Have President Donald Trump’s Actions in Iran Done Irreparable Damage to the Stock Market? One Data Point Tells the Tale.

For most of President Donald Trump’s tenure in the White House, the stock market has excelled. The widely followed Dow Jones Industrial Average (^DJI 0.56%), benchmark S&P 500 (^GSPC 0.11%), and technology-dominated Nasdaq Composite (^IXIC +0.35%) surged 57%, 70%, and 142%, respectively, during his first term, and were all up by double digits through year one of his second, non-consecutive term.

But pullbacks, stock market corrections, bear markets, and crashes are par for the course when putting your money to work in the world’s greatest wealth creator.

President Trump delivering remarks. Image source: Official White House Photo.

While the stock market has had its share of scares under President Trump (e.g., the five-week COVID-19 crash in February-March 2020 and the one-week tariff tantrum of April 2025), arguably the biggest challenge is yet to come.

Although a two-week ceasefire between the U.S. and Iran sent the Dow, S&P 500, and Nasdaq Composite soaring on Wednesday, April 8, the unfortunate reality for investors is that the damage done to Wall Street from the Iran war may be irreparable.

This may be an insurmountable headwind for a historically pricey stock market

Though the toll on human life is incalculable during war, military conflicts often have far-reaching effects that extend beyond the battlefield. The most notable impact of the Iran war, which began on Feb. 28 at Trump’s command, has been observed in the energy arena.

Shortly after the U.S. and Israel commenced attacks on Iran, the latter closed the Strait of Hormuz to most oil exports. Although this closure remains somewhat fluid, as of this writing on April 8, what can be said with certainty is that, for over a month, we’ve witnessed the largest energy supply disruption in modern history.

In the wake of this virtual closure, crude oil prices have soared. This has led to higher prices at the pump for consumers, as well as steeper transportation and production costs for businesses.

Monthly #PCE inflation data will be released tomorrow. Our #inflation nowcasting model (updated daily!) predicts year-over-year PCE #inflation of 2.67% for February. Check it out: https://t.co/qXCmAZQfCn pic.twitter.com/7pEsoozbHq

— Cleveland Fed (@ClevelandFed) April 8, 2026

Based on the Federal Reserve Bank of Cleveland’s Inflation Nowcasting projections from April 8, the trailing 12-month U.S. inflation rate is estimated to climb from a reported 2.4% in February to 3.56% in April.

While the Trump administration’s negotiated ceasefire with Iran sparked a significant sell-off in crude oil prices last week, energy prices often rocket to the upside during crude oil shocks and fall like a feather once they pass. This is to say that even if this ceasefire holds and military conflict between the U.S. and Iran is over, the pain consumers have felt fueling their vehicles, and the higher expenses businesses are paying to transport and produce goods, aren’t going away anytime soon.

In short, inflationary pressures are likely to be sticky for some time — and that’s a huge problem for a historically pricey stock market.

Image source: Getty Images.

Sticky inflation can be the stock market’s undoing

Although “value” is a subjective term, the stock market entered 2026 as its second-priciest valuation in over 155 years, according to the S&P 500’s Shiller Price-to-Earnings Ratio. The only time the stock market was pricier was in the months leading up to the dot-com bubble bursting, which wiped 49% and 78% off the S&P 500 and Nasdaq Composite, respectively.

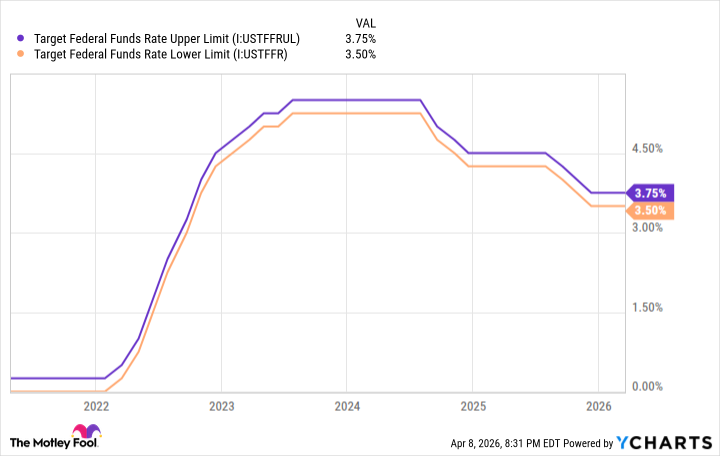

One of the primary reasons the stock market has been able to maintain a premium valuation is the expectation of additional interest rate cuts by the Federal Reserve in 2026. The Federal Open Market Committee (FOMC) — the 12-person body, including Fed Chair Jerome Powell, that oversees the nation’s monetary policy — lowered the federal funds target rate six times since September 2024.

But these rate cuts were made with the assumption that the U.S. inflation rate was heading back to the Fed’s long-term target of 2%. Based on the Cleveland Fed’s inflation projections, the trailing 12-month inflation rate is set to jump by more than one percentage point in two months, and would be closer to 4% than 3%.

Target Federal Funds Rate Upper Limit data by YCharts.

There’s absolutely no incentive for the FOMC to cut interest rates in 2026. In fact, it could be argued that there’s a stronger case for raising interest rates than cutting them at this point.

Even if the FOMC doesn’t go so far as to raise the federal funds target rate, simply taking rate cuts off the table could be enough to devastate a historically expensive stock market that’s been counting on lower lending rates to fuel artificial intelligence (AI), space, and quantum computing investments.

Regardless of when the Iran war ends and/or the Strait of Hormuz is unconditionally reopened, President Trump’s actions will have a lasting (and likely negative) impact on U.S. inflation and the stock market.

{kind=link}

{kind=link}

{kind=link}

{kind=link}