The general question I find myself preoccupied with right now is how we think – or fail to think – radical economic change. In other words, how we struggle to understand economic history in the full sense.

This is what my forthcoming book on climate-energy is going to be about.

Another case in point is the question of the global monetary system and, in particular, the question of the future of the dollar system. Even as conventional discourse appears to question the status quo, even as it asks what will succeed the dollar as a world “reserve currency”, the framing of the question obscures its own particular historical conditions. It reifies the idea of a reserve currency and obscures how dynamic the currency and financial system is.

The very idea of a “currency system”, or a “hegemonic currency”, or “reserve currency”, or “lead currency” is, first and foremost, a simplifying and stabilizing notion. In the face of a disorderly and fast-moving world, there is something comforting about asking: “Well … what does history tell us about the future of the dollar system?” At the very least such a question presumes that there is such a thing as the dollar system to talk about.

Indeed, if we start from the assumption that the world economy is organized around “reserve currencies”, we can assemble the world’s economic history into an orderly sequence: From Genoa, to the Netherlands, to Britain, to the US, the reserve currency follow each other in sequence.

It is chronological schematics like this, which then frame the way in which we ask the prospective, forward-looking question: “what comes after the dollar?” There was the sterling system. Now we are in the dollar system. So, what comes next?

But that logic is only compelling if the units being placed in sequence are sufficiently similar to form a series. Was the Dutch commercial or financial system, or that of Genoa, or Spain, or Portugal really similar to that of the 19th century British Empire or the United States in the 20th century? At an elementary level, they were all widely used currencies. But beyond that, such analogies surely obscure as much as they reveal.

Might it be more helpful to think of the history of currencies in the way that we think about technologies. A horse-drawn coach, a steam train, a petrol-powered motor vehicle, a modern high speed train, an EV, are all modes of ground transport. As such they can be placed in a historical sequence. But each innovation does not smoothly replace its predecessors. There are qualitative breaks. At times they coexist side by side. The category of “ground transport” is not meaningless. But, most of us would, surely, agree that at some point in the early 20th century the designation “horseless carriage”, though not exactly false, had outlived its usefulness.

In the same spirit, it is common place to refer to the pound sterling as the predecessor to the dollar as a “reserve currency”. But that conflate quite unlike systems under an overly general rubric. And, even talk of the dollar system, which by common consent began in the middle of the twentieth century, conflates very unlike moments in financial history. Within the dollar era there are phases as distinct as the Model T Ford, a Ford 150 truck and a modern EV.

In a piece published in the FT earlier this week, I argued that in asking about the future of the dollar, we all too easily fall into these traps.

What is the dollar system based on and how will it evolve? As we mark the 250th anniversary of the United States, our ability to realistically address those questions is clouded by all manner of myths. It is commonplace, for instance, to observe that since the second world war, the dollar has replaced the pound as the reserve currency of the world. But if that is true, it is because the dollar system has been repeatedly reinvented. Today, it is once again in a new and volatile configuration, quite different from that of 15 years ago let alone the 1940s. … ….

Here I want to double down. The era of gold-sterling, was quite distinct from what came after. It had relative longevity. A reasonably full accounting of the “dollar system”, by contrast, would suggest that we have been through at least five distinct dollar regimes, each with its own, particular political economy.

My intention in making this point is not to argue for “splitting” against “lumping”, but to insist that we not underestimate the restless dynamic of uneven and combined development. If, as Barry Eichengreen quips in his recent history of money, the successor to the dollar was the dollar, that is because it wasn’t. The dollar before and after 1971 was quite different. The global dollar is not one thing, but something constantly shifting. To take up a phrase suggested by Giovanni Arrighi, what we have to reckon with is the way in which the dollar system has undergone repeated metamorphosis.

