Featured partners

Compare the Best Stocks to Buy

The Best Stocks to Buy Now

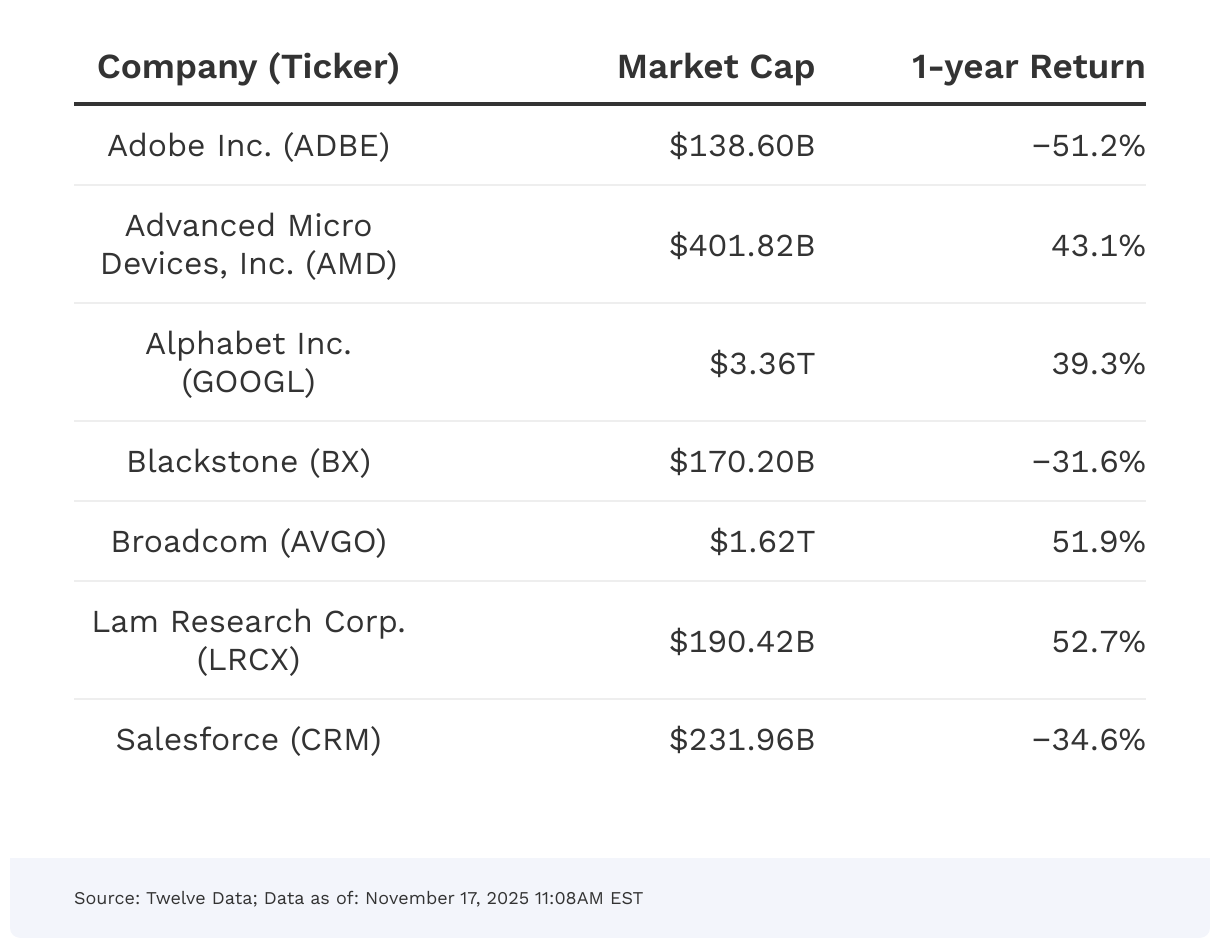

Adobe, Inc (ADBE)

Best for buy-and-hold investors

Adobe, Inc (ADBE)

Forward P/E

P/E

1-year return

Editor’s Take

Have you heard of Photoshop, Audition or Premiere Pro? If so, then you’re familiar with Adobe software. With digital content creation as widespread as it is, companies like Adobe are benefiting.

