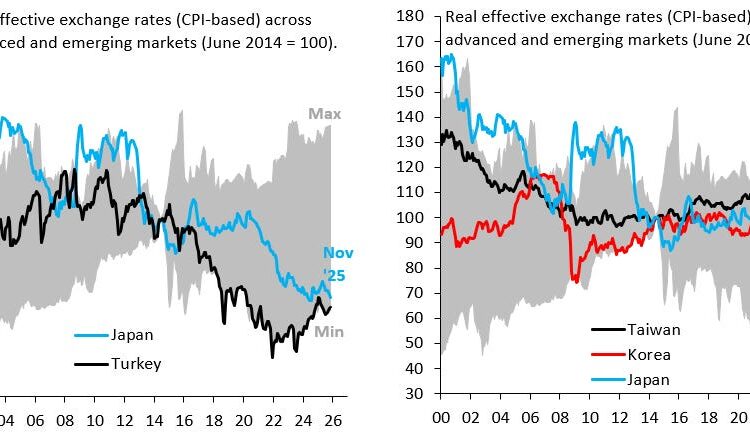

A few months ago, I caused consternation by pointing out that the Japanese Yen in real effective terms is as weak as the Turkish Lira. That’s shocking when you consider what a disaster Turkey is when it comes to erosion of central bank independence and how that’s debased the Lira. There are unfortunately undeniable parallels with Japan. President Erdogan fired the Governor of his central bank in March 2021 because he wanted lower interest rates. What followed were interest rate cuts and a catastrophic depreciation of the Turkish Lira. Nothing nearly as graphic has happened in Japan, but the massive debt load means the Bank of Japan (BoJ) has no choice but to cap long-term yields via ongoing purchases of government bonds. That’s putting depreciation pressure on the Yen. The BoJ is de facto as much a captive as Turkey’s central bank.

The left chart above is what caused so much consternation back in November. It shows the Yen (blue) and Turkish Lira (black) in real effective terms, meaning these are averages across many bilateral exchange rates and adjust for how inflation drives the price level in different countries. As of Nov. ‘25, the Yen had fallen almost to the level of the Turkish Lira.

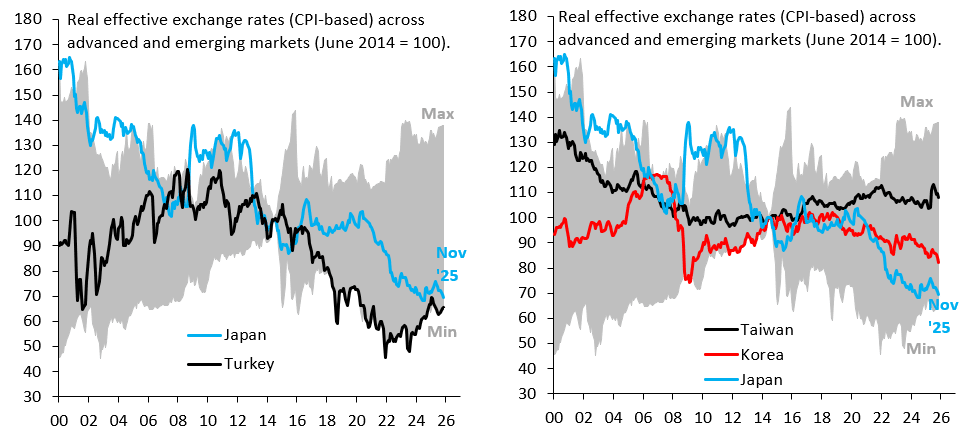

One pushback to this chart is that all Asian currencies are weak, so the fact that the Yen is weak doesn’t mean there’s a crisis. I think that’s wrong for two reasons. First, as the right chart above shows, the Yen (blue) is far weaker than the Korean Won (red) or Taiwanese Dollar (black). Second, and much more importantly, neither Korea nor Taiwan are seeing the kind of spike in bond yields that’s been hounding Japan for the past year. You simply can’t compare what’s going on with the Yen to the rest of Asia. No one else has Japan’s yield spike as the currency falls.

The bottom line is that the Yen is weak in absolute terms, since it’s far below the Korean Won or Taiwanese Dollar. More importantly, it’s shockingly weak when seen against the backdrop of sharply higher yields. As I explained in a recent post, as long as the BoJ suppresses the fiscal risk premium in the bond market, that risk premium will show up in the currency and put depreciation pressure on the Yen. Unfortunately, Japan is much more like Turkey than we would like to admit.

{kind=link}

{kind=link}

{kind=link}

{kind=link}