The era in which the pound sterling and the City of London and the Bank of England were the dominant players in global finance, was not an era of fiat currency. It was first and foremost the era of the gold standard. It was not sterling as such that was the anchor of the system, but the attachment of the British currency and the unprecedented array of financial connections organized around London, to gold. It was the Bank of England’s management of that peg that established the credibility and durability of the system.

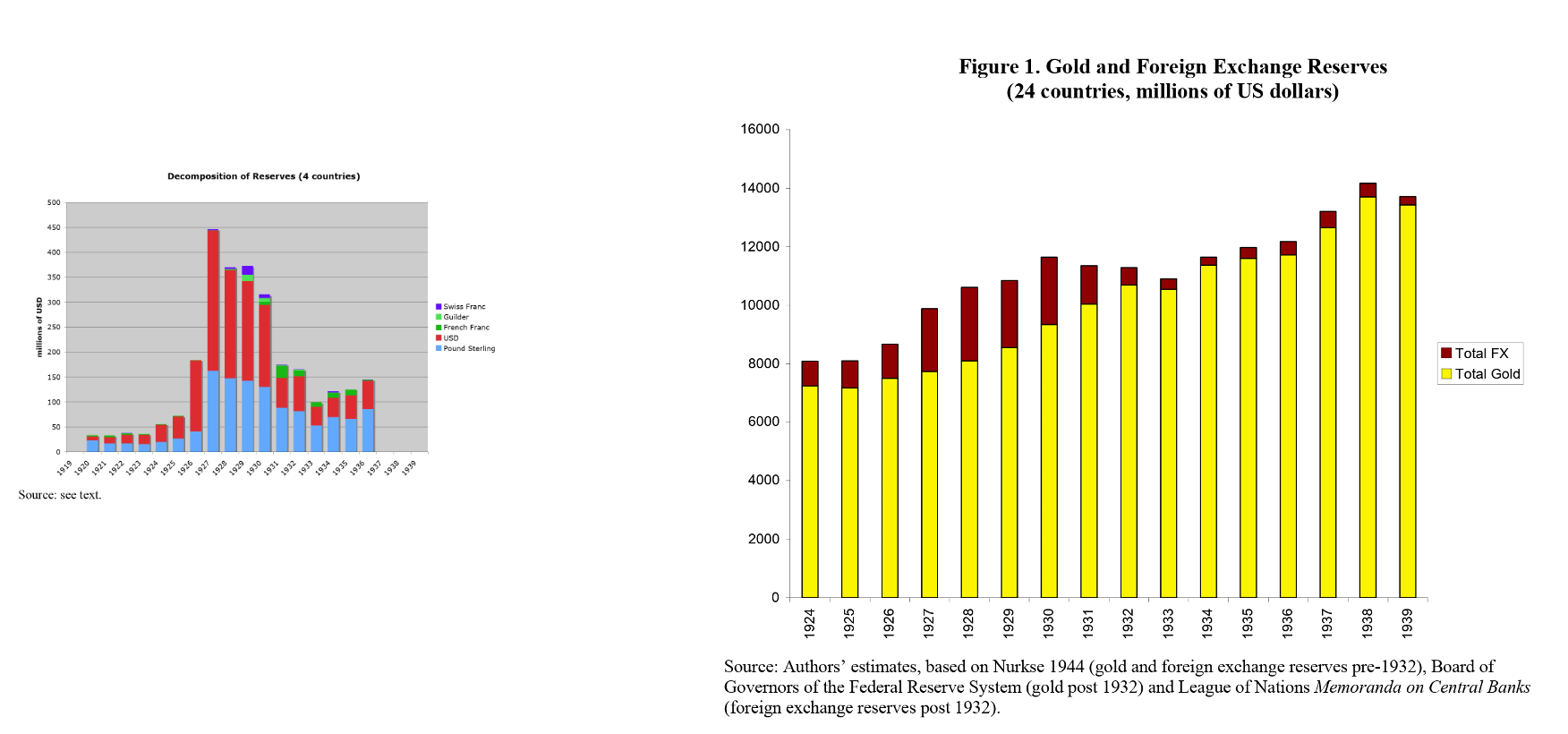

It was only after the fiscal and monetary shock of World War I that currencies – mainly the pound sterling and the US dollar – began to be held as reserves on a large scale, with the US dollar rapidly coming to the fore. But the vast majority of reserves continued to be held as gold. The graph on the left showing the dollar-sterling balance, appears again on the right-hand graph as the thin and dwindling dark-red slither atop a far larger reserve of gold.

