Summary of key points: –

- The post-war economic growth, inflation and therefore currency scenarios

- The RBNZ’s “hawkish hold” is positive for the Kiwi dollar

- How and when might the NZD/AUD cross-rate turn?

While it is still very fragile and early days in the Iran/US war ceasefire, it is timely to consider how the economic conditions and forces will play out in a post-war environment. The extent of the negative impact on global inflation and GDP growth will only be known over the course of time over coming months. Should the ceasefire stick and the peace talks progress satisfactorily for both sides, there will be hope from the financial markets and the central banks that the oil shock will be short-lived in pushing up inflation and reducing GDP growth.

However, the key measure of how long the negative economic impact will be, will off course be the direction of the oil price.

The West Texas Index crude oil price plummeted into the US$90’s/barrel when Trump perfected another TACO last week and did not go through with his threat to obliterate Iranian civilisation. The oil price has hovered between US$95.00/barrel and US$98.00/barrel over recent days as everyone waits to see if the ceasefire sticks and the oil tankers start sailing through the Strait of Hormuz again. There has certainly been a delay in the Iranians fulfilling the ceasefire condition of fully opening the Strait. Evidence of more ships passing through the strait next week should see further declines in the oil price to near US$90.00/barrel. If this occurs, confidence will return to the markets and central banks that the oil price induced increase in inflation is relatively short-term and can be “looked through” in terms of monetary policy management. It would be negative for US and global economic growth at this time if interest rates were increased on top of households paying much more for their energy/transport. At this point, both the Fed and the RBNZ are taking a cautious “wait and see” approach, hoping that long-term inflationary expectations are not increased by this oil shock caused by President Trump.

Our central theme in respect to foreign exchange price movements (in our recent FX reports) was that the Iran war sell-off in equities, bonds and most currencies against the USD would rapidly reverse once the peak risk point had been passed and there was confidence that the war was coming to an end. The preferred scenario that the war would be over within weeks, not months, looks like it is playing out. The expected reversal, once oil prices started to go down again, in currency markets has been very uneven. However, it is happening, with the NZD/USD exchange rate up 1.5 cents from 0.5700 to 0.5850 over the last week.

Two currencies have already returned to their pre-war levels of late February: –

- The EUR/USD rate is trading back above $1.1700 as the speculative positions to sell the Euro on the commencement of the war are quickly unwound. The EUR/USD rate dropped to a low of $1.1400 on 13th March.

- The AUD/USD rate has returned to 0.7060, not quite back to the 0.7100 level it traded at in mid-February when the RBA was hiking interest rates. The AUD/USD reached a low point of 0.6850 on 30th March.

The Kiwi dollar, the Pound and the USD Dixy Index have, so far, only recovered 50% of the ware-induced sell-off. The NZD/USD exchange rate depreciated three cents from 0.6000 to 0.5700 on the safe-haven buying of the USD when the war started six weeks ago. It has recovered half of that fall to 0.5850. The USD Dixy Index was at 97.00 in late February before the war started. It appreciated to just above 100.00. However, as expected, it ran into resistance at that point from making further gains as the currency speculators were not prepared to go “long” the USD at a 100.00 entry point. The USD Dixy Index has dropped away over the last week from 100.00 to 98.50.

On the proviso that the ceasefire holds and the oil price trends lower towards US$90.00/barrel over coming days/weeks, we would expect the unwinding of USD safe-haven trades to continue, returning the USD Dixy Index to its 97.00 starting point. As the Euro and the Australian dollar have largely unwound their positions, the next phase in currency markets may well see the Canadian dollar, the Pound and the Kiwi dollar catching up to the gains of the EUR and AUD. If the ceasefire falls apart, the catch up by the Kiwi dollar will be delayed.

As we have always stated, the dominant factor on what the duration of the Iranian war would be, was Trump’s political support levels at home. As the political polls moved dramatically against him, Trump was under pressure to find the exit ramp. He created the scenario with the outrageous threats to then accept Iran’s terms for a ceasefire and peace talks. Household affordability and the cost-of-living pressures on middle-and-lower income earners in the US have always been the determining issue for the mid-term elections this November. Trump could not afford gasoline prices at the pump being above US$4.oo/gallon for too long.

