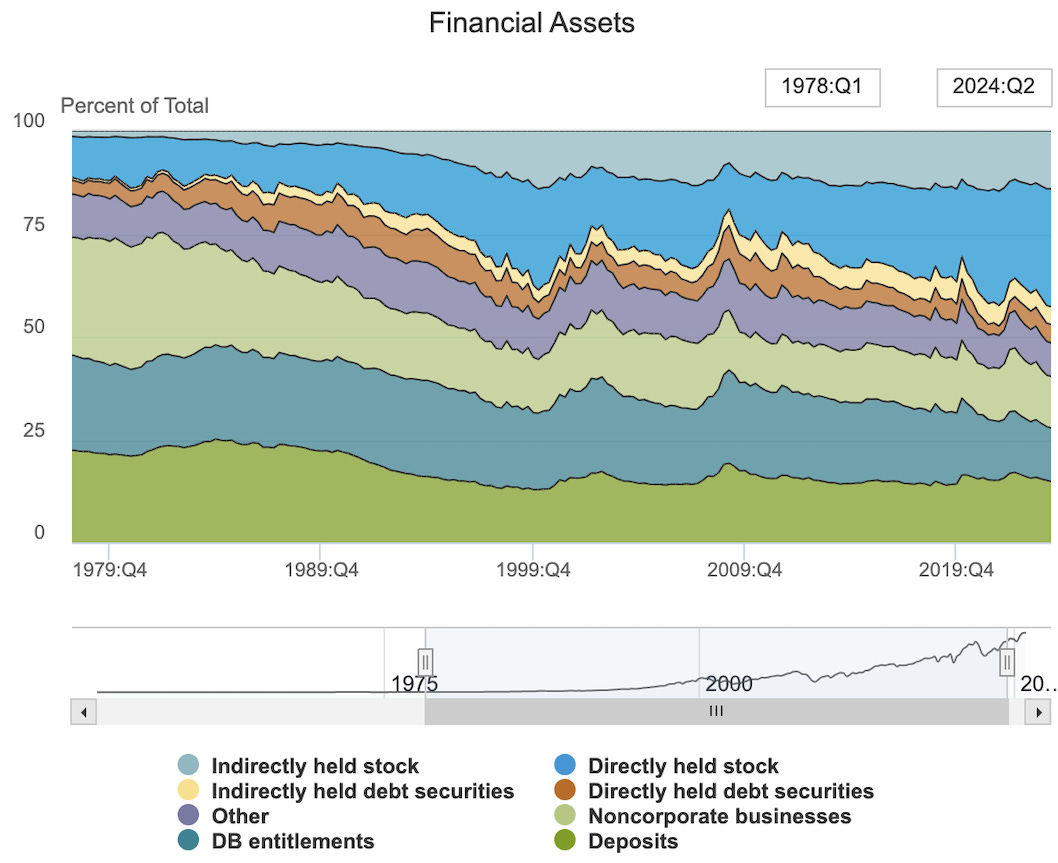

A little over 60% of Americans own stocks, and though most own very little, they still care about it because it’s often all they have for retirement. America is just much more reliant on stocks than it used to be. Here’s the balance sheet of American households and nonprofits.

You can see the growing importance of equities from 1979 to 2024. This chart is broken out by percentage though if you’re curious, financial assets have increased from $5 trillion to $125 trillion.

Every institution of power is now linked to the market. CEOs get paid based on the value of their stock, and Wall Street benefits from high valuations. Nonprofits, which include churches, universities, hospitals, foundations, and charities, have $1.8 trillion of stock. Cities and states have their pensions invested in the market, as do unions. California and New York, as well as many other political entities, are reliant on income from capital gains for their budgets. And 18% of the stock market is owned by foreigners, so the market is a key geopolitical tool and a mechanism to keep imports of electronics, food, fuel, machinery and medicine flowing to U.S. consumers.

What does this dynamic mean? Well, if financial assets fall in value, then it means the entire global hierarchy gets shaken up and reorganized, with unforeseen consequences. Many formerly rich people will go bankrupt, others won’t be able to feed or educate their kids, entire nations could go into civil war. In the 1930s, when this kind of thing happened, Hitler came to power in Germany. That is why we’re so scared of a market drop. That is why Trump is fighting the war with Iran, entirely bounded by the stock market. It is why we didn’t acknowledge the severity of Covid until the markets fell. Financial asset values are the lens through which we understand what problems are important to solve.

And yet, the stock market’s valuation prevents any useful change in our social order. A few weeks ago, on the Odd Lots podcast, Joe Weisenthal and Tracy Alloway profiled a paper that describes the dilemma we’re in. It’s titled “A Macroeconomic Perspective on Stock Market Valuation Ratios,” and it’s by three economists, Andrew Atkeson, Jonathan Heathcote, and Fabrizio Perri. The paper describes an economy designed around enshittification, though that’s not what they say directly.