Source: Eichengreen and Flandreau

When the Great Depression decoupled first the pound (1931) and then the dollar (1933) from gold, reserve holding of currencies again dwindled to insignificance. But what also became clear is that in extremis, highly sophisticated and dynamic economies, like that of Nazi Germany, could function over long periods with minimal reserve backing and other major currency blocks – like the sterling bloc – could “float” in a managed way.

The truly dollar-centric world began amidst the aftermath of the third great fiscal and monetary shock of the 20th century – World War II. In the 1940s this recentered the non-Communist world on America’s loan program and the Marshall Plan. The Bretton Woods system, though decided on in 1944, was, at first, a failed experiment. From 1944 to 1958, in the aftermath of World War II and the early Cold War, the dollar system was a complex and asymmetric alliance system, with the Europeans operating their own European Payments Union and the British maintaining the sterling zone. This was dollar system #1.

If we ask what configuration of interests within the United States itself sustained this new order, with the USA as the anchor of a newly reconfigured global capitalism, I would point to Leo Panitch and Sam Gindin’s excellent The Making of Global Capitalism: The Political Economy of American Empire, with which I find myself in near total agreement.

Dollar system #2 began in 1958 when the Bretton Woods model finally came into effect. The dollar was anchored on gold and the other major currencies of the American power bloc maintained fixed exchange rates with full convertibility for trade and long-term capital movements. This, however, was no straight forward replacement for the Edwardian golden age. With a far lower degree of globalization in proportional terms, the Bretton Woods system actually set out to mark a deliberate break with what was seen as the anachronistic Edwardian age.

But, though short-term capital movements were regulated, the forces of financial speculation were stirring. By the late 1950s, Wall Street was reviving from its historic defeat in the 1930s Great Depression and began to chafe against the regulatory power conferred on the state by Bretton Woods. The balance of class forces was shifting. By the 1960s the offshore eurodollar market centered around US financial players domiciled in the City of London was in full swing. This and the contrary economic policies of the US, UK, Germany and Japan, made upholding the Bretton Woods system increasingly difficult. The Bretton Woods system – dollar # 2 – was never a robust and solid architecture, analogous to the prewar gold standard. It began to fail almost as soon as it was put into effect. To keep it going the system was given additional support by restricting gold flows and setting up swap lines.

In the early 1970s those efforts failed. Nixon undid the gold peg. This could easily be seen as a humbling defeat for US authority. The international politics of the period – Vietnam, OPEC, NIEO, Soviet advances – certainly were a challenge. But, in the financial sphere, the 1970s and the period that followed – dollar #3, call it the Wall Street dollar – are far better understood as a triumphant period of upsurge by an unfettered Wall Street.

It is with regard to this transition that Eichengreen makes his quip:

But dollar #3 really was not dollar #2. Crucially, the new dollar opened the era of fita currency and that went hand in hand with a phase of explosive globalization. This conjuncture is unlike anything previously seen. Initially, it was unstable. Inflation and balance of payments imbalances led to questions being asked about possible alternatives to the dollar as a lead currency. Those were definitively answered by the interest rate shock delivered in 1979 by Volcker.

