A decade has passed since Chinese group Midea announced its €4.5bn takeover of Germany’s Kuka — a deal that helped catalyse the EU’s modern-day economic security framework and whose legacy is still sparking debate today.

On May 18 2016, the Guangdong-based appliance manufacturer became part of that year’s record €51.7bn wave of Chinese investment into the EU, according to Merics and Rhodium Group.

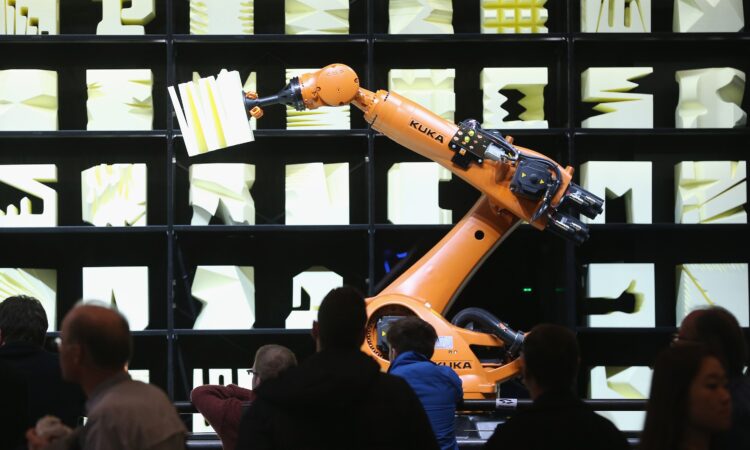

But losing control of the Augsburg-headquartered maker of the orange robotic arms seen in factories worldwide shook up Germany in ways other Chinese deals hadn’t.

M&A practitioners didn’t really care about FDI screening prior to Kuka–Midea . . . It was kind-of toothless

Kuka was an emerging national champion in automation, a symbol of German engineering prowess as Industry 4.0 was taking hold. Its takeover laid bare Europe’s lack of national security tools to intervene in deals beyond traditional defence sectors. The 60 per cent premium paid by Midea underscored Chinese strategic thinking behind foreign direct investment.

“It was a historic turning point for FDI screening in Europe,” says Alexander Otto, a partner at consultancy FGS Global who was involved in the transaction. “M&A practitioners didn’t really care about FDI screening prior to Kuka–Midea . . . It was kind-of toothless. Purely theoretical.”

That changed in the wake of the deal, which set in motion stronger FDI reviews, a new focus on protecting strategic industries and, a decade later, queries over whether EU economic security is going too far.

Kuka kerfuffle

Midea’s takeover of Kuka sparked an unprecedented level of public debate and political backlash against Chinese investment in Germany. However, it fell outside the country’s seven year-old formal FDI screening rules, which covered 25-plus per cent stakes in military equipment and IT encryption of classified information.

The government could have blocked the deal using a little-used authority that covered investments by non-EU companies that endanger public order or security. But “at the time, it would have been a very large step for the government” to put Kuka–Midea in this category, says Uwe Salaschek, a partner at Freshfields in Berlin. These cross-sector review powers had only been used on military-related deals and using them against Midea risked upsetting China, with which Germany had deep economic ties.

[They] started realising there are transactions where they need to be more careful

The government instead tried in vain to find an alternative European buyer. Once Midea’s acquisition closed, Germany made successive reforms expanding the sectors requiring mandatory screening notification to include critical infrastructure and technologies, and lowering the threshold to 10 per cent.

Just as important was the shift it sparked away from a purely open markets mindset within Germany’s FDI screening unit. “[They] started realising there are transactions where they need to be more careful,” says Roland Stein, director of the Celis Institute, who describes the deal as a “loss of naivety” regarding FDI.

This new ideology and rule book, also inspired by principles of technological sovereignty, have led Germany to block or restrict more than 10 acquisitions since 2016. That includes reversing its earlier approval of a €670mn Chinese takeover of semiconductor equipment maker Aixtron and forcing Cosco to reduce its proposed stake in a Port of Hamburg terminal from 35 per cent to 24.9 per cent.

