We have a suite of mortgage calculators to help you work out how repayments will affect your household finances, what you could save by remortgaging, and the beneficial impact of overpaying. You can also enter your details here to see what’s available on today’s market

7 August 2025: Rate Cut Expected To Boost Housing Market

House prices rose by 0.4% in July, the biggest monthly increase since January, taking annual price growth to 2.4%, writes Jo Thornhill.

However, the figures from the UK’s biggest mortgage lender, Halifax, show a decrease in annual house price inflation from 2.7% in June.

The average home across the UK is now worth £298,237, down from the record high of £298,815 in January.

Regionally, Northern Ireland continues to be the strongest performing part of the UK, with house price inflation of 9.3% over the past year. Its average property now costs £214,832.

The Bank of England will post its latest decision on interest rates at noon on 7 August. The benchmark Bank Rate is currently 4.25%.

Scotland has also posted strong annual house price growth, increasing by 4.7%, with average prices now at £215,238. Prices in Wales have risen 2.7% year on year, to an average of £227,928.

Among English regions, the North West and Yorkshire and the Humber have the highest rate of property price inflation, up 4.0% over the last year to £242,293 and £215,532 respectively.

The South West, the South East and London continue to see moderate growth, with prices rising by just 0.2%, 0.5%, and 0.5% respectively. The average home in the South West is now worth £302,306 while for the South East the average has hit £388,260.

London remains the most expensive part of the UK, with property prices averaging £539,914.

Jason Tebb at property website OnTheMarket said: “The market continues to demonstrate remarkable resilience, shaking off external economic concerns amid evidence of plenty of activity.

“While the average house price is close to a record high, this is only part of the picture as behind the headline figure are considerable regional variations and differences according to property type.

“Recent Bank Rate cuts have been fundamental in boosting confidence and activity. Further rate reductions will provide much-needed stimulus and boost buyer and seller confidence as we head towards autumn. Further relaxing of criteria by lenders will also help.”

Mark Harris at mortgage broker SPF Private Clients said: “Another cut in interest rates this month should further boost confidence and activity. While inflation remains higher than the Bank of England’s target, wage inflation is slowing and unemployment is rising. However, despite wider economic uncertainties, the picture for potential home buyers remains broadly stable.

“Mortgage rates continue to edge downwards but it’s not just pricing that is improving, with lenders also broadening lending policy, including increasing loan-to-income caps and lowering some income requirements, which is boosting affordability.”

1 August 2025: Market ‘Holding Up’ After Stamp Duty Changes

Average house prices rose 0.6% in July after falling by 0.9% the previous month, according to data from Nationwide building society. The increase takes annual property price inflation to 2.4%, up from 2.1% in June, writes Jo Thornhill.

The value of the average home across the country is £272,664.

Nationwide’s data shows that, despite the change to stamp duty nil rate band thresholds on 1 April 2025, activity has been resilient. Estate agents and mortgage lenders are hopeful of an interest rate cut by the Bank of England on Thursday 7 August.

Robert Gardner, chief economist at Nationwide, said: “Looking through the volatility generated by the end of the stamp duty holiday, activity appears to be holding up well. Indeed, 64,200 mortgages for house purchase were approved in June, broadly in line with the pre-pandemic average, despite the changed interest rate environment.”

Gardner also points out that affordability has been slowly improving as mortgage rates have fallen over the past year, with the house price to earnings ratio, which stands at around 5.75, at its lowest level in more than 10 years.

He said: “After deteriorating markedly in the wake of the pandemic, housing affordability has been steadily improving, thanks to a period of strong income growth alongside more subdued house price growth and a modest fallback in mortgage rates.

“While the price of a typical UK home is around 5.75 times average income, this ratio is well below the all-time high of 6.9 recorded in 2022 and is currently the lowest this ratio has been for over a decade. This is helping to ease deposit constraints for potential buyers, as has an improvement in the availability of higher loan-to-value mortgages.”

Alice Haine, analyst at Bestinvest, said: “Homebuying activity may be picking up, but there are wide variations in price growth across the country. Competition among sellers has also been heating up amid a surge in listings, which may keep a lid on prices.

“If the Bank of England proceeds with a rate cut next week, mortgage rates may ease further, opening up the market for more buyers. The traditional summer surge in listings is another positive for buyers, who can take advantage of a wider range of homes to choose from. It is less of a boon for sellers, however, as it raises the potential for heavier negotiations on price.”

Mark Harris of mortgage broker SPF Private Clients, said: “Lower mortgage rates, with the expectation of more reductions to come, are giving the market impetus and putting borrowers in a stronger position when it comes to negotiating their property purchase. This, in turn, is keeping prices in check.

“With the markets expecting a further rate reduction next week, we could be in for a busy autumn. Lenders continue to trim their mortgage rates, while easing of mortgage lending rules should also enable borrowers to take on bigger mortgages in the coming months.”

Zoopla figures based on Land Registry data for property sales show prices are up 1.3% annually in the year to June. The online property portal also found buyer demand is up 11%, and the number of sales agreed is up 8%, compared to this time last year.

However, there has been a sharp rise in the number of first-time buyers paying stamp duty since the changes in April. Zoopla data shows 41% of FTBs paid stamp duty in June, compared to 19% in March 2025, before the changes.

21 July 2025: Homes For Sale At Decade-High Levels

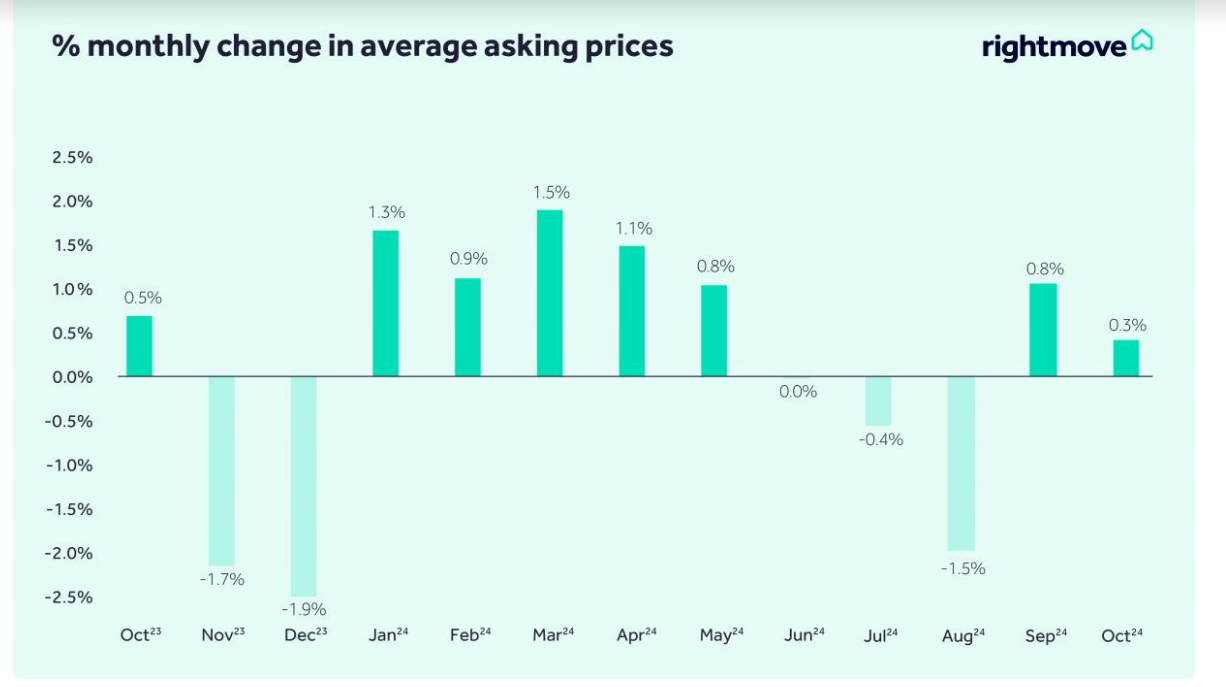

The average price of property coming onto the market fell by 1.2% in July, according to the latest data from property website Rightmove, writes Jo Thornhill.

The drop represents a fall in real terms of £4,531 this month, taking the average asking price across the country to £373,709. It follows an average fall of 0.3% in asking prices in June.