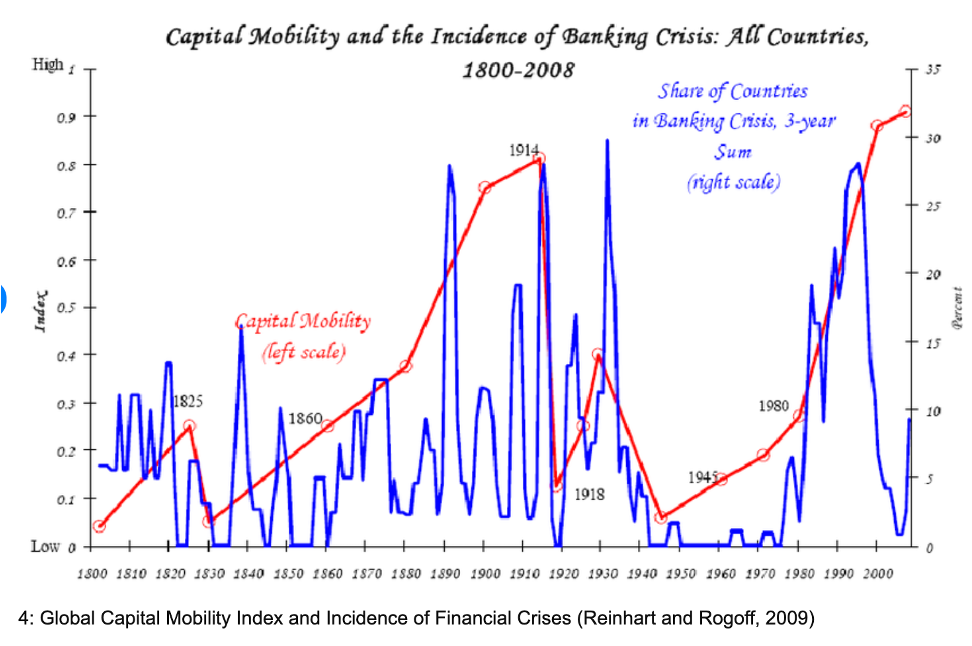

Floating exchange rates and unfettered capital mobility supercharged by the expansion of private finance were now the core of the Washington consensus, with independent central banks replacing the gold anchor as the guardians of stability. The result, after long last, was a return to a regime of capital mobility which matched and even exceeded that before 1914 and a return of financial crises. This is vividly demonstrated by one of the better graphs in Reinhart and Rogoff’s perversely mis-titled bestseller of 2009, This Time is Different.

As waves of financial crises swept the emerging markets in the 1980s, actually existing neoliberalism devolved into a regime of recurring crisis. For all its appeals to discipline and non-discretionary policy, for America’s neoliberal elites, the decades of the third dollar regime (dollar #3) were an era of ad hoc crisis-fighting. In interventions in Latin America, Mexico and the Asian financial crisis, what emerged was a tight nexus between the senior figures of Wall Street, the Fed system and the US Treasury. This was the era in which it became normal for former CEOs of Goldman Sachs to inherit the top job at the Treasury.

