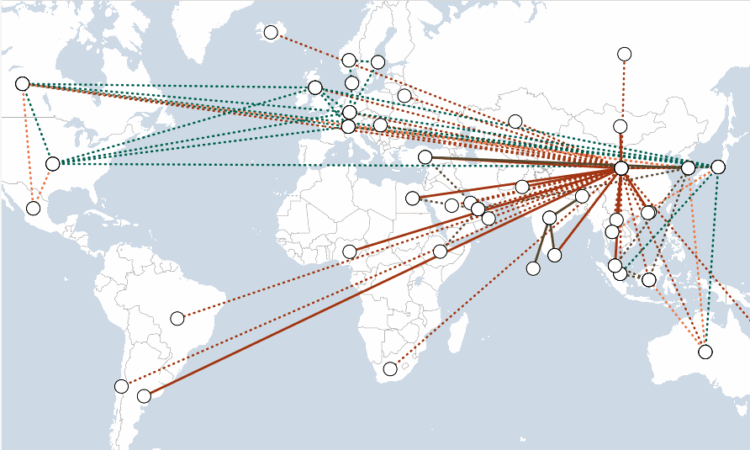

As it did during the Global Financial Crisis, the Fed again extended swap lines to select emerging-market central banks during the pandemic. The Fed approved emergency lines on March 19 for Brazil, Mexico, South Korea, and Singapore—the same nations that had received them in 2008. As with its emergency developed-world swap lines, the Fed approved the lines for six months and later renewed them through the following March. The Fed’s emergency swap line agreements with Brazil, South Korea, Mexico, and Singapore expired in 2021.

ECB Swaps

Global Financial Crisis (2007-2008)

The ECB established swap lines with Sweden in December 2007, Switzerland and Denmark in October 2008, and the UK in December 2010. The euro area, Sweden, Denmark, and the UK had relatively low foreign exchange reserves going into the crisis, owing to the costs involved in holding reserves and the belief that there was little likelihood that more would be needed in the foreseeable future. However, banks in these countries borrowed large sums in foreign currencies in the years leading up to the crisis. When it became difficult for them to borrow funds in 2008, they turned to their central banks, reserves of which proved insufficient to meet the unanticipated demand. The ECB swap lines were therefore called into use in 2009 to provide Sweden and Denmark euros with which to top up their foreign exchange reserves, and the swap line with Switzerland was called upon to provide the ECB with Swiss francs. The swap line with the Bank of England was put in place as a precautionary measure to ensure that the Central Bank of Ireland, which is part of the Eurosystem, had access to pounds sterling, but it has never been used. Since 2007, Sweden and Denmark have more than doubled their foreign exchange reserves, the UK has doubled its reserves, and the euro area has increased its reserves by 20 percent.

The ECB initially agreed to provide euros to Hungary, Latvia, and Poland only through repurchase agreements, in which securities rather than currency are held as collateral, but eventually extended temporary swap lines to Hungary and Poland. Switzerland also provided Swiss francs to Poland and Hungary in exchange for euros. Many households in Poland and Hungary had taken out foreign-currency-denominated mortgages because of the lower interest rates available on these loans. Demand for Swiss francs and euros from the Hungarian and Polish banks that issued the loans drove up borrowing costs in these currencies; the swap lines were intended to alleviate the upward pressure this demand was placing on euro and Swiss franc interest rates.

COVID-19 Pandemic (2020)

On March 20, 2020, the ECB reactivated a swap line with the Danish National Bank––the first of its measures to stabilize markets amidst the COVID-19 pandemic. In April, the ECB approved a temporary line to Croatia, and seven days later it granted one to Bulgaria. While the pandemic considerably strained the U.S. dollar funding market, as market participants rushed to hold more of the world’s reserve currency, global markets for euros remained relatively calm. As such, all three of the newly extended swap lines were not activated.

Over the course of the pandemic’s early months, the ECB also established repurchase agreements with Romania, Albania, North Macedonia, San Marino, Hungary and Serbia. While swap lines––extended only to countries with the highest creditworthiness––are backed by the borrowing bank’s foreign currency, repo lines extended by the ECB require high-quality euro-denominated financial assets as collateral. Without having to rely on the standing of a foreign currency, repo lines are more freely extended to non-euro area countries. Accordingly, the Eurosystem Repo Facility for central banks (EUREP) will be available to nearly all foreign central banks starting in the third quarter of 2026, further expanding the euro’s role beyond the Eurosystem and into global markets.

{kind=link}

{kind=link}

{kind=link}