Average asking prices are up a marginal 0.1% annually.

Rightmove has subsequently adjusted down its 2025 forecast for house prices, from a 4% increase over the year, to a rise of just 2%.

London has seen the sharpest fall in asking prices this month, with typical new seller prices down by 1.5%, and the drop increases to 2.1% for inner London. Asking prices in the capital are higher than any other city or region in the country at £684,689.

Prices in the North East of England have shown the most resilience, rising by 1.2% in July to £196,844.

The increase in the number of homes on the market is a major factor acting to suppress price rises. The average stock per estate agent was 65 in July, which is a decade-high level.

Overall market activity is positive, with Rightmove reporting the number of sales being agreed at 5% higher than a year ago. The number of potential buyers contacting estate agents is 6% higher than last year.

Colleen Babcock at Rightmove says it has been a promising first half of the year for buyers and sellers, particularly given changes to stamp duty in April: “Even after the stamp duty deadline, we’re seeing more sales being agreed and more new potential buyers entering the market than at the same time last year. Still, the knock-on effect of high buyer choice is slower price growth.

“Looking ahead to the second half of 2025, there will still very likely be the usual quieter seasonal periods around the summer holidays and Christmas, but we expect market activity to continue to be resilient.

“Crucially, buyer affordability is heading in the right direction, and another two Bank of England Bank Rate cuts before 2026 would be a big boost to this.”

The next Bank of England interest rate announcement is on 7 August.

Rightmove measures asking prices in England, Scotland and Wales. Asking prices fell in every area except the North East of England and East Midlands.

Prices in Scotland fell by 0.4% in July (they are up 2.2% annually) to £199,590. In Wales, average asking prices were down by 0.5% (up 2% annually) to £270,901.

Ryan Etchells at mortgage finance company Together said: “A consecutive monthly fall in house prices confirms what we’ve been seeing: it’s a buyer’s market. What may have been interpreted as a blip following the increase in stamp duty in April could be a more prolonged period of subdued activity.

“While mortgage rates have reduced slightly in recent months, stubborn inflation and high stamp duty may well be holding back buyers, who are waiting to see what will happen to mortgage rates. All eyes will be on the next Bank of England interest rate decision, with many experts predicting a cut.

“However, subdued house prices may present an excellent opportunity for aspiring homebuyers, as well as landlords looking to grow their portfolios.”

And Jeremy Leaf, a London-based estate agent, said: “Sales are still being agreed but nearly always with sellers who have recognised the importance of setting a realistic initial figure to differentiate themselves from so much other, often similar, property.

“Otherwise, buyers will take even more time waiting for the ‘right’ property and perhaps worrying about the possibility of autumn tax rises despite improving affordability – including the likelihood of imminent mortgage rate cuts.”

16 July 2025: Mortgage Rate Cuts ‘Boost Confidence’

House prices rose by 3.9% in the year to May, according to data from the Office for National Statistics (ONS), writes Jo Thornhill.

The rise, which included a 1.1% monthly increase in May, takes the average UK house price to £269,000 – £10,000 higher than 12 months ago.

The official figures, based on completed sales across the UK, show prices are up 3.4% in England (where the average house price now stands at £290,395), 5.1% in Wales (£209,580), and 6.4% in Scotland (£191,927). The average house price in Northern Ireland increased in the year to quarter one of 2025 (January to March) to £185,000, a rise of 9.5%.

Property market experts say the data is encouraging given the changes to Stamp Duty in England and Northern Ireland in April, which mean more buyers are paying higher levels of the tax when purchasing property.

Lower mortgage rates, however, are counteracting higher tax costs by boosting both buyer and seller confidence. Additionally, more lenders have been able to relax their income-to-loan ratios thanks to new guidelines from the financial regulator, which should help more first-time buyers onto the housing ladder.

Mortgage brokers are also hopeful there could be another interest rate cut by the Bank of England in August (the next rate decision is on 7 August), which would further fuel property market activity.

The only dampener on falling rates could be the rate of inflation, currently at 3.6%, which remains stubbornly higher than the Bank of England’s target of 2%.

Jason Tebb, president at property portal OnTheMarket, said: “The market continues to demonstrate remarkable resilience, assisted by four interest rate reductions since last August. These cuts, with the suggestion of more to come, have boosted buyer and seller confidence, increasing activity and benefiting the wider economy.

“The unexpected increase in inflation to 3.6 per cent in June may persuade the Bank of England to pause with regard to further reductions, although much depends on other economic data such as the jobs market.

“With mortgage lending rules being relaxed to assist buyers with affordability and boost first-time buyer numbers, there is recognition that it is a struggle to get on the housing ladder, but only time will tell if these measures are enough to make a real difference.”

Mark Harris, chief executive of mortgage broker SPF Private Clients, said: “Rate reductions have been playing their part in encouraging buyers and sellers to take the plunge, and the markets still expect a further cut in Bank Rate next month, even though inflation ticked up in June.

“Lenders have plenty of liquidity and are keen to lend, with mortgage rates fairly steady on the whole, while some lenders continue to reduce fixed rates.”

Amy Reynolds at Richmond estate agent Antony Roberts said: “The market continues to surprise. While headlines paint a gloomy picture, the reality on the ground is far more nuanced. June was a record month for us in terms of newly-agreed deals, and July has started strongly for exchanges.

“That said, fall-throughs were also high in June – it’s very much a tale of two halves.”

7 July 2025: Relaxation Of Lending Rules Boosting Activity

- House price growth flat in June (0% change)

- Annual growth stable at 2.5%

- First-time buyers back to pre-stamp duty change levels

House prices were flat in June showing a 0% change, compared to a drop of 0.3% in May, according to the latest data from the UK’s largest mortgage lender, Halifax.

Annual growth in prices is relatively stable, recorded at 2.5% in June, down from 2.6% in May, although prices dropped marginally by 0.3% during the second quarter of the year between April and June.

Halifax puts the price of the average UK property in in June at £296,665.

First-time buyer numbers are also back to levels seen before the increase in nil-rate stamp duty thresholds on 1 April in England and Northern Ireland, said the lender.

The changes, which had led to a drop-off in the number of house hunters in April, pushed more buyers into paying the property tax when purchasing a home.

But new regulatory guidance in ‘stress test’ rates – which checks what a borrower could afford at higher rates of interest than offered by their mortgage deal – has enabled lenders to take a more flexible approach to affordability, which is boosting the number of buyers.

Amanda Bryden, head of mortgages at Halifax, said: “Over the last two months, we’ve already helped an additional 3,000 buyers – including more than 1,000 first-time buyers – access a mortgage they wouldn’t have qualified for before.”

As also reported by Nationwide (see story below), Northern Ireland continues to record the fastest pace of annual price growth. Average property prices in the country have risen by 9.6% in the past year, taking the value of a typical home to £212,189.

Prices in Scotland are also showing strength, up by 4.9% annually to an average of £214,891. While prices in Wales are up by 3.9% year on year to £229,622.

Within England, the North West region has posted the highest rate of property price inflation, up 4.4% over the last year to £241,938.

The South West and London continue to see more subdued growth, with prices rising by just 0.5% and 0.6% respectively. However, the capital remains by far the most expensive part of the UK, with the average home now priced at £540,048.

The average property value in the South West is now at £303,271.

Mark Harris, chief executive at mortgage broker SPF Private Clients, said that lower mortgage rates and the easing of lending criteria has helped the market in recent months. He commented: “If interest rates fall further, as expected, this will give a further boost to activity and transactions later in the year.”

1 July 2025: End Of Stamp Duty Concessions Cools Market

- June average price slips 0.8% month-on-month

- Annual inflation slows to 2.1% from 3.5% in May

- N Ireland top-performing region with 9.7% annual growth

The annual rate of UK house price growth fell to 2.1% in June, from 3.5% in May, as April’s changes to stamp duty bedded into the market, write Laura Howard and Jo Thornhill.

Nationwide, the UK’s largest building society, said June’s softening in price growth may reflect weaker demand following the increase to the stamp duty nil-rate bands.

It puts the cost of an average UK property in June at £271,619 compared to £273,427 in May, a fall of 0.8%.