Why We Like It

If you’re considering ADBE stock as a “set it and forget” investment, its financial stability and continued innovation may reassure you. Revenue in the August 2025 quarter clocked in at $5.99 billion, up 2% from the prior quarter. So steady growth.

What We Don’t Like

In the world of digital creation, ADBE is facing competition from cheaper alternatives and open-source tools. The stock is also exposed to economic sensitivity, as its customers, many of whom are small businesses and freelancers, are vulnerable to economic downturns.

Pros & Cons

- Solid financial performance

- Strong economic moat

- High demand for digital content creation

- Trades at a high price-to-earnings ratio, implying the stock might be trading at a high valuation

- Faces competition from cheaper alternatives

- Overreliance on small businesses and freelancers

Advanced Micro Devices, Inc. (AMD)

Best for semiconductor enthusiasts

Advanced Micro Devices, Inc. (AMD)

Forward P/E

P/E

1-year return

Editor’s Take

AMD is one of the darlings of the semiconductor industry.

Why We Like It

The stock has been ablaze with excitement surrounding artificial intelligence stocks. Intel is one of AMD’s primary competitors. But the Santa Clara, California-based company has managed to dig in its heels and gain market share in the CPU, GPU and data processing space. The firm continues to grow in key markets, mainly high-performance computing, gaming and AI. Revenue growth has been solid. AMD’s third-quarter revenue from the 2025 fiscal year was up more than 36% year over year.

What We Don’t Like

Regarding competition pressure, Nvidia still reigns supreme in the AI GPU space—limiting AMD in that lucrative market. The company also relies on the Taiwan Semiconductor Manufacturing Co. (TSMC) for its chip production.

Pros & Cons

- Consistent gains in market share in the CPU space

- Financial momentum

- Growth in key AI markets

- A high P/E that sparks valuation concerns

- Exposure to geopolitical risks because of its international supply chain

- Nvidia’s dominance in the GPU space

Alphabet (GOOG, GOOGL)

Best for Growth

Alphabet (GOOG, GOOGL)

Forward P/E

P/E

1-year return

Editor’s Take

It’s sometimes easy to forget that a big name like Google is merely one of several businesses that make up Alphabet. In 2015, Google co-founders Larry Page and Sergey Brin restructured the Google search business as one of several subcompanies under the new parent company.

Why We Like It

Today, Alphabet is one of the world’s most valuable companies, with Google dominating nearly 90% of the worldwide market share for internet search. While advertising is the company’s primary revenue, Alphabet generates income from Google Cloud, hardware devices like Nest and Pixel, and other ventures like Waymo, an autonomous driving technology company.

Regarding performance, Alphabet delivers consistent revenue growth and high profit margins with minimal debt. EPS growth for fiscal 2026 is expected to clock in at just over 11%.

What We Don’t Like

When it comes to cons, the company faces intense regulatory scrutiny over antitrust issues as well as controversies surrounding data privacy. GOOG stock also trades at a premium when compared with other tech stocks.

Pros & Cons

- Market dominance in online search

- Leader in digital advertising

- Consistent revenue growth

- High valuation

- Faces regulatory scrutiny over antitrust issues

- Competition from AI-focused companies, like Meta (META) and Amazon.com (AMZN)

Blackstone (BX)

Best for alternative asset exposure

Blackstone (BX)

Forward P/E

P/E

1-year return

Editor’s Take

Blackstone is a behemoth in global investment, handling assets like private equity, real estate and credit. The New York-headquartered company has made numerous acquisitions, including the likes of hotel chains such as Hilton in February 2007. It’s also one of the world’s largest alternative asset managers, with more than $1 trillion in assets under management (AUM).

