In 2013, Morgan Stanley coined the term ‘Fragile Five’ in reference to Brazil, Indonesia, South Africa, Turkey and India. These countries were identified to be vulnerable and likely to face high currency volatility. They either had high inflation, high current account deficit, or high external debt and were thus dependent on external capital flows.

The timing then was fraught as the US Federal Reserve (FED) had begun signaling to the markets that it would slow down (taper’) the pace of its asset purchases (Quantitative Easing). This led to huge volatility in the global financial markets (tantrum’). The logic was that as the FED slows down its asset purchases, it would mean lower liquidity addition and hence less capital flows into emerging markets and riskier assets.

Taper Tantrums and the Fragile Five Label

Countries which depend on external capital flows for their growth or to meet their current account deficits would suffer from the fall out of this ‘taper tantrum’. The impact of ‘taper tantrum’ was most visible in the foreign exchange markets.

Chart 1: How markets traded the ‘Fragile Five’ currencies pre and post ‘Taper Tantrum’

Take a look at the chart above. Indian Rupee against the US Dollar is the dark blue line. The INR first faced a sharp depreciation of over 5% in the summer of 2012. See the dark blue line close to 90 by June 2012, suggesting an almost 10% depreciation. It then appreciated during the year and retraced almost all its losses.

Then as the markets got engulfed in ‘Taper Tantrum’ in May 2013, the Indian Rupee fell by ~18% between May 2013 and August 2013, as can be seen in the sharp drop in the dark blue line as compared to other countries.

Two key moments altered the slope of that line.

From Raghuram Rajan to Narendra Modi: The Road to Stability

In August 2013, Raghuram Rajan was announced to take over as the next RBI governor in September 2013. His welcome speech had many strong comments on India’s outlook, included my favorite “the words India and Crisis should henceforth not be used in the same sentence”. What steadied the rupee from September 2013 was the announcement to tap the Non-Resident Indians with an attractive foreign currency deposit scheme which helped shore up the foreign exchange reserves of the Reserve Bank of India. The RBI raised ~USD 34 billion in the span of two months.

The other key moment was made by the Bharatiya Janata Party (BJP) in announcing Narendra Modi as their Prime Ministerial candidate for the general elections due to be held in April 2024. The United Progressive Alliance (UPA), the alliance by the Congress party, was seen to be facing ‘policy paralysis, riddled with corruption allegations and with the ignominy of the country being clubbed as ‘Fragile Five’, and were rapidly losing public support. Mr. Modi as the next Prime Minister of India seemed appealing to many including to foreign investors.

The INR remained steady against the US dollar from 2014 and crossed the lows of August 2013 in a sustained manner only after September 2018.

The currency movement is of course only the symptom. The issue was in India’s macro-economic parameters.

Despite limited impact on the economy from the Global Financial Crisis (GFC), the UPA government chose to pump prime the economy by keeping fiscal deficit higher than warranted. The RBI ignored persistent high consumer inflation (CPI). The high pace of growth in the decade before boosted income and wealth and thus demand remained strong for goods and (imported) Gold. Oil prices averaged above US$100/rbl between 2011-2014.

The Current Account Deficit (CAD -the difference between what we export and import) rose to well above 3% of GDP. The CAD requires to be funded by external capital flows. This is why Morgan Stanley bracketed India as part of ‘Fragile Five’.

Data Deep-Dive: Comparing the Macro-Economic Decades

| Avg for the period(peak/low during) | 2011-2014 | 2015-2024 | 2025-2026 |

| Real GDP Growth | 6.7%(10.3% / Mar 2011)(4.3% / Mar 2013) | 6.0%(22.6% / Jun 2021)(-23.1% / Jun 2020) | 7.5% (*)(8.4% / Sep 2025)(6,7% / Jun 2025) |

| CPI Inflation | 8.7%(10.6% / Dec 2013)(4.0% / Dec 2014) | 5.0%(7.3% / Jun 2022)(2.2% / Jun 2017) | 2.2%(3.7% / Mar 2025)0.7% / Dec 2025) |

| CAD/GDP | -3.1%(-6.8% / Dec 2012)(-0.2% / Mar 2012) | -1.0%(-3.8% / Sep 2022)(+3.7% / June 2020) | -0.1% (*)(-1.4% / Sep 2025)(+1.3% / Mar 2025) |

| Memo | |||

| Brent Oil Prices ($/brl) | 107.9(118.7 / Mar 2012)(76.4 / Dec 2014) | 66.2(113.8 / June 2022)(29.7 / June 2020) | 71.8(63.6 / Dec 2025)79.7 / Mar 2026) |

| USD / INR | 55.3(44.8 / Mar 2011)(66.0 / Sep 2013) | 72.8(61.8 / Mar 2015(84.7 / Dec 2024) | 88.3(85.3 / Mar 2025)(91.5 / Mar 2026) |

As seen in the table above, the period from 2011 – 2014 was indeed a tough macro-economic situation for India. Much as we can blame the domestic policies, however, we cannot ignore the impact of high oil prices on CAD and inflation.