In addition to increased stamp duty for buyers, the market is also working against a global backdrop of economic uncertainty, with a question mark over future interest rate cuts.

The Bank of England has made two cuts so far this year to its Bank Rate – the driving force in determining the cost of mortgages – but inflationary pressures have paused any further reductions in the immediate future.

However, Nationwide says it still expects housing market activity to pick up during the summer, with ‘underlying conditions for potential homebuyers remaining supportive’.

Robert Gardner, Nationwide’s chief economist, said: “The unemployment rate remains low, earnings are rising at a healthy pace in real terms (ie, after accounting for inflation), household balance sheets are strong and borrowing costs are likely to moderate a little if Bank Rate is lowered further in the coming quarters as we, and most other analysts, expect.”

Northern Ireland remained the strongest performing region, with annual price growth of 9.7% in June. However, the growth is still under the 13.5% posted for quarter one of 2025. Scotland recorded a 4.5% annual rise, while Wales saw a 2.6% increase.

Across England prices were up 2.5% annually in June, marking a slight softening from the 3.3% annual rise seen over Q1 as a whole.

Average prices in Northern England (North, North West, Yorkshire & The Humber, East Midlands and West Midlands) were up 3.1% year-on-year, while those in Southern England (South West, Outer South East, Outer Metropolitan, London and East Anglia) were up 2.2%.

Within England, the North was the top-performing region, with prices up 5.5%. East Anglia was the weakest performer with annual growth of 1.1%.

Jonathan Hopper, chief executive of Garrington Property Finders, said: “If this trajectory continues, as we expect, the summer months may bring a series of increasingly visible price softening moments, driven not by panic, but by pragmatism.

“Sellers are being forced to adapt to a new normal, and the market data is beginning to reflect this sharp recalibration.”

Separate data from Zoopla’s June house price index also points to a slight slowing of house price rises. It shows annual house price inflation was up by 1.4% in the year to May, but the annual figure was running at 1.6% in both April and March.

Zoopla puts the cost of the average home in the UK at £268,400, in what its experts describe as a ‘steady’ market.

Despite cooling prices, the number of sales being agreed is at its highest in four years, with the number of sales agreed in the four weeks up to 16 June 6% higher than the same period last year.

The number of properties on the market is 14% higher than a year ago, said Zoopla, and the higher volume of supply is also likely to be having a dampening effect on prices.

Zoopla says house price growth is highest in areas where the average property is worth £200,000 or less, where affordability may be less of a constraint. Prices in these areas have risen by 2.7%, on average, in the year to May 2025.

In contrast, areas with higher value homes (where the property average is at £500,000 or more) have seen prices fall by 0.2% in the past year.

18 June 2025: First Slowing Of Annual Inflation Since 2023

- Tax overhaul takes heat out of market

- Annual inflation halves to 3.5%

- Average UK home worth £265,000

Average house prices fell 2.7% month-on-month in April as new nil rate bands for stamp duty kicked in at the beginning of the month, writes Jo Thornhill.

The figures from the Office for National Statistics (ONS), which uses Land Registry data based on completed sales, show prices up by 3.5% annually for the year to April. This is a marked fall compared to the 7% annual increase in March.

The ONS says it is the first slowing of annual house price inflation since December 2023. It ‘coincided with Stamp Duty Land Tax (SDLT) changes’ which came into force for England and Northern Ireland on 1 April. The reduction in the nil rate bands for stamp duty means many home buyers will pay more in tax.

House prices have risen the most in Northern Ireland, where they are up by 9.5% in the year to the end of Q1 2025 (end of March). The average home in the country is now worth £185,037.

Prices are up by 5.8% annually in Scotland, to an average value of £191,061, closely followed by an increase of 5.3% for Wales to £210,077.

Average values have risen by the slowest amount – by 3% in the year to April – in England, taking a typical home to a value of £286,327. The average home across the whole of the UK is now worth £265,000.

Detached properties have seen the biggest annual increases, rising by 5% in the year to April to an average value of £436,380 nationally. Flats rose by 0.6% during the same time to an average of £195,017.

Commenting on the ONS data, Amy Reynolds, head of sales at London estate agent Antony Roberts, said: “A modest uptick in prices is to be expected given that the spring/summer market is traditionally when people move and the market is at its busiest. Unfortunately, another interest rate cut this week is unlikely given today’s inflation figure, which is disappointing as a half-point cut would stimulate growth.

“However, there’s still plenty of money and desire to buy in the core price ranges. Surprisingly, we are seeing a rise in first-time buyer activity even though the stamp duty holiday has ended. Many are receiving help from family and are likely being driven by the pressures in the rental market, where demand far exceeds supply and rental listings have dropped sharply as landlords exit the sector.”

Nathan Emerson at estate agent trade body Propertymark said: “The first half of 2025 has proven very different from the expected trends we would normally witness within the housing market each year.

“We had the effect of stamp duty threshold changes across England and Northern Ireland completely alter consumer habits. The housing market witnessed a sizable uplift in both mortgage approvals and property transactions, as many people looked to complete on their purchase before the April deadline.

“As we progress further into the traditionally busy summer period, we are likely to see momentum regarding house prices. However, this will likely depend on consumer affordability and confidence.”

The government has announced the launch of a publicly-owned and taxpayer-funded National Housing Bank, to ‘turbo-charge’ its target of building 1.5 million new homes over the next five years.

The Housing Bank, a subsidiary of Homes England, the government’s housing agency, will be able to act in partnership with the private house building sector, offering up to £22bn in loans for development of new sites and projects.

16 June 2025: Buyers’ Market Sees Demand And Sales Rise

- Asking prices slide 0.3% in June

- Average asking price up 0.8% year on year

- Sales agreed up 6% annually

New seller asking prices dropped in June by 0.3% on average (down £1,277 in real terms), taking annual asking price house inflation to just 0.8%, writes Jo Thornhill.

The changes, drawn from Rightmove data, take the average asking price across the country to £378,240.

A June asking price dip is unusual, but Rightmove says many new sellers are lowering their price expectations due to competition, with more properties coming to market. According to the property portal, the number of properties for sale is the highest for a decade.

Buyer activity appears resilient, fuelled by falling mortgage rates, increased choice and stable asking prices.

May saw the highest number of sales agreed in any month since March 2022, with the number also up 6% on 2024. Demand is now 3% ahead of this time last year, while the number of homes coming to market is 11% higher.

Regional variations remain pronounced. Previously over-heated markets in London/South East and South West, where average asking prices outstrip the national average, saw the biggest monthly fall.

Prices fell by 1.6% in the South West, taking the average new asking price to £391,885. They were down 1% in the South East to £492,538, while in London they dipped by 0.9%, taking average prices to £695,414, the highest in any region.

Asking prices in the North West, Wales and Yorkshire & The Humber regions have risen the fastest this month.

Prices in Wales rose 0.4% in June, taking the average asking price to £272,381. In Yorkshire & The Humber, prices rose 0.2% to an average of 258,839, while in the North West prices were up 0.9%, the highest monthly rise of any region, to £272,388.

Colleen Babcock at Rightmove said: “We’re now seeing the decade-high level of homes for sale and the recent stamp duty increases have a delayed impact on new sellers’ pricing. Prices have fallen after the records set in April and May.

“Agents have been telling us that sellers need to set a competitive price to have a better chance of finding a buyer, and it looks like many are responding to that message.”

Jeremy Leaf, a London estate agent, said: “The amount of unsold stock is rising and transaction numbers are falling.

“However, the overwhelming majority of agreed sales are holding, although some prices are softening. We are telling sellers who are also buyers but who are receiving little or no interest in their properties, to concentrate on the difference between the two and reduce closer to their bottom line while still leaving room for negotiation.

“New sellers, particularly of flats, need to recognise quickly the buyers’ market conditions and price to stand out from the crowd.”

5 June 2025: Northern Ireland Roars Ahead But London Subdued

- Prices edge down 0.4% in May

- Average values up 2.5% year-on-year

- Typical home worth £296,648

Average house prices increased by 2.5% in the last 12 months, according to Halifax, the UK’s biggest mortgage lender, despite a dip of 0.4% in May.

The value of the average home across the UK stands at £296,648, down from £297,798 in April. In May last year, the average stood at £288,688.

