The Indonesian Rupiah (IDR) recently absorbed a historic shock, breaching the psychological threshold of Rp 18,000 per US dollar for the first time. According to Bloomberg and Bank Indonesia’s JISDOR (Jakarta Interbank Spot Dollar Rate), the currency hit an intraday low of 18,209/USD on June 9, 2026.

However, based on official Bank Indonesia (BI) announcements, aggressive market interventions and back-to-back interest rate hikes which pushed the BI benchmark rate to 5.75% on June 18 have temporarily halted the freefall.

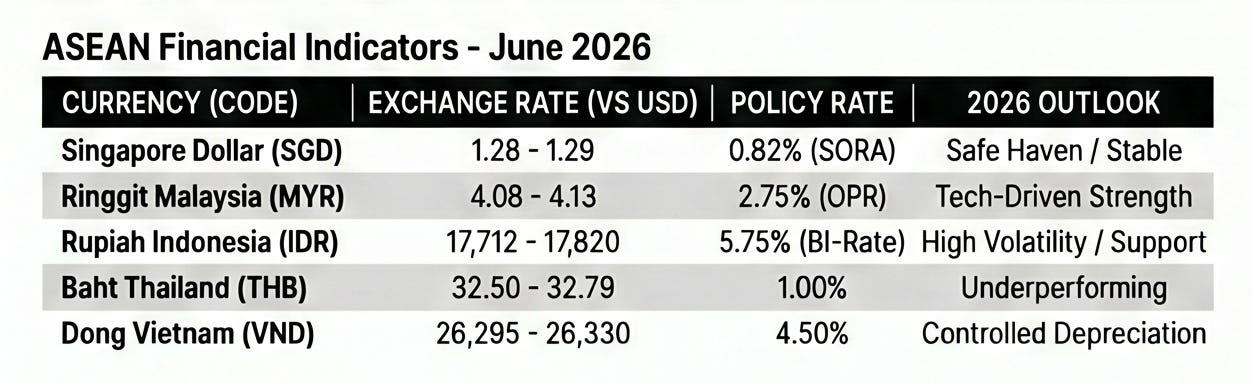

As of late June, the Rupiah is stabilizing in the 17,700–17,800 range, but the crisis exposed deep vulnerabilities driven equally by global volatility and domestic fiscal complacency.

As Southeast Asia’s largest economy, Indonesia acts as a regional bellwether. Based on demographic and economic data from Statistics Indonesia (BPS), a currency crash directly disrupts domestic consumption for 278 million people.

Furthermore, it signals to international investors how vulnerable broader emerging markets are to shifting global capital flows and internal policy risks.

According to structural economic data from the Ministry of Finance and Bank Indonesia, the Rupiah is traditionally highly sensitive to external pressure due to two realities:

-

💸 Foreign Capital Reliance: Based on Ministry of Finance debt composition data, Indonesia relies heavily on foreign portfolio investments to finance its government bond market (SBN). When global sentiment sours, capital flight disproportionately hits the Rupiah.

-

🛢️ Fossil Fuel Dependency: Despite being a major commodity exporter, data from the Ministry of Energy and Mineral Resources confirms Indonesia is a net importer of crude oil and refined fuel. Spikes in global oil prices create massive domestic demand for US dollars to pay for energy imports, which actively drains foreign exchange reserves.

Based on historical economic records from the World Bank, the IMF, and Bank Indonesia, the current plunge is not the first time the Rupiah has faced massive structural pressure. Since independence, it has weathered several historic depreciations:

-

1965 (Hyperinflation): According to Indonesian economic history archives, severe economic mismanagement and political turmoil triggered hyperinflation rates exceeding 600%, culminating in a drastic currency redenomination to stabilize the economy.

-

1997–1998 (Asian Financial Crisis): Based on data from the International Monetary Fund (IMF), regional contagion and massive unhedged foreign corporate debt led to the Rupiah plummeting from roughly 2,400/USD to over 16,800/USD. The resulting economic collapse led directly to the fall of the Suharto regime.

