When planning for retirement, most investors concentrate on what to invest in—stocks, bonds, cash, and other assets. But an equally important, and often overlooked, decision is asset location—which accounts to hold those investments in.

Because they sound so similar, asset location could be confused with asset allocation. The distinction is simple but important. Asset allocation refers to the mix of investments you choose, for example, stocks, bonds, or cash. Asset location, on the other hand, is about deciding which account to use for each investment, whether it’s a taxable brokerage account, a tax-deferred account like a traditional IRA, or a tax-exempt account like a Roth IRA.

By placing your investments in accounts to minimize tax drag, you enhance your portfolio’s aftertax performance, but you don’t have to reduce your annual retirement spending. Your long-term financial outcomes also get a powerful impact from asset location.

According to Morningstar Retirement research, for an investor with a $1 million portfolio at retirement, asset location increases their final bequest by an average of $112,000—equivalent to a performance boost of as much as 30 basis points annually, without sacrificing annual spending. This offers a powerful way to maximize a retiree’s financial security and legacy.

A Tax-Aware Retirement Strategy

The core benefit of asset location is improved tax efficiency. It boosts your portfolio’s aftertax performance, but without requiring you to reduce your annual retirement spending. As mentioned above, the gains come purely from optimizing the placement of investments in accounts to minimize tax drag.