Despite May’s dip, Halifax says the housing market remains stable. Amanda Bryden, head of mortgages at the bank, said: “Average prices fell by 0.4% in May – a drop of around £1,150 – following a modest rise in April.

“These small monthly movements point to a housing market that has remained largely stable, with average prices down by just 0.2% since the start of the year. The market appears to have absorbed the temporary surge in activity over spring, which was driven by the changes to stamp duty.”

Halifax says the outlook for the market in 2025 will depend to a large extent on what happens with interest rates. While the Bank of England cut the benchmark Bank Rate from 4.5% to 4.25% in May, experts are uncertain how far or how quickly it could continue to cut rates this year, as inflation remains stubbornly high.

The next Bank Rate decision is on 19 June.

Regionally, Northern Ireland continues to see the fastest pace of annual property price inflation at 8.6%. The typical home there now costs £209,388, though prices remain well below the UK average.

Wales and Scotland posted strong annual growth of 4.8% in May. Average prices now stand at £230,405 and £214,864 respectively.

Among the English regions, the North West and Yorkshire and the Humber have seen the biggest increases in average prices at 3.7%. The average home in the North West is now worth £240,823, while in Yorkshire it stands at £213,983.

In contrast, London continues to see more subdued growth, with prices rising by just 1.2% in the year to May. The capital has by far the most expensive house prices of any part of the UK with the average property now valued at £542,017.

Jason Tebb at property portal OnTheMarket said: “The market continues to demonstrate remarkable resilience, shaking off external economic concerns.

“Recent cuts to interest rates have been fundamental in boosting confidence and activity. Further rate reductions from the Bank of England will provide much-needed stimulus for the market as the year progresses. Affordability continues to impact what buyers are able or willing to pay.”

Holly Tomlinson, a financial planner at Quilter, said: “The latest Halifax index shows that, while activity has slowed, the market remains surprisingly robust.

“Following the changes to stamp duty thresholds in April, the market saw a clear shift in momentum. Buyers rushed to complete transactions in March to avoid higher tax bills, but activity cooled noticeably in April. Despite this drop in demand, house prices have not fallen off a cliff.

“The fact that prices fell only modestly in May indicates that supply remains constrained and sellers have not yet been forced to adjust their expectations. However, with affordability still stretched and borrowing costs relatively high, the risk of a more prolonged slowdown cannot be ignored.

“Mortgage rates are edging down slightly but for many buyers, this remains a far cry from the ultra-low rates of recent years. For those coming to the end of a fixed deal, the jump in monthly repayments can be significant, adding to the financial strain.

“Looking ahead, market confidence will likely hinge on the timing and pace of interest rate cuts. A more meaningful pick-up in buyer demand may not materialise until there is clearer evidence that mortgage costs are on a sustained downward path. For now, the market appears to be pausing for breath after a frenetic start to the year.”

2 June 2025: Homes In Rural Areas See Biggest Jump In Values

- Average prices up 0.5% last month

- 3.5% annual rise from 3.4% in April

- Typical home worth £273,427

Average house prices rose 0.5% in May, taking the annual rate of increase to 3.5%, according to the latest figures from Nationwide building society.

The lender, which increased its share of the mortgage market from 12.3% to 16.2% in the past year, says the average UK home is now worth £273,427.

Homes in rural areas have risen by 23% in the past five years, compared to an average of 18% for other areas, according to Nationwide, with rural semi-detached properties seeing the biggest price rises.

Nationwide chief economist Robert Gardner said: “Mortgage approvals data suggests that market activity appears to be holding up well following the end of the stamp duty holiday. Despite wider economic uncertainties in the global economy, underlying conditions for potential home buyers in the UK remain supportive.

“Unemployment remains low, earnings are rising at a healthy pace, even after accounting for inflation, household balance sheets are strong and borrowing costs are likely to moderate a little if Bank Rate is lowered further in the coming quarters as we, and most other analysts, expect.”

Data published by Zoopla shows house prices are up by 1.6% annually to an average value of £268,250. The online property portal says it was the busiest May for home sales agreed since the 2021 pandemic.

Mark Harris, chief executive of mortgage broker SPF Private Clients, said: “Last month’s interest rate cut from the Bank of England gave the housing market and wider economy a timely boost following the end of the stamp duty concession.

“Lenders have been reducing mortgage rates and enhancing loan-to-income ratios, increasing the size of loan that some borrowers can access. However, while the borrowing environment may be easing, higher inflation and the wider economic picture remains a concern, which could mean the pace and size of further base rate reductions is more gradual than markets thought only a few weeks ago.”

David Johnson, managing director of property consultancy INHOUS, said: “Buyer demand picked up immediately after the bank holidays and has remained strong throughout May. This level of buyer motivation has resulted in the majority of sellers receiving multiple offers and achieving their asking price. One and two-bedroom apartments remain particularly sought-after, as well as larger family homes in and around commuter hotspots.”

Mortgage approvals for house purchase fell by 3,100 to 60,500 in April, according to the latest data from the Bank of England’s Money and Credit report. The figures are unsurprising given the lowering of stamp duty thresholds on 1 April, which means many buyers will pay more in the tax.

21 May 2025: Longer-Term Outlook ‘Cautious’

Average house prices increased by 6.4% – or £16,000 in real terms – in the year to March, according to the latest government data, writes Jo Thornhill.

It takes the value of the average UK home to £271,000, according to the Office for National Statistics (ONS), which uses Land Registry data from completed residential sale prices.

The March rise is up on the 5.5% annual increase recorded in February. However, market experts believe the road ahead could be bumpy for mortgage rates following a sharp rise in inflation to 3.5% in April, which will add a dose of caution to the market.

It means interest rates may not fall as quickly as many borrowers hoped, as the Bank of England uses Bank Rate to control rising inflation.

Jeremy Leaf, north London estate agent and a former RICS residential chairman, commented: “At first glance, the ONS figures demonstrate market resilience with activity shrugging off recent economic uncertainties at home and abroad. However, on the ground we are seeing a different story.

“Although this is the most comprehensive of all the housing market surveys, as it includes mortgaged and cash transactions, these numbers reflect activity and pricing over the past few months.

“In the past month or so, many buyers and sellers are pressing the pause button and sitting on their hands. The recent cut in mortgage rates has restored some confidence but April’s sharp rise in inflation will not help.”

The regions

The North East of England saw the biggest jump in property prices, with double digit increases, on average. The 14.3% rise in the region has taken the average home to a value of £168,227.

In contrast, the slowest rate of growth has been in London, where the annual increase in the year to March stood at 0.7%. The capital is still home to the highest average house prices at £552,073.

Elsewhere, the average price in England increased by 6.7% annually to £295,654. Northern Ireland saw a rise of 9.5% (in the year to the end of the first quarter of 2025), where house prices average £185,037.

Wales posted a 3.6% rise in year to March to £208,093, while Scotland saw a 4.6% average rise to £185,939.

Gareth Lewis, managing director of specialist lender MT Finance, said: “House prices continue to rise because the quality of stock being sold is good but there is plenty of overpriced stock which is sitting on the market for too long and not selling.

“Swap rates had already priced in the recent jump in inflation. But this increase in inflation makes it harder for the property market as, with the stamp duty concession no longer available from April, stimulus at the moment is coming from [mortgage] rate reductions.”

The ONS data also found the rise in monthly private rent eased slightly in the year to April, at 7.4% to £1,335. This annual growth rate was down from 7.7% recorded in the 12 months to March.

However, a survey of tenants by the flatshare website SpareRoom has found that one-in-seven don’t think they’ll ever get onto the property ladder, with a further one-in-three uncertain of when this could happen.

The research shows the rent burden is intensifying, with around a quarter of renters spending more than 50% of their take-home pay on rent and three-quarters spending more than 30%.

19 May 2025: Stamp Duty Changes Take Edge Off Buyer Appetite

- Average prices up 1.2% in year to May

- Typical home worth record high £379,517

- Buyer demand down 4%, sales agreed up 5%

The asking price of the average home coming to market in May has increased by 1.2% year on year, according to the online property portal Rightmove, writes Jo Thornhill.

But while new seller prices rose by 0.6% for the month, taking the average asking price nationally to a record high of £379,517, the monthly increase is the lowest seen in the traditionally busy Spring season since 2016, reflecting a more subdued market.