The latest University of Michigan survey of US consumer confidence has plummeted in April to a record historic low of 47.6, from 53.3 in March. The lead indicators for US GDP growth and therefore employment growth are certainly far from positive. For these reasons, the US interest rate markets will not be too far away from again pricing-in Fed cuts to interest rates over the balance of this year. In turn, that change should lead to the USD index falling away to 95.00 and below by year-end. Before the war, the Fed was viewing the tariffs as a one-off/temporary impact on inflation that was already passing through and falling out of the annual inflation measure.

Provided the war is indeed at an end, the Fed should also see the oil shock as a one-off as well, and therefore quite quickly return to their interest rate cutting cycle of late last year.

The RBNZ’s “hawkish hold” is positive for the Kiwi dollar

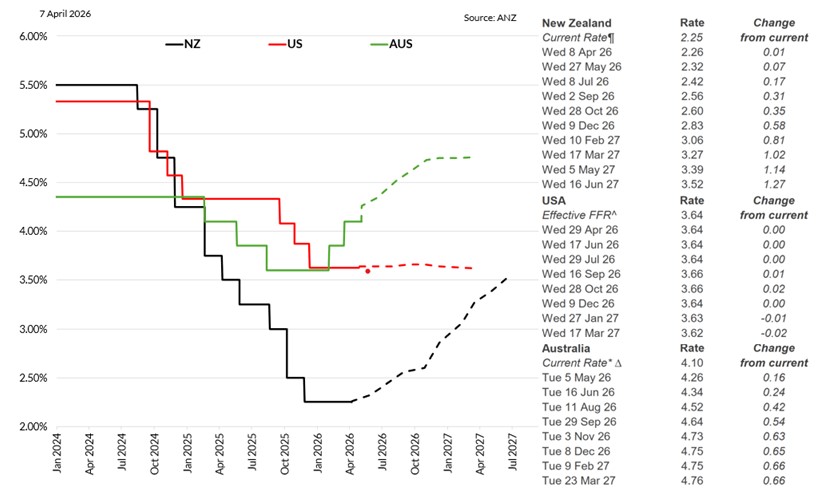

There is a lot more communication and information nowadays from the RBNZ, under the new Governor, in their OCR Review reports than the previous one-pagers that mostly told you nothing new. The take-out from the RBNZ’s messages last week was that they would be prepared to act decisively to raise interest rates if wages and inflationary expectations started to lift from the oil shock. It was certainly a subtle shift from their previous dovish stance that the economy was only in the formative stages of economic growth and there was a stack of spare capacity, therefore few risks to inflation rising. The global landscape is now changed dramatically and the RBNZ have recognised the inflation risks. What the RBNZ will also be forced to recognise over coming months is that non-tradable inflation is a lot stickier around 3.00% than what they have been factoring into their 2026 inflation forecasts. Tradable inflation will also be tracking higher than their estimates. The next inflation read is the March quarter CPI numbers on Tuesday 21st April.

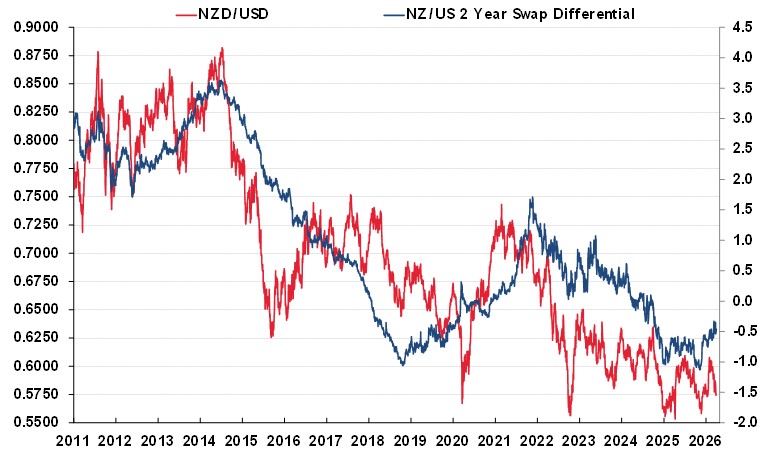

The RBNZ’s statement reinforced our view that there is a growing probability that they will be increasing interest rates from their super low 2.25% OCR base later this year, precisely at the same time that the Fed in the US will be cutting their interest rates. The interest rate differential to the US has already closed up and is set to close some more to zero and then likely positive i.e. NZ two-year interest rates above US two-year interest rates.