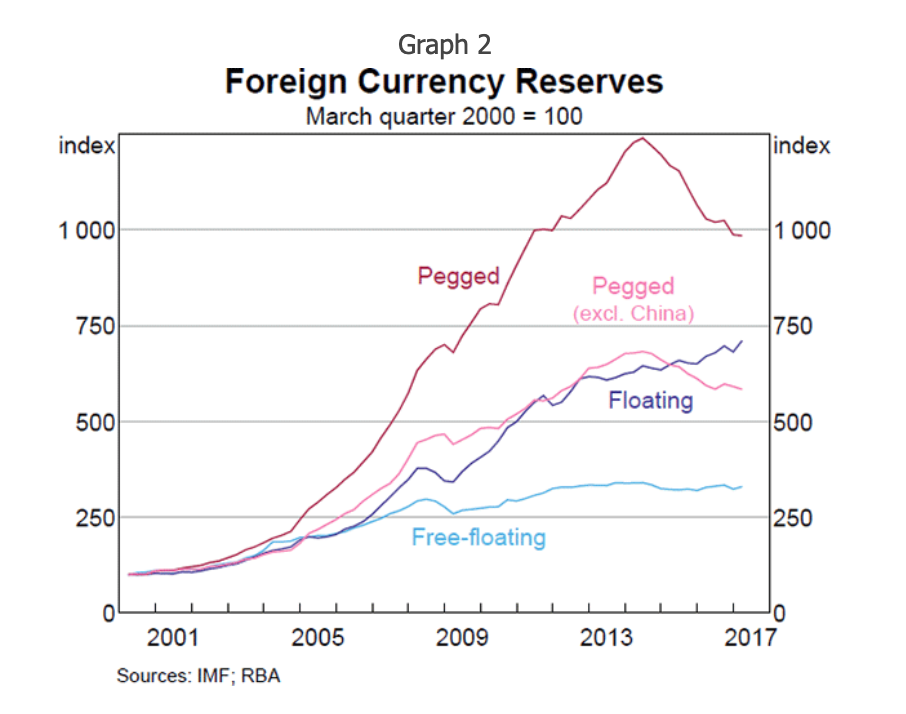

But, if the world was in the end saved from crisis, it had less to do with the daring-do of a posse of Beltway super heroes than a new metamorphosis of the dollar system. The major emerging markets, and above all China, did not want saving. Out of the high-octane danger-world of the Wall Street Dollar (#3), they made a fourth dollar regime – Bretton Woods 2.0. This was defined by a government-directed accumulation of reserves, notably in dollars, above all as a form of self-insurance against financial crisis.

The system was dubbed Bretton Woods 2.0, because emerging markets, having experienced the turmoil of the 1980s and 1990s, pegged their currencies unilaterally against the dollar at competitive rates and then, on the back of their trade surpluses, progressively accumulated reserves.

Source: RBA

This suited exporting businesses in the emerging markets. It offered a degree of security to their governments. Wall Street was only too happy to oblige with the financial intermediation, even if exchange controls hampered the entirely free flow of capital. There was always the prospect that, in due course, China would “converge”.