Economic security precursor

The Kuka deal unfolding in Germany, the EU’s largest economy, meant its ramifications didn’t stop at national borders. It came one year after Beijing launched its Made in China 2025 roadmap, which targeted advancements in 10 manufacturing-related sectors, including robotics.

“When Kuka became a target, it suddenly dawned on Berlin that this was all part of a top-down strategy in Beijing to acquire strategic assets in Europe and help China reach its goals” to dominate those industries, says Noah Barkin, a senior adviser at Rhodium Group.

When Kuka became a target, it suddenly dawned on Berlin that this was all part of a top-down strategy in Beijing to acquire strategic assets in Europe

Germany pushed the issue up the European Commission’s agenda in early 2017 by partnering with France and Italy to propose that Brussels consider co-ordinated FDI screening across the EU to avoid the “possible sellout” of EU expertise. That proposal became the genesis of the EU’s first FDI Regulation in 2019, which required member state co-operation when reviewing deals. In May 2026, exactly 10 years after the Kuka–Midea announcement, the European parliament approved stricter bloc-wide screening rules, which include mandatory notification of deals in semiconductors, quantum and artificial intelligence.

FDI review is just one part of the EU’s growing economic security architecture, but experts see similarities across other parts of the spectrum with concerns raised over Kuka–Midea. These centred on the loss of technology and wholesale shift of resources out of Germany. Fast-forward to today, and the Industrial Accelerator Act requires investors from dominant countries like China to keep knowhow and intellectual property in the bloc, and commit to minimum R&D and local workforce thresholds when investing in four of the EU’s most strategic industries.

Alleged risks regarding access to Kuka’s customer data were also a preview of the contemporary push towards data sovereignty. Meanwhile, Midea’s receipt of subsidies, totalling $197mn in 2017 according to Global Trade Alert, helped bring on to the EU agenda how state financing can create an uneven playing field — an issue now tackled by the Foreign Subsidies Regulation.

“Current policies are full of examples that show EU policymakers have closely followed these [early] cases,” says André Wolf, head of technology, infrastructure and industrial development at the Centre for European Policy.

The reckoning

Yet Wolf is among other fDi sources to observe that Kuka–Midea’s outcome to date “from a European industrial policy perspective has been mixed”.

Kuka’s headquarters remain in Augsburg and 4,000 of its 14,500 workers are in Germany. Data is still ringfenced in the EU and it continues to invest in German R&D. “Being associated with Midea as a company . . . is very positive for Kuka,” the German group’s CEO Christoph Schell told fDi earlier this year. “Midea has a very long-term plan for Kuka and we’re executing on that plan.”

A spokesperson says “we don’t see any disadvantages arising from our ownership structure”. Freshfields partner Florian Sippel, who advised the acquirer, describes Midea as “one of the most sophisticated investors” he experienced during the mid-2010s surge of Chinese investment.

It’s a good point to reflect on whether [policymakers] overreacted, and whether tighter FDI screening and over-regulation is good for EU competitiveness

On the flipside, Kuka’s investment in China is growing faster than in other regions, in line with the country generating 54 per cent of global demand for industrial robots. Midea is no longer bound by the pledges it made in 2016 to guarantee Kuka’s local operations, although Kuka itself committed to no lay-offs in Augsburg for operational reasons until 2029. And Chinese investors’ cost-driven reputation doesn’t bode well for local investment in the long term.

If the same deal was proposed today, most fDi sources expect it to be blocked or subjected to reviews or conditions that would make it unviable.

With the jury out on whether the deal warranted the alarm bells a decade ago, Linlin Liang, director of communication and research at the China Chamber of Commerce to the EU, believes the time is ripe for Brussels to reconsider the direction of economic security. “It’s a good point to reflect on whether [policymakers] overreacted, and whether tighter FDI screening and over-regulation is good for EU competitiveness.”

{kind=link}

{kind=link}

{kind=link}

{kind=link}