There has also been a dip in new buyer demand, according to Rightmove, which it says is likely due to the reductions to the stamp duty nil rate bands in April. The changes will see many home buyers paying more tax when they buy.

Demand saw a 4% drop in April after a busy March, according to estate agents, although demand over the 12 months to date is still 3% higher than in the previous 12 months. And despite the lull in buyer appetite, the number of sales agreed is 5% higher than a year ago.

The number of new properties coming onto the market is 14% higher than this time last year, and Rightmove says the overall supply is at a 10-year high. But with the supply of homes for sale outstripping demand, sellers will need to be realistic with pricing.

Colleen Babcock at Rightmove said: “It’s another new price record this month, but having seen a May price record for the last five years, it appears to be driven more by seasonal factors given that new buyer demand has slowed. The 10-year-high choice of homes for sale means sellers need to be aware of the competition they’re facing for the attention of buyers, and the prices that are being advertised in their location.

“Buyers may have several similar homes to choose from in their area, and a home which appears over-priced compared may not get a second look. This month’s price increase being the lowest in May for nine years is a sign of a market that favours buyers and is more subdued than usual.

“Despite April’s dip in demand, there are signs of a bounce-back in May. Mortgage interest rates are lower than they were this time last year, and the recent Bank Rate cut gives us some optimism for further mortgage rate drops.”

Regionally, asking prices have risen most in North of England, Scotland and Wales, while prices have risen by the slowest amount in London, South of England and East of England.

The North West has seen the biggest rise in prices in the year to May at 3.9%, taking the average new asking price to £269,992. In contrast, asking prices are up by 0.6% in the South East region, where the average price stands at £497,475.

Prices rose by 0.4% in London in May, taking the annual rate of increase to 0.7%. Average asking prices in the capital are still the highest of any other region of the country at £701,990.

David Johnson at property consultancy INHOUS said: “Demand picked up immediately after the bank holiday and has remained strong throughout May. This level of buyer motivation is resulting in the majority of sellers receiving multiple offers and achieving their asking price. One and two bedroom apartments are particularly sought-after as well as larger family homes in and around commuter hotspots.”

Tomer Aboody at MT Finance said: ‘With higher supply of stock for sale, buyers have been more spoilt in choice, which is reflected in the lower growth in asking prices. As interest rates reduce, we should see affordability increase which in turn will encourage buyers to be active. This should produce a more buoyant market with higher transaction levels.”

8 May 2025: Interest Rate Cut Likely To Increase Demand

House prices rose 0.3% in April, taking the annual inflation figure to 3.2%, according to mortgage lender Halifax, writes Jo Thornhill.

While the monthly rise recorded was relatively modest, it reversed the fall of 0.5% in average prices seen in March.

The April increase takes the average UK home value to £297,781.

If, as expected, the Bank of England cuts interest rates today (8 May), lower mortgage rates are likely to fuel housing market activity and price rises.

Amanda Bryden, head of mortgages at Halifax, said house prices have been remarkably stable over the last six months, particularly given global economic and political uncertainty: “The market continues to show resilience despite a subdued economic environment and risks from geopolitical developments.

“Stamp duty changes [reductions to the nil rate band from 1 April] prompted a surge in transactions in the early part of this year, as buyers rushed to beat the tax-rise deadline. However, this didn’t lead to a significant increase in property prices, with the last six months characterised by a stability in prices rarely seen since the pandemic.

“While the market has cooled slightly since this rush, buyer activity remains strong in comparison to recent years.”

Regionally the north-south divide continues. Northern Ireland, Wales and Scotland recorded the strongest annual growth across the UK, with all three nations outpacing regions in England.

Northern Ireland saw the highest level of annual property price inflation, rising by 8.1% in March, taking the average home to a value of £208,220.

Wales posted the next highest rate of annual house price growth, increasing by 4.7% in the year to April. The average house price now stands at £229,079.

Average prices in Scotland have risen by 4.6% year-on-year and a typical home in the nation is now valued at £214,011.

The strongest annual price growth across English regions was recorded in the North West at 4.1% in the year to April. The average home in the region is now £240,975.

Southern regions of England lag behind, with the South West recording the lowest level of average house price inflation at 0.9% annually. The average home here is now £304,451.

Halifax says London continues to see more subdued annual house price growth at 1.3% in the year to April. But the capital remains the most expensive market with an average price tag of £543,346.

Mark Harris at broker SPF Private Clients said: “As lenders cut mortgage rates and ease affordability criteria, borrowers are being given more options. With an increasing number of mortgages pegged at the psychologically important sub-4% level, there is less of a barrier for those who need to borrow to buy a home.

“Swap rates, which underpin the pricing of fixed-rate mortgages, continue to decline. A quarter-point rate cut from the Bank of England is expected today, which would further ease affordability, boost confidence and give buyers renewed confidence to make their move.”

Matt Thompson at estate agent Chestertons said: “In April, some house-hunters paused their search amid the Easter holidays, but sellers remained motivated, which resulted in an uplift in the number of properties put up for sale.

“A cut to interest rates would also have an [immediate] impact on buyer activity as more house hunters will feel motivated to start or finalise their search, which will fuel a busier-than-usual summer market.”

30 April 2025: Values Rise 3.4% Annually But See Monthly Fall

- House prices rise 3.4% year on year

- Price growth fell by 0.6% in April

- Average home worth £270,752

House prices fell by 0.6% in April, taking the annual house price inflation figure to 3.4% (down from 3.9% in March), according to the latest figures from Nationwide building society’s house price index, writes Jo Thornhill.

Robert Gardner, Nationwide’s chief economist, said the softening in price increases was widely expected given the changes to stamp duty that came into force on 1 April. The reduction to the nil rate band of stamp duty for homebuyers means many, including first-time buyers, will pay more in tax when they buy a property.

Gardner said: “Early indications suggest there was a significant jump in transactions in March, with buyers bringing forward their purchases to avoid additional tax obligations.

“The market is likely to remain a little soft in the coming months, following the pattern typically observed following the end of stamp duty holidays. Nevertheless, activity is likely to pick up steadily as summer progresses, despite wider economic uncertainties in the global economy, since underlying conditions for potential home buyers in the UK remain supportive.

“Unemployment remains low, earnings are rising at a healthy pace in real terms (after accounting for inflation), household balance sheets are strong and borrowing costs are likely to moderate a little if Bank Rate is lowered further in the coming quarters as we and most other analysts expect. Indeed, swap rates, which underpin fixed rate mortgage pricing, have moderated in recent weeks.”

Residential property sales increased by 62%, up to 177,370 in March from 109,700 in February, according to HMRC transaction data published today (30 April). The rise, the third highest month-on-month increase since records began, was linked to the changes to the nil rate bands for stamp duty.

Jason Tebb, president at property website OnTheMarket, said: “Affordability remains an ongoing concern with rates still higher than many borrowers have grown used to, combined with the high cost of living and other pressures.

“Lenders have been trimming mortgage rates in recent days and further action from the Bank of England [the next interest rate decision is on 8 May] should enable this trend to continue, giving buyers who rely on mortgages increased confidence to make their move.

“With more property stock on the market as one would expect at this time of year, average house prices are being held in check, although local markets and even individual properties can vary considerably.

“Buyers on the whole remain sensitive on price and keen to negotiate because of affordability pressures, so sellers should seek advice from local agents and price accordingly.”

What will happen to mortgage rates and house prices in 2025?

House prices cool as demand slows, says Zoopla

According to property portal Zoopla, average house prices rose 1.6% in the year to March. This compares to the 0.2% annual inflation recorded in March 2024 but is down from 1.9% in December 2024.

Zoopla says buyer demand is up 1% year on year, tempered in the first few months of 2025 by the changes to stamp duty.

The stock of homes for sale is 12% higher than a year ago as more sellers enter the market, possibly buoyed by falling mortgage rates, while the number of sales agreed is 6% higher than at the same point in 2024.

Zoopla’s property experts believe the loosening of mortgage lenders’ stress tests for affordability, prompted by calls from the regulator the FCA to relax stress tests, could boost buying power by up to 20%, which would further support sales.