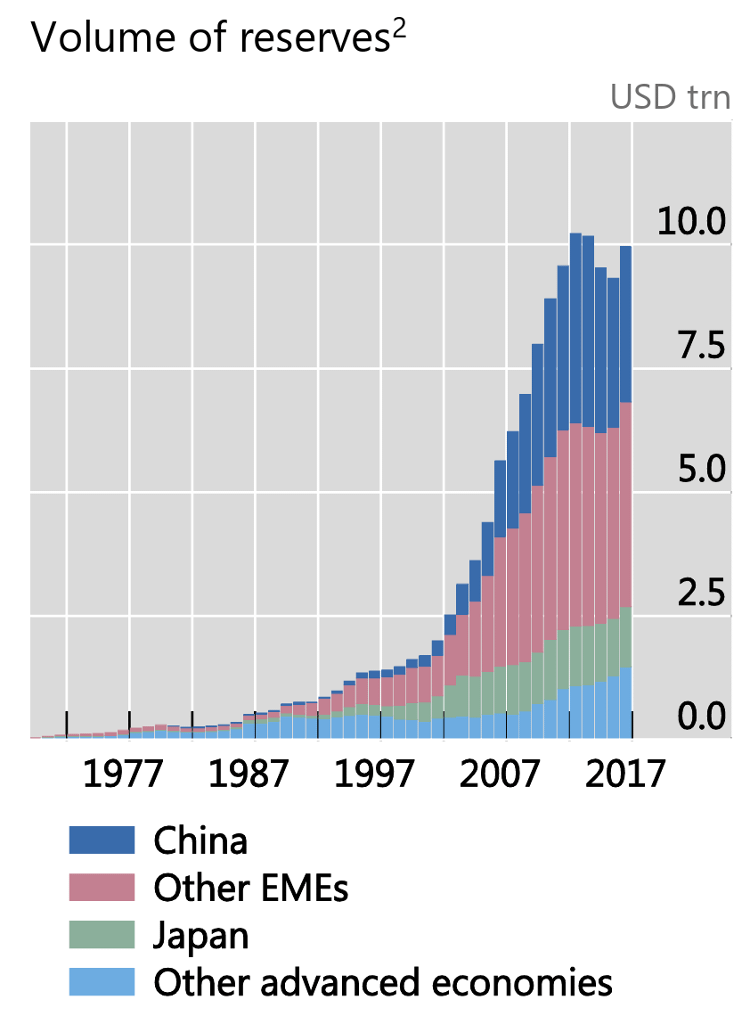

When stacked into an aggregate, we see the dramatic scale of this reserve accumulation. It was from the late 1990s that for the first time the large-scale accumulation of fiat currency, dollar reserves began.

Not all the reserves accumulated were in dollars, but dollars predominated. And they were above all accumulated by official reserve holders in the big Emerging Markets. Bretton Woods 2.0 – dollar #4 – was a world of exorbitant privilege. But one made not by the US, but by the policy choices of the rest of the world and most notably China. The privilege consisted in the ability of the US to borrow at lower interest rates, as foreign holdings of debt piled up. The burden to the US came in the pressure exercised on US domestic producers in exposed sectors and competitors in export markets – China Shock 1.0.

When we ask, who, after sterling and the dollar will come next as a reserve currency, it is this model – Bretton Woods 2.0/ dollar regime #4 – that we project both into the future and past. It was, in fact, very particular to a period that ran, roughly speaking, between 2000 and 2015.

