Nvidia (NVDA +2.59%) and Broadcom (AVGO +4.69%) are two of the top AI computing companies to invest in right now. Each of their stocks has done incredibly well over the past few years, with Nvidia up 36% since the start of 2025 and Broadcom up over 50%.

Each stock has risen so much over the past few years that investors may question whether there are any future returns left in the tank. I still think there is plenty to go for these two, but let’s take a look at what history says to determine if they are still solid buys right now.

Image source: Getty Images.

Both companies are growing rapidly

Both Nvidia and Broadcom are competing in the AI computing space. Nvidia is the market leader by far and has done it by offering the best graphics processing units (GPUs) available as well as the system necessary to support them. While GPUs are excellent computing units at nearly every workload they encounter, that flexibility isn’t always needed when workloads become standardized.

In situations like that, clients may choose to work with Broadcom and develop a custom AI chip that focuses only on one workload type. This can provide superior performance in one area, but it fails when tasked with doing work outside of its core competency.

Today’s Change

(4.69%) $16.63

Current Price

$371.54

Key Data Points

Market Cap

$1.8T

Day’s Range

$360.82 – $376.55

52wk Range

$161.61 – $414.61

Volume

1.5M

Avg Vol

27M

Gross Margin

64.96%

Dividend Yield

0.67%

With how much the AI hyperscalers are spending on AI, there is plenty of room for both companies to thrive, and investors don’t need to make a choice on which is the better buy. I own both, because I think both will succeed over the long term. However, right now looks about as good a buying opportunity as investors could hope for.

Each company is seeing incredible growth despite already posting strong results for many years. In its latest quarter, Broadcom’s AI semiconductor revenue rose 106% to $8.4 billion. This division also includes other products, such as connectivity switches, underscoring the strong AI demand. However, by the end of 2027, management expects that its custom AI chips business alone will generate $100 billion or more in revenue. That’s huge growth, and it showcases the rising demand for Broadcom’s custom AI chips.

While its growth is really starting to get going, Nvidia’s is still doing incredibly well. During its past quarter, its growth rate was an impressive 73%. Next quarter, management expects 77% growth. It’s mind-boggling that Nvidia’s growth can be that fast and still accelerating, but that shows how strong AI demand is.

Today’s Change

(2.59%) $4.76

Current Price

$188.67

Key Data Points

Market Cap

$4.6T

Day’s Range

$184.32 – $190.00

52wk Range

$95.04 – $212.19

Volume

5.9M

Avg Vol

179M

Gross Margin

71.07%

Dividend Yield

0.02%

Despite both of these companies growing at incredible paces and showing no signs of weakness, their stocks are still valued at fairly low levels.

Each stock is on sale

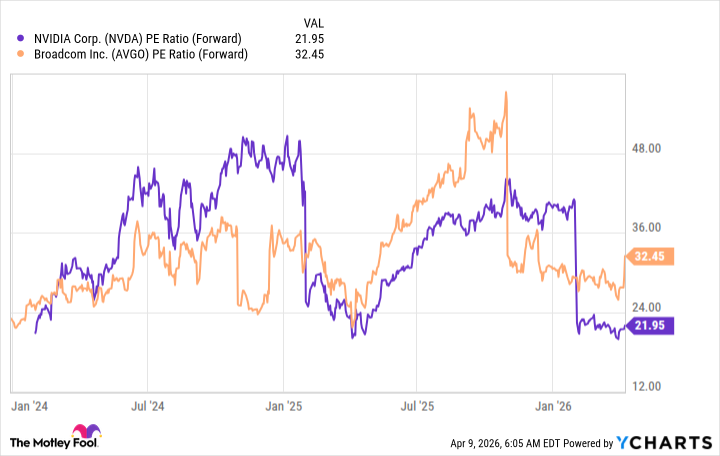

For these two, I think it’s best to zoom in on the past two years, especially since their business makeup has shifted so much from even five years ago. Furthermore, because each company is rapidly growing, it’s best to look at the forward price-to-earnings ratio. From that standpoint, both Broadcom and Nvidia are trading at discounts to their normal levels.

NVDA PE Ratio (Forward) data by YCharts.

Because these two are posting impressive growth rates yet aren’t valued higher, I think right now is an excellent time to buy. Both of these stocks tend to catch fire in the second half of the year (or at least that was the case in 2024 and 2025), and both of them could be fantastic buys right now. Market patterns don’t always repeat, but they tend to echo (especially around the crucial year-end season).

Broadcom and Nvidia will continue to be huge beneficiaries of the billions of dollars being spent on AI. They are among the best buys in the market right now, and investors should be willing to load up on them as long as they can stay patient over the next few years.

{kind=link}

{kind=link}

{kind=link}

{kind=link}