Richard Donnell at Zoopla said: “Buyer demand has cooled in recent weeks as the supply of homes for sale continues to expand, slowing house price inflation. We expect continued growth in sales agreed, and slow but steady house price inflation.”

16 April 2025: Average Home Now Worth £268,000

The average property price was unchanged in February, according to the latest data released by the Office for National Statistics, but year-on-year values are up by 5.4%, writes Jo Thornhill.

The ONS data is based on completed transactions rather than, for example, asking prices, and is thus one of the most accurate reflections of house prices. The index shows that the average home in the UK is now worth £268,000 (February 2025), £13,000 higher than a year ago.

Transaction figures were also up in February. The number of sales was 28% higher than in February 2024, and 13% higher than in January 2025. This likely reflects buyers’ desire to complete their purchase in the run-up to changes to the stamp duty regime that would have seen them paying more tax from 1 April.

The ONS house price data comes as inflation figures out today show the rate of price increases across the economy fell slightly in the year to March to 2.6% from 2.8% in February.

The drop could encourage the Bank of England to reduce interest rates at the next meeting of its Monetary Policy Committee on 8 May, which would be a further boost to the property market in the wake of the Stamp Duty changes.

According to the ONS, average prices rose in the 12 months to February across the UK. They increased by 5.3% in England to reach an average of £291,640, by 4.1% annually in Wales to reach £207,382, and by 5.7% in Scotland, where average prices are now at £185,870.

In Northern Ireland, the average home increased in value by 9% in the year to the end of the fourth quarter of 2024, the latest data available. A typical property here is now worth £183,259.

Within English regions, the north-south divide remains, with the North West seeing annual price growth of 8% (the average property is now £211,977), for example, while in London prices have gone up by just 1.7% in the same time (average homes in the capital are now worth £555,625).

Semi-detached and terraced homes have seen the largest annual increase in average prices at 6.1% and 6.2% respectively. A typical terraced home is now worth £225,486, while a semi-detached home is worth £270,925, on average.

Flats have risen by the smallest amount year on year at 3%, taking the value of a typical flat to £196,110.

Mark Harris, chief executive at mortgage broker SPF Private Clients, said: “The dip in inflation to 2.6% is encouraging news as far as future interest rate movements are concerned, and if this downward trend continues, it will make it easier for the Bank of England to cut rates again sooner rather than later.

“Another rate reduction would help boost affordability and would be particularly timely now that the stamp duty concession has ended.

“On the mortgage front, several lenders have cut fixed rates, although the best deals aren’t hanging around for long.”

Karen Noye, mortgage expert at advisor Quilter, said: “February’s house price figures show the market holding steady on a monthly basis, but still growing firmly on the year. This suggests a housing market that continues to defy expectations.

“But while house prices have picked up in recent months, the outlook remains mixed. Regional differences are stark and affordability pressures haven’t gone away. But if mortgage rates continue to ease and confidence builds, this spring could mark a turning point for both buyers and sellers.”

Source: ONS (April 2025)

14 April 2025: Buyer Demand Up 5% In Resilient Market

The average asking price of homes coming to market reached a record high of £377,182 in April, according to data from property portal Rightmove, writes Jo Thornhill.

This suggests increased demand across the market despite the stamp duty changes that came into force on 1 April, bumping up property tax bills for many buyers.

The latest monthly increase to average prices was recorded at 1.4% while annual house price inflation is running at 1.3%.

The monthly rise in average prices is bigger than the increases typically seen at this time of year, according to Rightmove, even with a decade-high number of homes for sale. Higher values have been fuelled by an increase in buyer demand, up 5% compared to April 2024. The number of sellers coming to market is up 4% annually.

The increase in choice of homes for sale and increased buyer demand points to resilience in the housing market, according to Colleen Babcock, property expert at Rightmove: “Confidence from new sellers is a good sign for the overall health of the market, but they do need to be careful when setting their asking price.

“The high level of supply right now means buyers are likely to have plenty of homes in their area to choose from, and an overpriced home will stick out for the wrong reasons.

“It’s important to remember that among records and national trends, the [country’s] housing market is made up of thousands of diverse local markets, each uniquely responding to market changes and world events. London, for example, is likely to see greater knock-on effects from the United States trade tariffs than the rest of the country, while Northern regions appear to be performing more strongly post-stamp duty rise.

“It’s difficult to predict what the next few months will bring, but if mortgage rates reduce more quickly, it would be a helpful boost to buyer affordability.”

There is a growing belief that the Bank of England will cut its benchmark Bank Rate from its current 4.5% to 4.25% on 8 May, its next scheduled decision, with up to three further cuts expected during the year. This would trigger reduced mortgage rates and stimulate demand.

Interest rates are likely to fall if the Bank feels the economy is facing recessionary threats as a result of an international trade war triggered by the imposition of import tariffs by the US and retaliatory action, primarily by China.

Rightmove says that, regionally, Scotland and northern regions of England have seen the biggest annual increase in asking prices. The average price in Scotland rose 2.6% year on year to £200,593, while in the North West of England prices are up 2.6% to an average of £266,408. In the North East prices are up 2.2% annually to an average of £194,213.

Annual growth has been slowest in London and the South West of England at 0.4% and 0.2% respectively in the year to April. The average asking price of a home in the South West now stands at £394,342, while London has the highest asking price of any region at £699,200.

Nathan Emerson at estate agent trade body Propertymark said: “It is encouraging to witness the market continue to deliver growth, despite the increasingly complex economic challenges we face. Although the rush from many people in England and Northern Ireland to beat Stamp Duty threshold changes has concluded, we now progress into the spring and summer months, which typically deliver strong momentum.

“We remain in a position where inflation is on a potential uneven footing, and this may impact any decision the Bank of England might make regarding interest rates when they next meet on 8 May.”

7 April 2025: Global economic uncertainty causing ‘buyer worries’

- Average prices down 0.5% in March

- Prices up 2.8% year on year

- March sees record day of sales

- Typical property now £296,699

Property prices took a hit in March, falling by 0.5% (£1,575 in real terms) on top of a 0.2% drop in February, according to Halifax, the UK’s biggest mortgage lender.

The fall in prices is being linked to reduced buyer demand in the run-up to reductions to stamp duty nil rate bands that came into force on 1 April.

The changes to stamp duty saw fewer house-hunters looking to buy in the past two months, fearing their sale would not complete before 1 April and they would pay more in tax.

But Halifax says many buyers did beat the deadline, with more sales completed in March than in January and February combined. It also recorded its busiest ever day of transactions during the month.

Year-on-year house prices were up by 2.8% in March, taking the value of the average home to £269,699, according to Halifax.

What will happen to mortgage rates and house prices in 2025?

Amanda Bryden, head of mortgages at Halifax, said: “House prices rose in January as buyers rushed to beat the end of March stamp duty deadline. However, with those deals now completing, demand is returning to normal and new applications slowing.

“Following this burst of activity, house prices, which remain near record highs, unsurprisingly fell back last month. Looking ahead, potential buyers still face challenges from the new normal of higher borrowing costs, a limited supply of available properties to choose from, and an uncertain economic outlook.

“However, with further base rate cuts expected alongside positive wage growth, mortgage affordability should continue to improve gradually, and therefore we still expect a modest rise in house prices this year.”

What’s happening with house prices?

Regional divide in house price inflation

Northern Ireland has seen the biggest annual rise in average horse prices, according to Halifax’s data. Prices here are up 6.6% year on year in March, with a typical home now worth £206,620.

Prices in Scotland, Wales and the northern regions of England have also seen relatively high growth in the year to March. Prices are up 4.3% in Scotland to an average of £213,750. In Wales average prices are up 3.7% to £227,322, while in Yorkshire and Humber they are up 4.2% to £215,807.

In contrast, prices have risen the least in the East of England, southern regions of England and Greater London. Prices are up a nominal 1% in the South West, for example, where the average home is now worth £304,091. In Greater London prices have risen 1.1% to an average of £543,370.

Jeremy Leaf, a north London estate agent, said: “There’s no doubt many purchases were brought forward as a result of the stamp duty deadline, so we might have expected to see more impact in the data.

“Buyers and sellers who missed out on the stamp duty savings had the choice to stay put, keep to previously-agreed terms and continue with their move or try to re-negotiate in an attempt to find some middle ground. The last option has proved the most popular in our offices.