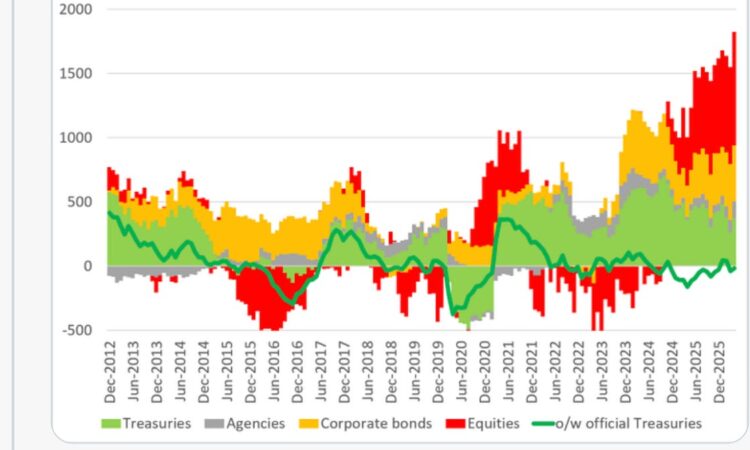

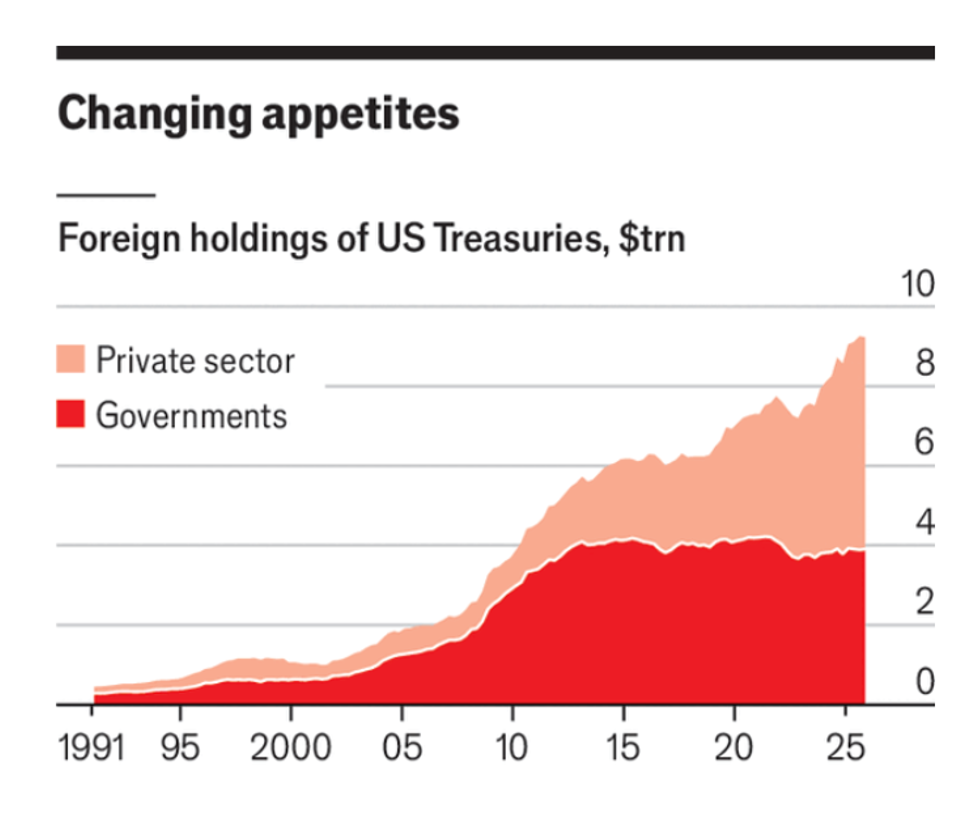

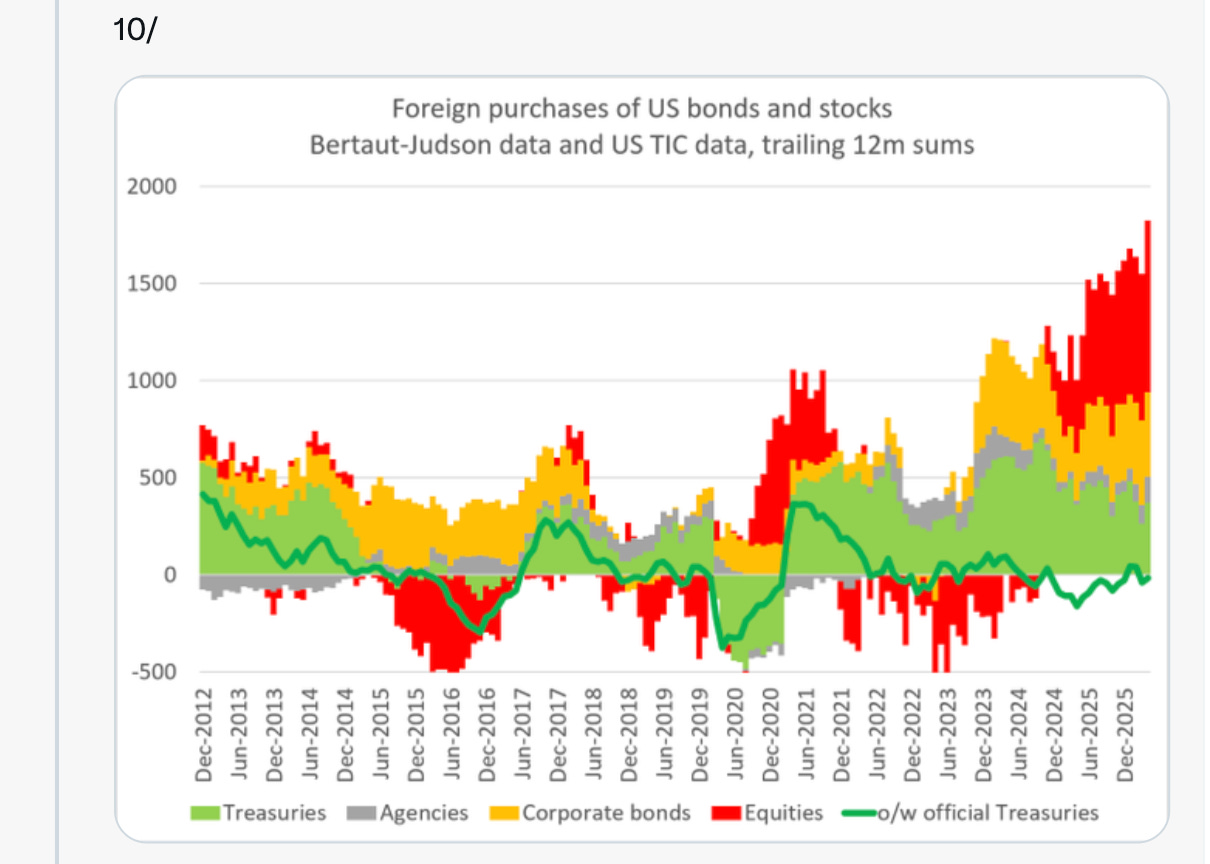

In the mid 2010s the large reserve holders stopped building new official reserves. The emerging markets led by China went on pegging their currencies and controlling capital flows, the trade surpluses continued accumulating, the US went on issuing debt, at an accelerating rate after 2018. But, that debt was no longer being accumulated by official “reserve managers”. Without fanfare, the dollar system was again shifting gear, dollar #4 was giving way to dollar #5. The shift is clearly evident in the figures for foreign holdings of US Treasuries, the key reserve asset.

If in the era of Bretton Woods 2.0, it was official reserve accumulation that covered America’s balance of payments imbalance, it was now inflows of funds into American private assets, attracted by the dramatic dominance of American financial markets over all possible competitors.

US fiscal deficits continue on an unprecedented scale. Foreigners continue to buy Treasuries, but given the huge deficits, these make up a smaller share of total new issuance. These boost demand and corporate profits. That in turn validates foreign investment in those assets. As in Bretton Woods 4.0, the circuit closes, but in a new way.

As I argued in the FT piece

America’s unequal, K-shaped economy is the honeypot of global capitalism. Unlike in the classic phase of Bretton Woods 2.0, it is not China leading the way. Since 2015 Beijing has imposed tight capital controls that trap $50-60tn in Chinese bank accounts behind a financial firewall. Official reserve accumulation is one thing. A private capital exodus from Xi Jinping’s China would be quite