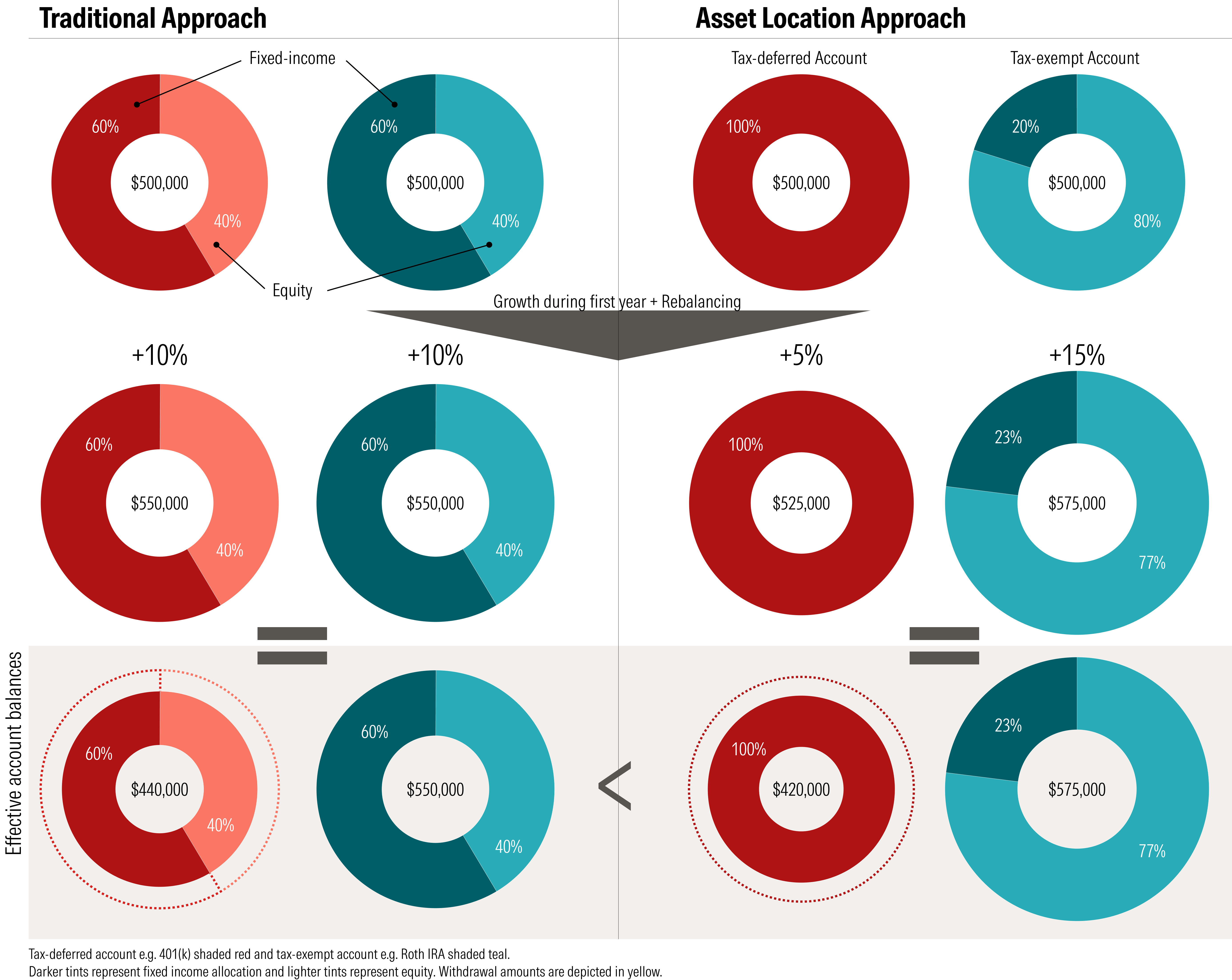

Let’s use a bond fund as an example. A bond fund’s return has two parts: price changes and income from coupon payments. This income is distributed as dividends, which are taxed at your ordinary income rate—potentially as high as 37%. If you hold this fund in a standard taxable brokerage account, your aftertax return will be significantly lower than the fund’s reported pretax return because you must pay taxes on those dividends out of pocket.

Now, under an asset location strategy, imagine holding that same bond fund in a tax-deferred 401(k). Inside the 401(k), the dividends are not taxed annually. The entire pretax return can be reinvested and continue to grow tax-deferred, dramatically increasing its compounding power. You only pay taxes when you withdraw money in retirement, often at a lower marginal tax rate. The single, simple, strategic choice of account—the location—makes all the difference.

How to Implement an Asset Location Strategy

Implementing an asset location strategy is straightforward. You can begin by understanding your account options. Broadly speaking, there are three kinds of accounts: tax-deferred, tax-exempt, and taxable.

- Tax-deferred accounts, like traditional 401(k)s and IRAs, allow you to contribute pretax dollars and grow investments tax-free until retirement, when withdrawals are taxed.

- Tax-exempt accounts, such as Roth IRAs, are funded with aftertax dollars, but both growth and withdrawals are tax-free.

- Taxable accounts, like standard brokerage accounts, are also funded with aftertax dollars, and dividends and capital gains are taxed as they occur.

Say you already have a tax-deferred account through your employer. By opening another type of account, such as a tax-exempt account, like a Roth IRA, you could leverage the benefits of an asset location strategy to maximize your tax savings.

You want your largest gains to occur in the account that will not be taxed in the future. Therefore, a general rule is to place your assets with the highest growth potential, like stocks and equity funds, into your tax-exempt Roth accounts. This ensures that decades of compound growth from your most aggressive investments can be withdrawn entirely tax-free in retirement.

Conversely, your assets with lower expected growth, such as bonds and bond funds, are better suited for your tax-deferred accounts. While the withdrawals from this account will be taxed, the total tax bill will be on a smaller amount of growth compared with what your equities would have generated. This strategy maximizes the powerful benefit of the Roth’s tax-free status by filling it with your investment “all-stars.”

Finally, it’s important to know that asset location isn’t a high-maintenance strategy. It should receive updates over time but doesn’t require constant monitoring. As your income, tax situation, or retirement goals change, your asset location strategy might, too. The most important consideration is that it should be deployed in tandem with an appropriate asset allocation. In fact, allocation takes precedence. A yearly check-in, perhaps with a financial advisor, is typically sufficient to ensure your overall investment strategy—that is, both asset allocation and location, remains aligned with your long-term goals.

By thinking not just about what you own, but also where you own it, you can unlock significant value and ensure your retirement strategy is as powerful as it can be.

{kind=link}

{kind=link}

{kind=link}