“However, worries about short and longer-term economic prospects both here and abroad have been driving that decision-making (or lack of it) over the past few weeks at least.”

Karen Noye, mortgage expert at financial advisor Quilter, said: “The housing market’s resilience is wavering with a second monthly decline in prices. Borrowing still remains expensive by historic standards. The traditional spring bounce appears to be more muted than usual.

“Adding to this, the news of tariffs might start to spook would-be buyers as once again unpredictability seeps into the market. But swap rates which dictate fixed-rate mortgage deals have tumbled as traders speculate that there could now be further rate cuts to fuel economic growth in the face of the impact of the tariffs.

“Affordability therefore could improve at least in the near term.”

1 April 2025: Northern Ireland Posts Double-Digit Annual Growth

- Prices up 3.9% year on year

- Monthly change flat

- N Ireland sees 13.5% annual growth

House prices remained stable in March, rising 3.9% annually on average, according to data from Nationwide building society, writes Jo Thornhill.

It was the same annual rise as recorded in February, following no change in month-on-month for average prices in March. The average home across the UK is now worth £271,316, according to the lender’s figures.

Regionally, Northern Ireland has seen the largest annual increase in average prices at 13.5%, pushing the average price locally to £205,796.

London was the worst-performing area for price rises, with an annual increase of 1.9%. The capital still has the most expensive homes, on average, at £529,369.

Overall there continues to be a north-south divide in the performance of house prices, with the top six areas in the north of the UK, while the lowest-performing six are in the south of England.

Robert Gardner, Nationwide’s chief economist, said: “These price trends are unsurprising, given the end of the stamp duty holiday at the end of March (transactions associated with mortgage approvals made in March, especially toward the end of the month, would be unlikely to complete before the deadline).

“The market is likely to remain a little soft in the coming months since activity will have been brought forward to avoid the additional tax obligations – a pattern typically observed in the wake of the end of stamp duty holidays.

“Nevertheless, activity is likely to pick up steadily as the summer progresses, despite wider economic uncertainties in the global economy, since underlying conditions for potential home buyers remain supportive. The unemployment rate is low, earnings are rising at a healthy pace in real terms (after accounting for inflation), household balance sheets are strong and borrowing costs are likely to moderate a little if Bank Rate is lowered further in the coming quarters as we and most other analysts expect.”

Nathan Emerson, chief executive at estate agent trade body Propertymark, said: “The housing market has witnessed an extremely encouraging start to the year with sustained house price growth year on year. Although we now sit at the very start of the amended stamp duty thresholds for England and Northern Ireland, we remain optimistic to see strong market momentum across the entire UK, as we head towards the traditionally busy summer months.

“Although we are still seeing fluctuations within the rate of inflation, and a much needed cautious approach from the Bank of England regarding base rates, we are starting to see enormously welcome sub-4% mortgage deals offered by some lenders.”

The Bank of England’s latest Money and Credit report shows gross mortgage lending, which topped £24.3 billion in February, is at its highest level since November 2022, when it reached £24.9 billion.

However, the number of mortgage approvals dropped by 600 to 65,500 in February. This is a measure of borrowers remortgaging to a new lender – it does not record new mortgages with an existing lender (known as a product transfer). It followed a fall of 400 in January.

Remortgage approvals were also down by 800 to 32,000 in the period, following an increase of 2,100 in January.

Mark Harris, chief executive at mortgage broker SPF Private Clients, said: “With mortgage approvals falling only slightly in February, it’s steady-as-she-goes for the market.

“Remortgaging numbers dipped, perhaps suggesting that borrowers are sticking with their existing mortgage provider rather than shopping around and going through the hassle of applying to another lender.”

26 March 2025: Zoopla Sees Return Of Buyers’ Market

- Prices rise 4.9% in year to January

- Month-on-month rise at 0.2%

- Typical home priced £269,000

House prices rose, on average, by 4.9% in the year to January, according to government data from the Office for National Statistics, writes Jo Thornhill.

Zoopla, the online property portal, has reported house price inflation cooling in February, with an annual price increase of 1.8% compared to a rise of 1.9% in January (more on Zoopla’s latest data below).

The annual price rise recorded by the ONS, which uses official property transaction data from the Land Registry to compile its index, takes the average home in the UK to a value of £269,000 – £13,000 higher, in real terms, than a year ago.

The monthly figures show prices rose, on average, by 0.2% between December 2024 and January 2025, compared with a fall of 0.1% in the same period 12 months ago.

It comes as the ONS’s report into housing affordability, published earlier this week, shows affordability has returned to pre-Covid levels, after the situation worsened in 2020-21. The average home (at £269,000) is 7.7 times the median average salary of £37,600 a year.

During the pandemic in 2021, the average home value was more than nine times average earnings.

ONS regional data reveals Northern Ireland has seen the biggest price increase, recording a rise of 9% in average values in the year to the end of the fourth quarter of 2024. It takes the average property value in the country to £183,259.

Prices have risen by 6% in the year to January 2025 in Wales, to an average of £209,579, while prices are up by 4.6% over the same period in Scotland, to £187,434.

Among English regions, prices have grown most in the North East, increasing by 9.1% to £161,373 in the 12 months to January 2025. London was the English region with the lowest annual inflation, where average prices are up by 2.3% annually to £563,899.

Terraced and semi-detached homes have increased in value the most over the past 12 months, according to the ONS, rising by 5.9% and 6% respectively. A typically semi-detached home in the UK is now worth £271,027. In contrast, the value of flats has risen by 2.3% over the same period to an average of £196,069 nationally.

Source: ONS

Commenting on the ONS figures, Jeremy Leaf, a north London estate agent, said: “The modest increase in prices confirms what we have seen in our offices – a steady rise kept in check by improving stock levels.”

Zoopla house price index

Zoopla says the housing market is showing signs of resilience, despite the looming stamp duty changes and interest rates not falling as quickly as borrowers had hoped.

Its data shows there are 11% more homes for sale (for the four weeks to 16 March) compared to the same period last year, and 5% more sales agreed. But it says the supply of homes is currently outstripping demand, particularly in London and the south of England, which is acting to suppress prices (house price inflation is running at just 1.8% year on year).

Richard Donnell at Zoopla said: “Buyers have a wide choice of homes for sale which will keep price inflation in check. Sellers need to be very careful in how they price their homes if they are serious about moving in 2025.”

Among UK cities prices have risen the most over the past year include Belfast (up 5.7%) to an average of £183,900 and Liverpool (up 3%), where the average home is now worth £162,000, according to Zoopla.

Eight out of the nine cities which have seen the lowest annual price growth are in the Midlands or south of England, including Bristol, London, Oxford, Bournemouth and Southampton.

17 March 2025: Stamp Duty Deadline Pushing More To Market

- Asking prices up 1.1% in March

- Agreed sales up 9% year-on-year

- Average asking price £371,800

The property market is seeing a robust start to the year, according to the latest data from Rightmove, with average asking prices rising 1.1% in March and prices up 1% compared to 2024, writes Jo Thornhill.

Compared to the same period last year, 9% more sales were agreed. In addition, the number of properties being listed for sale is at its highest level since 2015, which is good news for buyers as increased supply should subdue price rises.

Experts say the surge in activity is likely due to buyers and sellers trying to beat stamp duty tax changes on 1 April, which will affect the market in England and Northern Ireland. The nil rate band thresholds for first-time and other buyers are set to fall, leading to bigger tax bills for most.

The average home coming to market is now valued at £371,870 by Rightmove, which is £3,876 more than in February and in line with the long-term average increase in prices seen in March.

Colleen Babcock, property expert at Rightmove, said: “Historic averages show that March is likely to be one of the strongest months of the year for sellers to spring into action. However, sellers can’t just rely on these historic averages for success, as this year they are facing a decade-high level of competition.

“The big milestone ahead is the stamp duty deadline, and with a massive log-jam of 575,000 moves going through the legal completion process, many cost-conscious buyers will be doing all they can to get their move over the line and avoid unnecessary extra tax.”

Mortgage rates are only slightly lower now than at this time last year, according to Rightmove data, which means buyer affordability remains stretched. Its figures show the average five-year fixed mortgage rate is 4.74%, down from the peak of 6.11% in July 2023, but only marginally lower than the 4.84% recorded this time last year.

