Sandisk (SNDK 3.79%) stock has been one of the top performers on the stock market in 2026, with shares of the memory specialist rising more than 5x so far this year. However, what’s worth noting is that analysts expect Sandisk’s red-hot rally to continue even after its remarkable rally.

Last month, equity research firm Bernstein noted that this semiconductor stock could soar to $3,000. Analyst Mark Newman of the investment research firm believes that the booming demand for NAND flash chips and the sustained increase in pricing will be a tailwind for Sandisk.

Bernstein’s $3,000 estimate is based on a significant increase in the company’s earnings over the next three years, suggesting the stock will double from current levels. But can Sandisk indeed live up to Bernstein’s expectations and deliver such terrific gains? Let’s find out.

Image source: The Motley Fool.

Sandisk’s valuation suggests that the market hasn’t completely priced its growth potential

Sandisk is trading at 50 times earnings, a slight premium to the tech-focused Nasdaq Composite index’s price-to-earnings ratio of 43. However, this premium is justified by the exponential earnings growth that Sandisk has been clocking.

Today’s Change

(-3.79%) $-58.49

Current Price

$1483.75

Key Data Points

Market Cap

$219B

Day’s Range

$1474.30 – $1527.78

52wk Range

$36.21 – $1600.00

Volume

306.2K

Avg Vol

17.1M

Gross Margin

56.04%

The company’s adjusted earnings in the first nine months of fiscal 2026 (which ended on April 3) jumped by 11.5x year over year to $31.32 per share. Even better, Sandisk’s guidance of $31.50 in earnings per share for the current quarter points toward a massive acceleration in growth. Sandisk is therefore on track to end fiscal 2026 with $62.82 in earnings per share (based on the midpoint of its earnings guidance for the current quarter).

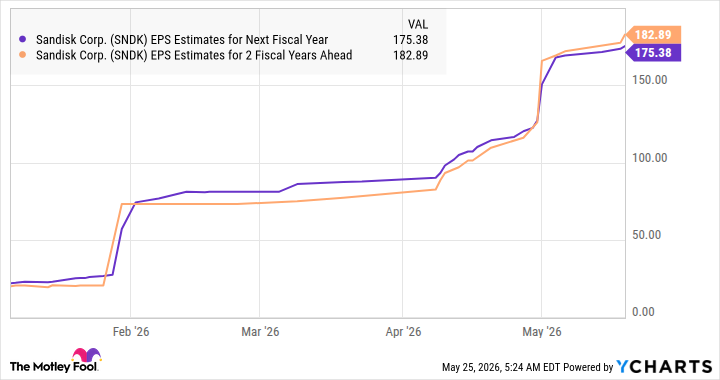

That would be a huge improvement over the earnings per share of $2.99 it reported in fiscal 2025. Analysts have also become bullish about Sandisk’s earnings growth over the next two fiscal years.

Data by YCharts

The stock is trading at just 22 times forward earnings. Assuming Sandisk maintains this multiple after a couple of years and its earnings per share indeed reach $182.89, its stock price will reach $4,023. So, Bernstein may be underestimating this AI stock’s upside potential, especially considering that the favorable demand and pricing environment driving Sandisk’s phenomenal growth is sustainable.

Solid NAND flash demand will be a tailwind for Sandisk

According to data storage solutions provider Seagate, global data generation is poised to more than double to 2.4 zettabytes (ZB) in 2028 from 1.1 ZB in 2024, driven primarily by AI. So, Sandisk’s addressable market is on track to keep growing at an incredible pace in the coming years.

Importantly, traditional storage solutions such as hard disk drives (HDDs) are already sold out for 2026. As a result, hyperscalers have been turning to flash-based storage products such as solid-state drives (SSDs). McKinsey estimates that the enterprise SSD market could grow at an annual rate of 35% through 2030 in a base-case scenario.

So, the healthy storage demand that has been fueling Sandisk’s outstanding growth isn’t going away. That’s why investors looking to add a top growth stock to their portfolios will do well to buy Sandisk, as it is capable of soaring significantly despite multiplying impressively in 2026.

{kind=link}

{kind=link}

{kind=link}

{kind=link}