Why We Like It

BX is on an upward trajectory. For the first three quarters of fiscal 2025, BX beat market expectations. The icing on the cake was BX’s third-quarter earnings with a 24% surprise EPS beat. Analysts expect revenue to march on and grow by 26% in fiscal 2026.

What We Don’t Like

While BX is diversified in what it does, its ability to do real estate deals is a risk because large commercial deals typically rely on debt financing. That said, the Federal Reserve’s future series of rate cuts could serve as a catalyst in its real estate business for years to come.

Pros & Cons

- Great stock for gaining exposure to alternative assets

- Pays a nice dividend of at least 3%

- Consecutive quarters beating earnings expectations

- High interest rate environment can slow down real estate deals

- Private equity is facing growing regulatory scrutiny

- Premium stock valuation compared to other financial stocks

Best for AI workloads

Broadcom (AVGO)

Forward P/E

P/E

1-year return

Editor’s Take

AVGO is a “picks and shovels” stock. In other words, you can be exposed to other Big Tech names like Alphabet or OpenAI. Those “big shot” companies partner with Broadcom.

Why We Like It

AVGO holds the majority of the market share for application-specific integrated circuits (ASICs). Broadcom has also been very strategic in acquisitions; AVGO acquired VMware in 2023 for $69 billion, a move that expanded Broadcom’s reach into cloud computing and virtualization.

Sales will continue a hot streak, expected to grow nearly 35% in the 2026 fiscal year. For AVGO’s 2025 fiscal year, the company has been able to beat earnings per share (EPS) expectations in the first three quarters.

What We Don’t Like

Broadcom is very exposed to the smartphone market. In the past, Apple has represented 20% of AVGO’s net revenue. And now Apple is creating its own Bluetooth and Wi-Fi chips. This will likely impact Broadcom as a supplier, although AVGO does still maintain some licensing deals with the company that Steve Jobs built.

Pros & Cons

- Strategic acquisitions to diversify the business

- A big player in ASICs

- Overreliance on Apple

- High stock valuation

Lam Research Corp. (LRCX)

Best for Dividends

Lam Research Corp. (LRCX)

Forward P/E

P/E

1-year return

Editor’s Take

Lam Research produces and supplies semiconductor processing equipment for cell phones, computers, wearables and other devices.

Why We Like It

Lam Research is a classic pick-and-shovel play if you’re trying to get exposure to the semiconductor industry. In stock speak, that means it’s a company that provides necessary equipment for an industry’s end product. And you’ve probably heard of Lam’s biggest clients: TSMC, Samsung and Intel, all big chipmakers.

LRCX’s financials are solid. Revenue for the 2025 fiscal year was up by 24%.

What We Don’t Like

One of the biggest obstacles facing LRCX is that its revenue comes from a concentration of a few clients, and there are also geopolitical risks, too. With many Asian customers, LRCX would face difficulties if it faced U.S. restrictions on selling semiconductor equipment to China.

Pros & Cons

- Growing demand for AI and high-performance computing.

- Robust revenue and profit margins.

- Pays a dividend.

- Exposure to geopolitical risks associated with China.

- Faces competition from Applied Materials and ASML.

- Revenue is concentrated among a few chipmaker clients.

Salesforce (CRM)

Best for AI business solutions

Salesforce (CRM)

Forward P/E

P/E

1-year return

Editor’s Take

Well-known companies like FedEx, PepsiCo, Pandora and even schools like the University of Chicago use Salesforce for their business solutions in sales and marketing. Some of those software-as-a-service solutions range from providing student support with “purpose-built AI for education,” automated workflows for big companies, digital marketing solutions for building customer bases, and more.

Why We Like It

Salesforce is such a big name in customer relationship management (CRM) sales software, so much so that its ticker on the New York Stock Exchange (NYSE) is that exact acronym. And you’ve probably even seen the hallmarks of CRM in your inbox in the form of automated sales emails.

CRM sales growth is expected to increase by nearly 9% for the 2026 fiscal year. For the first two quarters of the fiscal year 2026, CRM has beaten its EPS expectations.