The outlook is for mortgage rates to fall, albeit slowly. The Bank of England cut the benchmark Bank Rate in February from 4.75% to 4.5%. Its next meeting to decide on the Bank Rate level is on Thursday 20 March, when it is expected to keep rates on hold at 4.5% as the annual inflation rate increased in January from 2.5% to 3%.

The Bank uses high interest rates to cool the economy and bring the rate of price increases down.

Mark Harris, chief executive of mortgage broker SPF Private Clients, says: “Swap rates [the interest rates banks use to lend to each other in wholesale markets] largely dictate the pricing of fixed-rate mortgages, and a recent decline in pricing has enabled lenders to launch cheaper mortgage rates this month.

“In theory, even if the Bank of England holds base rate at 4.5% in March, the pricing of fixed-rate mortgages could still decline if swap rates continue on a downward trajectory.”

Regional variations in asking prices

Asking prices rose, on average, in every region in England, Wales and Scotland in March, according to Rightmove. But on an annual basis, price rises show a distinct north-south divide.

While prices are up by 4% in Scotland over the past year (the average asking price is £197,643), up by 2.4% in Yorkshire and The Humber (£252,957) and by 2.6% annually in the North West (£263,855), annual rises are more modest in the south.

Prices are up year on year by 1.2% in the East of England (average asking price £420,120) and 0.6% in the South East (£481,890), and they fell by 0.3% in the South West (£382,637).

In London the year on year increase is 1.3% which takes the average asking price of a property in the capital to £695,885.

Matt Thompson, head of sales at estate agent Chestertons, said: “As we are seeing the beginning of spring this month, agents are preparing for what is historically known as one of the busiest times of the year for the property market.

“2025 was off to a strong start with increased buyer demand and we foresee this level of buyer motivation to intensify by the end of March. The majority of sellers are aware of the heightened market activity which has also led to an uplift in the number of vendors planning to put their property on the market in due course.

“While this will provide house hunters with a slightly larger pool of properties to choose from, we still expect to see several buyers compete over a single property.”

7 March 2025: Demand Wanes As Stamp Duty Hikes Loom

- House prices slip 0.1% in February

- Annual growth steady at 2.9%

- Average UK home worth £298,602

The average UK house price fell by 0.1% in February, wiping just £213 from its total value to leave it at £298,602, writes Laura Howard.

The UK’s largest mortgage lender puts the cost of an average home at £298,602 compared to £298,815 the previous month, which saw a 0.6% monthly rise. Annual growth held fast at 2.9%, unchanged from January.

While mortgage deals have become more competitive in recent weeks, demand is waning as the 1 April deadline for stamp duty concessions comes closer, leaving new buyers insufficient time to complete their property purchase, said Halifax.

Most UK regions saw a slowdown in house price inflation in February. On an annual basis, Scotland saw growth accelerate at the fastest rate in 13 months to 3.8%, up from 2.5% in January. Average house prices in the country now stand at £213,014.

The strongest annual property price growth, however, continues to be in Northern Ireland, which remained unchanged in February at 5.9%. Properties in Northern Ireland now cost an average of £205,784.

In Wales, annual house prices were up by 2.8% in February, with the average property valued at £226,811.

In England, the Yorkshire and Humberside region recorded the strongest annual growth – up 4.1% compared to the previous year, with properties costing an average of £216,130.

The traditionally strongest parts of the English housing market saw the weakest growth. In the South East, annual growth was at 2.2% in February, while in Greater London it stood at 1.6%, down from 2.6% in January.

However the capital still has the most expensive homes, with an average value of £545,183.

Amanda Bryden, head of mortgages at Halifax, said: “While house price growth has slowed overall, market activity remains strong and comparable to pre-pandemic levels, demonstrating a resilience amongst buyers that’s been evident in the face of higher borrowing costs.”

Ms Bryden added that an ongoing shortage of housing supply coupled with sustained demand suggests that property prices will continue to rise this year, albeit at a more measured pace compared to 2024.

Matt Smith at property portal Rightmove said the weeks before the changes to stamp duty thresholds on 1 April are likely to see frenetic activity: “As the deadline edges nearer, we expect a rush to complete from those in the process of buying a home, particularly from affordability-stretched first-time buyers eager to avoid unnecessarily parting with thousands of extra pounds.”

28 February 2025: Prices Up Despite Tougher Affordability

- House prices rise 0.4% in February

- Property values up 3.9% annually

- Average home now worth £270,493

House price inflation remained stable at 0.4% in February, according to Nationwide writes Jo Thornhill. The monthly rise was up from the near-flat 0.1% growth in prices recorded in January 2025.

Year-on-year house prices have risen by an average of 3.9% according to the building society, revealing notable resilience in the market during 2024 despite higher mortgage rates. The average property is now worth £270,493.

Robert Gardner, chief economist at Nationwide, commented: “Housing market activity has remained resilient in recent months, despite ongoing affordability challenges. Indeed, the second half of 2024 saw a noticeable pick-up in total housing transactions, which were up 14% compared with the same period in 2023.

“However, taking 2024 as a whole, transactions were still modestly (6%) lower than the levels prevailing before the pandemic struck in 2019.

“It is notable that first-time buyer activity continued to recover, with mortgage completions in 2024 just 5% below 2019 levels. This represents a solid performance, given the interest rate environment.”

Housing transactions, as recorded by stamp duty receipts received at HMRC, also support signs of a resilient market. The government data shows 95,110 sales were completed in January, which is 14% higher than in January 2024 and just 1% lower than in December 2024.

Matt Thompson, head of sales at estate agent Chestertons, said: “February’s property market saw a decline in first-time buyer enquiries as the chances of finding a property in time to beat the changes to stamp duty are now nil.

“We did, however, see continuous demand from other buyer demographics; especially after the Bank of England announced a rate cut to 4.5% in January. With the news of sub-4% mortgages returning to the market, we expect more house hunters to start their search over the coming weeks.”

Stamp duty thresholds will change from 1 April 2025 for home buyers in England and Northern Ireland. For first-time buyers the nil-rate band threshold for stamp duty will fall from £425,000 to £300,000. It will also only apply to homes worth up to £500,000, rather than the current £625,000.

The standard nil-rate band for stamp duty for all other residential buyers is set to drop from £250,000 to £125,000.

7 January 2025: Northern Ireland Records Strongest Growth

- House prices increase 3.3% annually

- Values drop 0.2% in December

- Average home worth £297,166

Average property values increased by 3.3% in 2024 but finished the year with a marginal 0.2% fall in December, according to the latest data from Halifax, writes Jo Thornhill.

The UK’s biggest mortgage lender says the average home now costs £297,166.

Across the UK, Northern Ireland saw the strongest price growth last year, with typical values rising 7.4% to push the average to £205,895.

In Wales, average prices rose by 4.6% to £226,646, while in Scotland prices edged up more slowly, by 2.4%, to an average of £209,959.

Among the English regions, prices in the North West saw the biggest annual rise, at 5.3%. A typical home in the North West now costs £238,832.

London, which has the highest average house prices in the UK at £547,614, saw average values rise by 3.3% in 2024.

Amanda Bryden, head of mortgages at Halifax, said: “While the housing market has been supported in recent months by falling mortgage rates, income growth and the announcement on upcoming stamp duty policy changes, mortgage affordability will remain a challenge for many, especially as the [Bank of England] Bank Rate is likely to come down more slowly than previously predicted.

“However, providing employment conditions don’t deteriorate markedly from a more recent softening, buyer demand should hold up relatively well and, taking all this into account, we’re continuing to anticipate modest house price growth this year.”

Mark Harris, chief executive of mortgage broker SPF Private Clients, said: “Modest house price growth is being underpinned by borrowing costs which, while softening, remain higher than many borrowers were paying just a few years ago.

“With HSBC, Halifax and Leeds Building Society among those lenders reducing some of their mortgage rates this month, the new year has got off to an encouraging start. Borrowers will be hoping that other lenders follow suit and that the Bank of England delivers further rate reductions, helping ease affordability concerns.”

Karen Noye, mortgage expert at Quilter, said: “Despite the challenges it faced throughout 2024, the housing market ended the year looking considerably stronger than many might have anticipated 12 months ago.