There’s one big question that seems to be on the market’s mind: How much is too much when it comes to AI capex?

The concern is evident in the growing split between the shares of the AI trade’s biggest spenders and chipmakers, with chip and other hardware stocks soaring while hyperscalers — which have earmarked billions for AI spend this year — are getting punished by investors.

Despite some selling pressure this week, the Philadelphia Semiconductor Index has continued to move up and to the right, recently posting its best-ever quarter. The chips index was up a record 88% in the second quarter, its best quarterly performance ever.

The performance of the Magnificent Seven, by comparison, has been weak. The Roundhill Magnificent Seven ETF, which tracks the seven tech giants that have collectively surged on a wave of AI hype in recent years, has tumbled from its peak in May.

Every Magnificent Seven stock have lagged the Nasdaq 100’s 16% gain this year, with many down double digits.

The shift appears to have signaled a new chapter for the AI trade, which revolves around one issue in particular: how investors feel about the companies shelling out the big bucks to invest in AI.

“A major trigger for this outperformance has been the spectacular revision in the 2026 plans by hyperscalers,” JPMorgan said of the divergence in stocks this week, pointing to how AI capex spending plans among the largest firms are on track to soar 100% year-over-year.

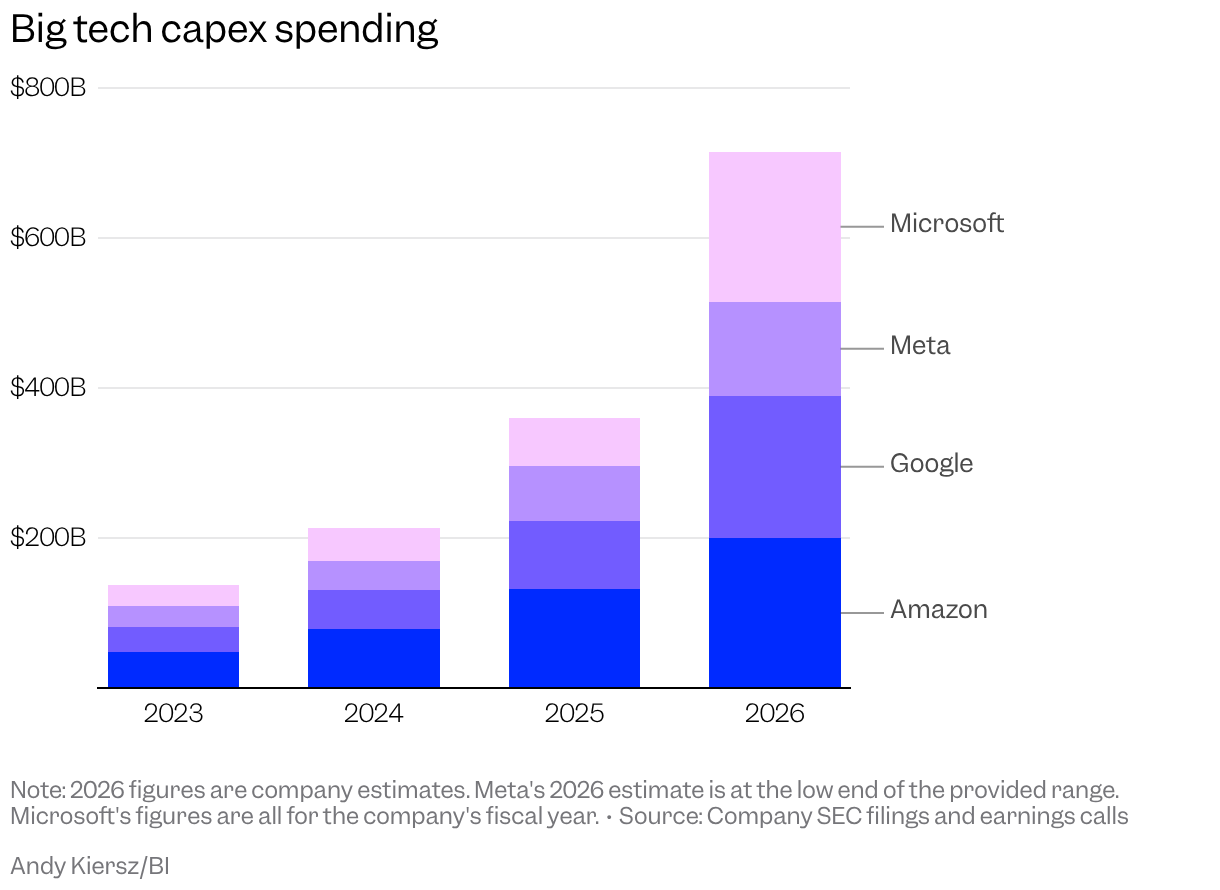

Amazon, Alphabet, Meta, and Microsoft, four of the largest spenders in the AI trade, are on track to spend as much as $725 billion on capex this year alone. By the end of the decade, the four tech giants’ AI capex will likely exceed the GDP of major economies like Japan, according to a projection from Goldman Sachs.

There’s an “intuitive nature” in how markets often rotate from firms that heavily invest in something new, to firms that supply the hardware, Art Hogan, the chief market strategist at B. Riley Wealth Management, told Business Insider. He pointed to a similar pattern that preceded prior market booms, using the analogy of the gold rush, when wealth flowed heavily to those selling shovels and picks, while the prospectors chasing actual gold in the rivers and hills came up mostly empty handed.

“It’s certainly more of an evolution,” he said of the market trend.

The end of the bubble?

Michael M. Santiago/Getty Images

There are some mixed views on what the divergence actually means among Wall Street prognosticators, with some framing the rotation as a positive, while others have floated it as a possible omen for the AI bubble to soon burst.

Strategists at JPMorgan said the divergence looks “somewhat unsustainable,” and floated two possible ways the gap between chip stocks and hyperscalers could narrow.

In the more bullish scenario, hyperscalers see improvement in AI monetization, leading them to “catch up” with chip stocks.

In the bearish scenario, hyperscalers could start to pull back AI capex spending, creating a feedback loop where depressed spending starts to hurt chip stocks.

In a separate note, JPMorgan added that the growing divergence between big spenders and hardware stocks was also seen in markets the months leading up to the dot-com crash.

“The semiconductor trade could come under severe pressure, inducing a more significant and sustained correction in the AI trade,” a team led by Nikolaos Panigirtzoglou wrote on Wednesday, though they added that the bank was leaning toward the more bullish scenario.

Hogan pushed back on the idea that the rotation is an omen for the AI trade, but speculated that more AI firms will likely exit the market in the future as the market narrows its list of true winners in the artificial intelligence race.

“We’ll continue to see the evolution of where the spoils are,” he said. “Right now, it just happens to be in the cohort of memory players,” he added, pointing to blistering rally in memory stocks like Micron Technology and Korea’s SK Hynix in recent months.

Bret Kenwell, an investment and options analyst at eToro, also said he is taking a more agnostic stance on the ongoing rotation, rather than declaring it bullish or bearish outright. It’s not necessarily good or bad for the long-term health of the AI bull market, since investors don’t necessarily need the hyperscalers to keep the trade alive, he told Business Insider.

“Micron just hit a trillion,” he said of the chip maker’s market cap. “From the perspective of if the trade can keep going without the participation of the Mag Seven, without question, it could keep going.”

{kind=link}

{kind=link}

{kind=link}

{kind=link}