The Federal Reserve Just Delivered Terrible News for the Stock Market, but There’s a Silver Lining for Investors

Kevin Warsh wrapped up his first policy meeting as chairman of the Federal Reserve on June 17. He adopted a hawkish tone in his commentary, which left Wall Street mulling the impact of at least one potential interest rate hike by the end of 2026.

Warsh and his colleagues on the Federal Open Market Committee (FOMC) are concerned about the recent spike in inflation. The geopolitical conflict between the U.S. and Iran triggered a sharp spike in oil prices earlier this year, which continues to drive up the cost of every product that travels by truck, boat, or plane.

History suggests rising interest rates are bad for the stock market. In fact, the Fed’s last bout of rate hikes in 2022 and 2023 sent the S&P 500 (^GSPC +1.08%) index plunging into bear territory. However, here’s why the market might avoid a sharp decline this time around.

Image source: Getty Images.

Why the Fed is eyeing interest rate hikes

The conflict between the U.S. and Iran led to the temporary closure of the Strait of Hormuz waterway earlier this year, through which 25% of the world’s seaborne oil transits each day. Iran routinely disrupted commercial shipping lanes to gain leverage in peace negotiations, which sent oil prices soaring. West Texas Intermediate crude hit a peak of $113 per barrel in April, which marked a whopping 97% increase from where it opened in 2026.

It takes time for rising energy costs to filter into economic data, but it’s starting to show up. In May, the Consumer Price Index (CPI) measure of inflation climbed at an annualized rate of 4.2%, more than twice the Fed’s annual target of 2%. This is the first time the CPI has been above 4% since April 2023, and the Fed was raising interest rates back then.

In fact, the federal funds rate (overnight interest rate) was 4.8% in April 2023, which is a full 120 basis points higher than where it is today. The Fed would have to execute five 25-basis-point hikes if it wants to tackle inflation with the same aggression as it did back then — which might be necessary, because it looks like even higher prices could be in the pipeline.

The Producer Price Index (PPI), which measures the change in input costs for businesses, soared at an annualized rate of 6.5% in May, with the energy component exploding by a whopping 36.6%. This laid bare the impact of higher oil prices, and businesses will typically pass at least some of those increased costs on to consumers, so the CPI probably won’t cool in the short term.

In his statement following the June Fed meeting, Warsh clearly said policymakers will deliver price stability, meaning they are focused on bringing the CPI back down to 2%. The central bank’s Summary of Economic Projections (SEP) report for the June quarter showed that almost every FOMC member is now leaning toward at least one interest rate hike before the end of 2026, as they attempt to slow economic activity to bring inflation down.

Rising interest rates are bad for stocks, but there is a silver lining for investors

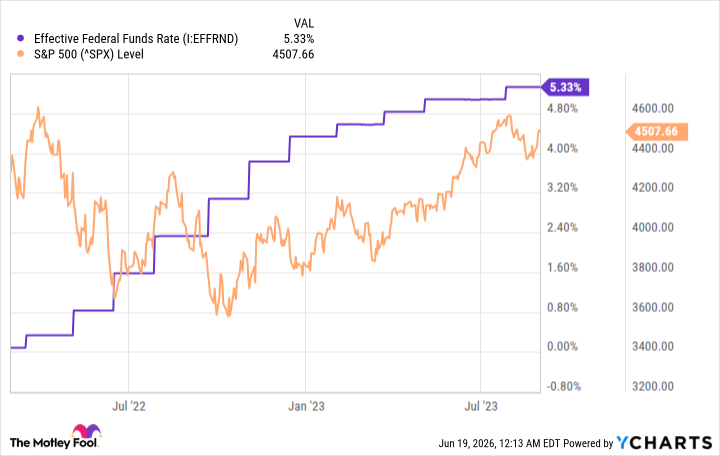

The Fed’s last rate-hiking cycle started in March 2022 and ended in August 2023. It raised the effective federal funds rate from a historic low of 0.1% to 5.3%, and the S&P 500 delivered almost no return during that period. In fact, it spent most of that time in a bear market after plunging more than 20% from its peak.

Effective Federal Funds Rate data by YCharts

Rising interest rates are bad for stocks for a few reasons. They force consumers to allocate more of their household income to debt repayments, leaving them with less money to spend on goods and services. The average business also has a lower borrowing capacity when interest rates rise, which limits its ability to invest in growth. These factors impact corporate earnings, and earnings typically drive stock prices in the long run.

Further, risk-free assets like cash and government Treasury bonds become more attractive when interest rates are high, so fewer investors will pile into growth assets like stocks.

But the current situation has a silver lining. Economic data points like the CPI and the PPI are lagging indicators, meaning they are backward-looking and don’t always reflect the situation in the economy today. The U.S. and Iran recently negotiated a peace deal, and so a barrel of West Texas Intermediate oil trades at just $74 as I write this — significantly below its April peak.

It will take some time before this is reflected in the inflation data, but as long as oil remains at these levels, Warsh and his colleagues might be singing a very different tune in a few months. As a result, I think even one interest rate increase is less likely than the Fed’s recent SEP report suggests.

{kind=link}

{kind=link}

{kind=link}

{kind=link}