-

2008 & 2013 (Liquidity Shocks): According to Bloomberg global market data, panic capital flight during the 2008 Global Financial Crisis pushed the Rupiah past 12,000/USD. Later, in 2013, the US Federal Reserve’s “Taper Tantrum” permanently pushed the currency past the 14,000/USD threshold.

-

2020 (COVID-19): Based on Bank Indonesia market tracking, global pandemic lockdowns caused a sharp, sudden plunge past 16,500/USD as investors liquidated emerging-market assets.

🔍 The Crucial Distinction: While the 2026 breach of 18,000/USD is a nominal record low, it is fundamentally different from the 1998 crisis. Based on Bank Indonesia’s latest official reports, Indonesia currently holds over $140 billion in foreign exchange reserves, whereas reserves were nearly depleted in 1998. The banking sector is highly capitalized, making this a managed slide rather than an overnight systemic collapse.

Market data indicate investors actively punished the Rupiah for perceived poor fiscal management, demanding an “Indonesia-specific policy risk premium” due to several recent missteps:

-

Bloated Spending vs. Weak Revenues: Based on state budget reviews by the Ministry of Finance, the government pushed an aggressive budget expansion to fund massive new initiatives, such as the “Free Nutritious Meals” program. With actual tax revenue collections weakening compared to the previous year, rating agencies anticipated heavier debt issuance and wider fiscal deficits.

-

Policy Unpredictability: According to market alerts from global index providers, transparency concerns such as the centralization of strategic commodity exports through the new Danantara sovereign wealth fund and MSCI index reviews spooked foreign investors.

-

Loss of Macro Credibility: Based on tracking data for Indonesian Government Securities (SBN), an eroding sense of fiscal discipline led to aggressive sell-offs by foreign institutional investors, who dumped Indonesian bonds and pulled capital out of the country.

These domestic vulnerabilities were compounded by unforgiving global conditions:

-

Geopolitical Energy Crisis: According to global commodities-tracking data, the escalating conflict in the Middle East has sharply increased global oil prices. This drastically increased the dollar-denominated cost of Indonesia’s energy imports right as domestic revenues were stalling.

-

The “Higher for Longer” US Dollar: Based on US Federal Reserve policy tracking, US interest rates remained stubbornly high. Global capital naturally flowed to safe-haven US Treasury yields. The combination of high US yields and domestic fiscal uncertainty made Indonesian assets highly unattractive.

-

Squeezed Middle Class: Based on inflation tracking by Statistics Indonesia (BPS), a weak Rupiah is driving import inflation. To manage the soaring cost of oil, the government hiked non-subsidized fuel prices (Pertamax) by 32% in early June. This acts as a direct tax on logistics and basic consumer goods.

-

Aggressive Monetary Tightening: Bank Indonesia’s rapid rate hikes to 5.75% have successfully stabilized the currency, but according to banking sector forecasts, these higher borrowing costs will squeeze domestic credit, slowing down real estate, manufacturing, and business expansion.

-

According to regional financial analysts, a severely weakened Rupiah risks triggering localized capital flight if investors perceive systemic weakness in Southeast Asian assets. However, contagion has been limited so far because regional peers have differing fiscal fundamentals and varying degrees of dollar-denominated debt.

The breach of the 18,000 threshold was a harsh wake-up call. While Bank Indonesia’s emergency rate hikes successfully stopped the panic, they are only a temporary fix.

Based on the convergence of data from global markets and domestic fiscal trackers, the Rupiah’s historic plunge was a symptom of both external headwinds and internal complacency.

Until the government realigns its fiscal ambitions with its actual revenue, and global energy markets stabilize, the Indonesian economy will remain fundamentally on the defensive.

(ARS/QOB)

{kind=link}

{kind=link}

{kind=link}

{kind=link}