Tenant referencing still runs on emailed payslips. Rent is collected via card or direct debit with end-of-month reconciliation done by hand. Contractor invoices are paid one bank transfer at a time.

These are not edge cases. They are the standard operating model for most UK letting agencies, property managers and portfolio operators — and the friction they create is measurable in time, cost and avoidable risk.

Open banking is infrastructure that addresses this directly. It gives property businesses consented, real-time access to bank-verified financial data and a way to initiate payments from a customer’s bank account, without routing through card schemes or requiring paper documents.

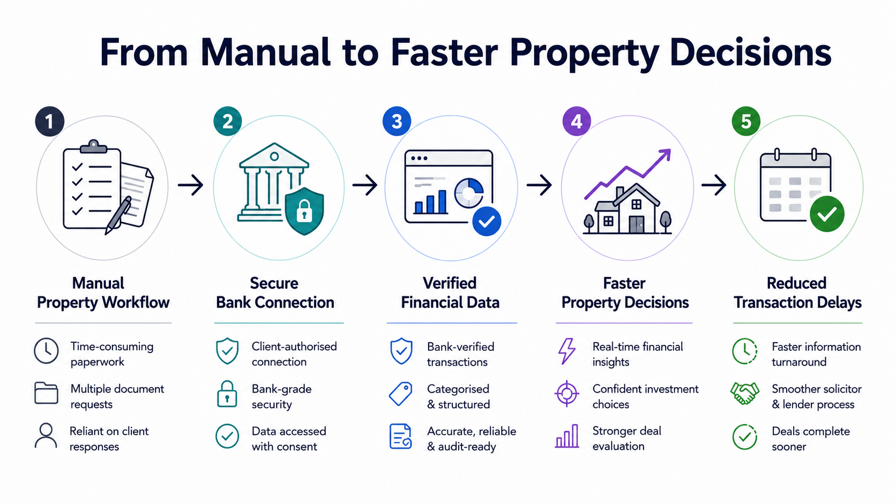

How open banking changes the property workflow: from manual document collection to bank-verified data, faster decisions and reduced transaction delays.

What open banking means for property businesses

Open banking in the UK operates under the Payment Services Regulations, derived from PSD2, and is overseen by the Financial Conduct Authority. Providers must hold an FCA authorisation to offer these services.

Two capabilities matter most for property:

Account Information Services (AIS) provide read-only, consented access to a customer’s bank account data — income transactions, balance history, account ownership and spending patterns — drawn directly from the bank, not from uploaded documents.

Payment Initiation Services (PIS) allow a firm to trigger a payment directly from a customer’s bank account, with their authorisation, without the transaction going through a card network. These are often described as Pay by Bank or account-to-account payments.

Open banking is not screen-scraping. Authorised providers use regulated APIs with explicit customer consent. Always verify that a provider holds a current FCA authorisation and Firm Reference Number at fca.org.uk/register.

17 million — active open banking user connections across consumers and SMEs in the UK as of January 2026, reflecting growing confidence in bank data sharing as a financial tool. (Source: Open Banking Limited / EY, ‘Unlocking the Everyday’, March 2026)

Four practical use cases for property operators

1. Tenant affordability checks

The traditional affordability check relies on payslips and PDF bank statements that take days to collect and are easy to alter. Open banking replaces this with a consented pull of verified income and transaction data drawn directly from the tenant’s bank account. Affordability checks that previously took 3 to 5 working days can complete in minutes.

This strengthens the income and affordability layer of referencing. It does not replace identity checks, credit checks or right-to-rent obligations — those requirements remain in place.

2. Pay by Bank for rent, deposits and holding fees

Pay by Bank payments allow rent, deposits and holding fees to be collected directly from a tenant’s bank account, without the transaction routing through a card network. Account-to-account payment flows — the A2A payments property operators are increasingly evaluating — reduce processing costs and the admin associated with card transactions, particularly for high-value, recurring property payments.

Account-to-account payments do not carry the card scheme chargeback mechanism. Firms should still maintain clear refund and dispute processes, as those obligations remain regardless of payment method.

£1.6bn — potential annual saving for UK businesses from shifting online payments to account-to-account flows, driven by lower processing costs and reduced reconciliation overhead. (Source: Open Banking Limited / EY, ‘Unlocking the Everyday’, March 2026)

3. Source of funds support

Open banking can provide bank-verified account ownership and transaction history as an additional data input into source of funds checks for high-value transactions. This sits alongside — not in place of — a firm’s anti-money laundering obligations. Customer due diligence, risk assessment and record-keeping requirements remain unchanged.