That impact is visible over the next 10 years shown in the next column. With oil prices averaging ~$66/brl, CPI inflation averaged 5.0% and CAD averaged -1.0% for the entire quarter. Even then, in the quarter where Oil spiked above $100/brl in 2022, CPI climbed to 7% and the current account deteriorated to -3.7% of GDP. This just shows how sensitive India’s macro parameters remain to oil prices.

The 2026 Crisis: Conflict in West Asia and the $100 Oil Spectre

Brent Oil prices shot above US$100/ brl in the month of March 2026. We are already seeing its impact on the INR/USD, on 10-year bond yields and stock market indices.

In 2025, it was capital flows and not current account which was the issue

The conflict in West Asia broke out only on the night of February 28th. It has only been a month of high oil prices, however there is significant uncertainty on the outcome of the war and the trajectory of Oil and Gas prices.

India, as I wrote in my earlier column, has idiosyncratic risks stemming from the conflict and Indian currency and bond yields, although heavily supported by the RBI, are responding to the uncertainty.

The Indian rupee has anyways been the worst performing among many EM and DM currencies. Since 2025, in a period when the US dollar was weak, the INR depreciated against the US dollar. This meant that it depreciated in double digits against the CNY, GBP, EUR.

Even amongst the original ‘Fragile Five’, the INR has been the worst performing.

The Capital Inflow Crisis: Why India Needs a Serious Policy Rethink

In 2011-2013, current account deficit (CAD) was the issue. The government and the RBI had to find ways to attract foreign capital to fund the CAD. It opened up FDI, allowed greater participation for foreigners in the bond market, relaxed non-resident inflows and then opened the special window for non-resident deposits. It also had to allow a substantial depreciation as a natural adjustment and raise interest rates to defend the currency.

Chart 2: Oil prices have just spiked, but the INR is ‘fragile’ already?

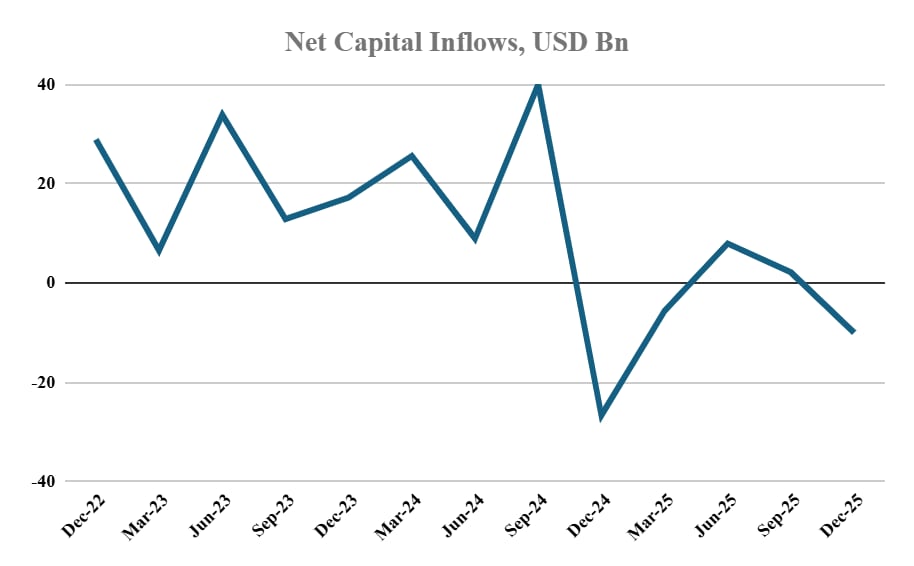

Since 2025, we seem to have an issue with capital inflows. As I wrote over last year, (my two part series on Are foreign investors exiting?, the FDI story, FPI story) and my exhortation to remove capital gains tax on foreign investors; we seem to be struggling to raise capital flows.

From a run rate of average USD 20 billion per quarter, we have moved to negative net flows. When CAD was under control, this was manageable and did not exact a huge pressure on the currency. However, if the tension in the middle east persists and oil and gas prices remain firm, at the current rate of capital inflows, we would have some serious issues in funding the CAD.

Chart 3: India needs a serious policy rethink on attracting global capital flows

India Fragile Again?

India should hope and pray that the situation in middle east resolves itself and that prices and supplies of oil, gas, fertilizers and other important chemicals are normalized.

Other wise in this changed global environment, having a vulnerability to energy imports and a high dependence on capital inflows to fund the current account deficit could leave Indian financial assets fragile again.

Disclaimer:

Arvind Chari is a Chief Investment Strategist and has been with Quantum Advisors India group since 2004. Arvind has over 20 years of experience in long-term India investing across asset classes. Arvind is a thought leader and guides global investors on their India allocation.

This article is for educational and discussion purposes only and is not intended as an offer or solicitation for the purchase or sale of any investment in any jurisdiction. No advice is being offered nor recommendation given and any examples are purely for illustrative purposes. The views expressed contain information that has been derived from publicly available sources that have not been independently verified. No representation or warranty is made as to the accuracy, completeness, or reliability of the information.

The views and opinions expressed in this article are my personal views and should not be construed of the Firm. There is no assurance or guarantee that the historical result is indicative of future results, and the future looking statements are inherently uncertain and cannot assure that the results or developments anticipated will be realized.

{kind=link}

{kind=link}

{kind=link}

{kind=link}