What they were trying to describe is why the stock market is so high, what most people consider to be at a historically inflated level. What these economists show is that this inflated value has a structural explanation. American corporations have dramatically lowered their share of output going to workers since the 1980s, and have also reduced the amount they are investing in new factories, software, robots, et al.

That means they can return more to investors in buybacks and dividends. So the stock market is not high relative to the amount investors are getting back. How do companies sustain such low levels of investment and hiring, and such high profit margins, without encountering competition? Well these are conflict-averse economists, so they shy away from saying anything interesting. But the final line in the paper is as follows:

A final possible explanation for the strong observed growth in earnings absent growth in measured investment is that firms have enjoyed an increase in monopoly power in recent decades, and that this has allowed them to earn greater pure rents or “factorless income” that is not income to capital.

Their paper draws on a lot of work from anti-monopolists, who noticed the trends of declining investment and labor share of corporate output in the late 2010s. And the evidence keeps piling up. Another recent paper shows that a third of the post-1980 slowdown in wage growth is a result of noncompete agreements and more employer concentration.

Basically, financial assets depend on the ability of companies to extract from customers, suppliers, creditors, governments, workers and communities. Every junk fee, every subscription trap, every speculative trade in an AI bubble, these are all mechanisms to keep stocks up. Regulating the bad behavior away will thus limit profits, and cause the market to go down. And yet the market must go up.

Because of what I do, I run into labor union officials on a fairly regular basis, and these are the people who are structurally concerned with increasing wages. And yet, most labor unions have their own capital markets group negotiating over pensions, whose goal is to maximize financial returns for their members. The net effect is that say, Texas teachers will invest in private equity funds seeking to break unions elsewhere. Unions effectively have some of their resources dedicated to increasing wages, and some of their resources dedicated to lowering them via achieving better market returns.

We are caught in the economic version of a Chinese finger trap. Attempting to pull the contraption off one finger tightens it on the other.

I’m hopeful about a lot of things, the public is turning towards a more populist outlook, there’s increasing awareness among state officials of the problem of market power, and Trump’s leadership is deeply unpopular. But every time I try to play out possible scenarios of what could happen, I run into the problem of Wall Street’s hold on the Democratic Party. And that hold is not about a few dollars given here or there, it’s fundamentally baked into our institutions.

If anyone tries do anything socially useful that lowers the enterprise value of firms, whether that’s prohibiting monopolies, junk fees, or any other form of extractive behavior, the market will go down. But if the market goes down, huge numbers of Americans suffer, and a bunch of Western institutions will break.

To get out of this trap doesn’t necessarily mean the market has to go down. Often, companies can earn more cash when they are broken up – that certainly was the case with Standard Oil. But my guess is that a market decline will be necessary to have any political reform. That is in fact why so many people have an emotional need to call for market declines, over Iran or AI or anything else. It’s not that anyone knows we’re in a bubble, it’s that decisions are happening in a way over which we have no control. Popping a bubble is a deus ex machina way to wipe out the current leadership class, and restore some sense of community control. But of course, that has very significant risks.

There’s a historic precedent here. Market declines, whether the crisis of 1857, the panic of 1906, or the 1929 crash, often lead to political reforms after periods of listless apathy and frustration. Here’s how Rep. Emanuel Celler characterized the first days in 1933, when Franklin Delano Roosevelt took over.

“In March of 1933 we had witnessed a revolution – a revolution in manner, in mores, in the definition of government. What before had been black and white sprang alive with color. The messages to Congress, the legislation, even the reports on the legislation took on the briskness of authority.”

Imagine that. Anyway, the Democratic Party is likely to be a fractured group coming into the majority, with the polling showing overwhelming support for populist ideas, but unable to test for the deep-seated fear of what a market drop might imply. And that’s why Democrats have nothing to say, and seem so meek. No one wants to be the political leader to say “The market must drop.” It doesn’t even matter if they are cynics or dupes. They are trapped. As are we all.

And now, the rest of the monopoly round-up. Lots of fun stories. The Elon Musk-Sam Altman blood feud starts in court tomorrow, most but not all 2028 Democratic contenders are calling Lina Khan for advice, Kevin Warsh’s nomination to become Fed Chair moves along, and the Chinese rare earth monopoly is starting to fade. And in AI bubble watch, the company behind Prego spaghetti sauce is launching a listening device to tape dinner conversations. Because why not?

Lots of fun stuff this week, after the flip.

{kind=link}

{kind=link}

{kind=link}

{kind=link}