another. America’s deficits are financed by inflows from Europe, South Korea, Taiwan and Japan. What then, should we call this latest phase of the dollar system? Bastard Bretton Woods? The hedge fund dollar? Given the latter’s outsized role in Treasury markets, it is tempting. But relative value trades are too technical to really capture the flavour of this era. Discussing the question in Beijing with a Chinese colleague who specialises in Marxist political economy, he remarked that the quality of a currency system is ultimately defined by the class relations that underpin it. In that spirit, perhaps the best label for the current era would be the “billionaire dollar” in honour of President Donald Trump and his shameless self-enrichment. Or perhaps that should be the “trillionaire dollar” after Elon Musk and the SpaceX IPO, which has redefined the parameters of wealth. Certainly, in the current iteration of the dollar system, anyone worrying too much about America’s chronic fiscal incontinence can easily seem out of touch. We aren’t in the 1990s any more. But if that is so, perhaps it is also time to stop speaking of the dollar as a reserve currency, with all its time-honoured connotations of bank vaults, probity and solidity. America’s currency today is, above all, a promise of liquidity and a vehicle for outsized and unfettered capital accumulation:

Dollar #5, is the “profit dollar”.

I love putting out Chartbook. I am particularly pleased that it goes out for free to thousands of subscribers around the world. But, writing this newsletter takes a lot of work. If you are enjoying it and would like to support the project, sign up for one of the subscription options here.

{kind=link}

{kind=link}

{kind=link}

{kind=link}