The position of monetary policy and therefore the pricing of short-term forward interest rate curves is quite different today between the US and New Zealand to what it was in 2025. Outside of the war impacts (which are arguably similar for both economies in terms of inflation and economic growth), the US economy is slowing, whereas the NZ economy is finally expanding after some tough years.

The chart below displays how the markets are (rightly or wrongly) pricing in successive interest rate hikes for New Zealand and nothing for the US. It should always be remembered that the steep upward sloping forward curve for New Zealand is mostly a mathematical function of our longer-term interest rates moving higher, merely following the US longer term interest rates, and therefore pulling the short-term rates upwards. However, there is also an element of the local market pricing-in the fact that the OCR went too low at 2.25% last year.

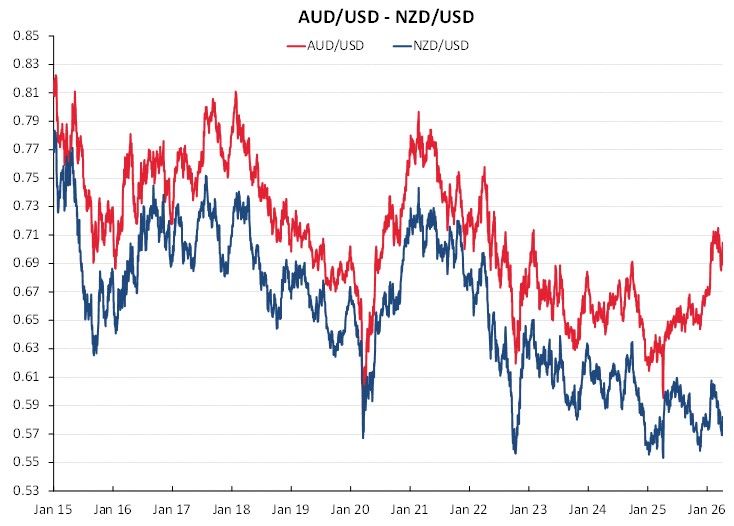

How and when might the NZD/AUD cross-rate turn?

The economic relationship between Australia and New Zealand has always been a close and strong connection. In many ways the economies are similar, the historical difference being that the Aussies rely heavily on metal and mining commodities and our economy is largely based on agricultural commodity exports. In recent years some other stark differences have emerged, notably Australia has experienced strong immigration inflows and house prices rising, New Zealand has experienced neither of those economic tailwinds. As a consequence, Australia never had any recession and New Zealand posted mini recessions until the high export prices kicked in last year. These differences have shown up in the management of monetary policy by the RBNZ and RBA. Australia has expeienced rising inflation and has hiked interest rates in response. In contrast, the RBNZ slashed the OCR to 2.25% and have been forecasting lower inflation in 2026. The immigration/housing trends are different for the two economies; however, they do not represent a fundamental or structural shift in the economic relationship. The two respective monetary policy settings have just become out of synch with each other, the Aussies arguably just six months ahead of New Zealand in terms of timing.

Later this year there is a distinct possibility that New Zealand will be increasing its interest rates, whereas Australia will be finished with that adjustment and their economy will be slowing under the tighter monetary policy conditions. The interest rate differential between the two currencies will be closing up, allowing the NZD/USD exchange rate to catch up on the impressive gains the AUD/USD exchange rate has made over recent months on their interest rate increases.

Picking the bottom of the collapse of the NZD/AUD cross-rate is nigh impossible, however looking ahead, the change in the relative central bank actions would suggest that 0.8200 is as low as the cross-rate goes on this major re-alignment. The reversed economic and monetary policy conditions in the second half of 2026 would suggest a Kiwi dollar recovery and the cross-rate returning to the 0.8700/0.8800 region.

Select chart tabs

*Roger J Kerr is Executive Chairman of Barrington Treasury Services NZ Limited. He has written commentaries on the NZ dollar since 1981.

{kind=link}

{kind=link}

{kind=link}

{kind=link}