What We Don’t Like

Salesforce’s growth is beginning to flag a bit as it navigates pressure on its profit margins.

Pros & Cons

- Well-known trusted platform

- Data to train AI models

- Trades at a premium with a sky-high price-to-earnings ratio

- Revenue growth slowdown

Methodology: How we score our products

The top stocks listed above all meet the following criteria and are traded on major U.S. stock exchanges:

- Analyst Consensus of “Buy” or Better: A high number of “buy” ratings from analysts suggest the stock is expected to outperform the broader market.

- Market Capitalization of $10 Billion or More: Companies with a market cap of over $10 billion typically dominate their industries and possess competitive advantages. Smaller companies, with market caps under $10 billion, tend to receive less attention from the media and analysts and carry higher investment risks.

- Altimeter Overall Grade of B or Higher: Only stocks rated “B” or above by Altimeter are included. This grade reflects factors like profitability, earnings stability, valuation, and growth expectations. Stocks that score B or better rank in the top quarter of over 5,000 companies in Altimeter’s database, signaling strong potential for improving returns and favorable valuations.

- Positive Earnings-Per-Share Growth: For our analysis, we looked at stocks that had delivered positive EPS growth over the past five years, which is an indicator of strong financial and profitability performance. We also screened for stocks that had positive projected EPS growth for 2025.

Top Performing Stocks This Year

While the highest returns might look flashy, it’s important to remember that a stock’s performance is backward-looking and not an indicator of future returns. That’s why we curated a shortlist of stocks above based on methodologies to screen for risks and future projections.

But it’s only natural to be curious about the heavy hitters that are performing well this year. That’s why listed below are the top performing stocks in the S&P 500 based on year-to-date returns.

What to Look for When Buying Stocks

When shopping for stocks, it’s important to do your due diligence with research and understand key metrics in the decision-making process.

You can easily find a company’s financial statements on Yahoo Finance and Google Finance. From there, you can examine metrics and data within those reports, such as revenue, profit margins and earnings.

Metrics help investors gain insight into a company’s overall financial health. You’ll also want to consider the company’s future growth since that will affect stock appreciation and earnings. Look through reports, stay current on the news and follow expert analysis. Many stock analysts also examine the company’s overall management team and leadership. That way, they can understand how strategic decisions are made.

If you’re new to investing, you’ll want to look for companies with a competitive edge, with the potential for growth and stability. Valuation is also important, where metrics like a stock’s price-to-earnings or price-to-book ratios come into play. When compared to a company’s industry peers, these metrics can help you gauge whether a stock is overvalued or undervalued.

To sum up, before making a stock purchase, apply research and learn how to invest in stocks.

Frequently Asked Questions (FAQs)

How long should I hold these stocks?

How long you should hold stocks depends on your objectives and what the market is doing. In general, most investors build wealth by holding stocks long-term. Our picks for the best stocks to buy now include a lot of technology and semiconductor stocks. These industries have done extremely well over the past several years and are likely to do so for the next few years at least. But will they still do well in 20 years, or will some of these companies be replaced by the next innovation? You’ll have to keep up with industry trends to know when the best time to sell is and you probably won’t get the timing perfectly right. That’s part of the risk of investing in individual stocks.

How much should I invest in stocks?

There’s no one-size-fits-all answer. If you’re younger, you have a longer time horizon and can allocate more of your investment portfolio. In other words, you have some wiggle room to be riskier, allocating up to 70% to 90% of your portfolio to stocks.

As you approach retirement, you need to be slightly more conservative with your investments. It is typically recommended that you trim your stock portfolio allocation to 60% to 70% by the time you are in your 40s or 50s. As you age, you want to turn more to bonds and cash holdings for stability and lower risk tolerance.

If you still need more help, a financial advisor can help you tailor your strategy based on your specific needs and circumstances.

{kind=link}

{kind=link}

{kind=link}

{kind=link}