4. Contractor and landlord payouts

Payment APIs and bulk payout workflows allow a firm to distribute payments to multiple recipients — landlords, contractors, service providers — in a single operation, with structured transaction data returned for reconciliation. This removes the repetitive manual steps from multi-party payment runs without changing the underlying logic of who gets paid and when.

£1.4bn — in annual benefit already delivered to UK SMEs through automated bank data feeds and real-time reconciliation — the most mature open banking application currently in production. (Source: Open Banking Limited / EY, ‘Unlocking the Everyday’, March 2026)

Where open banking fits in a proptech platform

For proptech platforms building tenant or buyer journeys, open banking typically integrates at two points: onboarding and payments.

At onboarding, a consented bank data check can verify account ownership, confirm income and support identity or source of funds checks within the same user flow — reducing document uploads and the time to approval.

In the payment flow, Pay by Bank can sit alongside or replace card payment options for deposits, reservation fees and service charges.

Platforms evaluating open banking for real estate should look for infrastructure that supports both bank data access and account-to-account payments from one integration — so that data and payment flows share a single consent journey and audit trail.

What to check before choosing a provider

Before committing to an integration, confirm the following:

- FCA authorisation. Current FCA authorisation and a valid Firm Reference Number (check at fca.org.uk/register)

- AIS and PIS on one licence. Both data access and payment initiation from a single provider

- UK bank coverage. Coverage across major retail and challenger banks

- Consent journey quality. A clear user consent flow with a documented audit trail

- Data minimisation controls. Only the data required for the stated purpose is collected

- Refund and dispute process. Documented, regardless of payment method

- Bulk payout support. If multi-party payment runs are part of the operation

- VRP readiness. Variable Recurring Payments are worth monitoring for rent collection, though availability depends on provider and bank support

Compliance considerations

Open banking changes how data is collected and how payments move. It does not change the regulatory obligations that apply to property businesses.

Estate agents and letting agencies subject to the Money Laundering Regulations must still conduct customer due diligence, maintain records and report suspicious activity. Using bank-verified data as part of a CDD process does not replace any of these requirements.

Data collected via open banking must comply with UK GDPR: collect only what is needed for a specific, documented purpose; do not retain it longer than necessary; and ensure the customer has clear information before they consent.

Affordability decisions informed by open banking data should be consistent, fair and documented.

Open banking infrastructure for real estate: Finexer

Property firms and proptech platforms evaluating open banking need infrastructure that covers both sides of the capability — bank data access and account-to-account payments — under a single FCA-authorised integration.

Finexer is a UK FCA-authorised open banking infrastructure provider (FRN: 925695) offering Account Information Services, account-to-account payments, bulk payouts for UK businesses. For real estate and proptech use cases specifically:

- Tenant affordability checks. Real-time, consented bank data to verify income and financial stability — can reduce parts of the referencing process from days to minutes, depending on the provider workflow and checks required.

- Pay by Bank. Collect rent, deposits and holding fees directly from a tenant’s bank account without card network routing or chargeback exposure.

- Bulk payouts. Distribute payments to landlords, contractors or service providers in a single operation, with structured reconciliation data returned automatically.

- KYB verification. Verify business clients and landlord entities using live bank account data — supporting onboarding and source of funds workflows.

- White-label and embedded options. Integrate the payment or verification flow within your own platform interface.

Where to start

A phased approach is more practical than replacing multiple processes at once:

- Start with affordability checks. Bank-verified income data integrates into existing referencing with minimal disruption and delivers the fastest visible improvement.

- Add Pay by Bank for deposits. Discrete, one-off payments where the cost and dispute reduction is immediate.

- Add account verification for source of funds. Useful for high-value or commercial client onboarding.

- Add rent collection where the tenant journey is digital. Works best in platforms that already manage the tenant relationship end-to-end.

- Add bulk payouts once payment logic is defined. Automate only after the underlying process is correct.

Conclusion

Open banking is moving from a financial services concept into property infrastructure. The data is already showing traction: over 17 million active connections in the UK, £1.4 billion in SME accounting benefits already delivered, and a clear regulatory direction of travel toward wider adoption.

For property operators, the practical starting point is almost always affordability checks — the improvement in referencing speed and data quality is immediate and the integration is contained. For proptech platforms, it is more often embedded payments or onboarding.

In both cases, the goal is the same: less manual document handling, better payment visibility and stronger verification workflows, without adding new regulatory risk.

{kind=link}

{kind=link}

{kind=link}

{kind=link}