Why the rupee-dollar equation matters more than ever for India’s auto industry

The Indian rupee moving closer to the psychological mark of ₹100 against the US dollar may sound worrying for consumers, importers and policymakers. But for India’s manufacturing sector — especially export-oriented industries — a weaker rupee also opens up an interesting strategic opportunity.

For the automotive industry, the impact is even more nuanced. India is no longer just a domestic vehicle market. It is gradually becoming a global production base for small cars, SUVs, two-wheelers, commercial vehicles, tractors, auto components and increasingly, EV-related parts. From Maruti Suzuki shipping made-in-India vehicles to Latin America and Africa, to Bajaj, TVS and Royal Enfield building strong global two-wheeler franchises, the country’s auto industry already has a meaningful export engine.

A weaker rupee can make this export engine more competitive. But it can also raise the cost of imported components, electronics, batteries, semiconductors, rare-earth magnets, tooling, machinery and crude-linked inputs. That is why the rupee at 100 is not a simple good-news or bad-news story. It is a stress test of how localised, export-ready and globally competitive Indian manufacturing really is.

The simple logic: a weaker rupee makes Indian exports cheaper

When the rupee weakens against the dollar, Indian-made products become relatively cheaper for overseas buyers. For an exporter billing in dollars, the same export price converts into higher rupee revenue. This improves margins, gives exporters more pricing flexibility and helps Indian companies compete better against suppliers from China, Thailand, Vietnam, Indonesia, Mexico and Eastern Europe.

For example, if an Indian auto component supplier exports parts worth USD 1 million, the rupee revenue at ₹85 per dollar is ₹8.5 crore. At ₹100 per dollar, the same USD 1 million billing becomes ₹10 crore. The company may choose to retain the additional margin, pass on part of the benefit to global customers, or invest in capacity and product development.

This is why currency depreciation can help export-heavy manufacturers. It creates an immediate arithmetic benefit. However, the real advantage depends on how much of the product is actually made in India.

Auto sector: where the opportunity is strongest

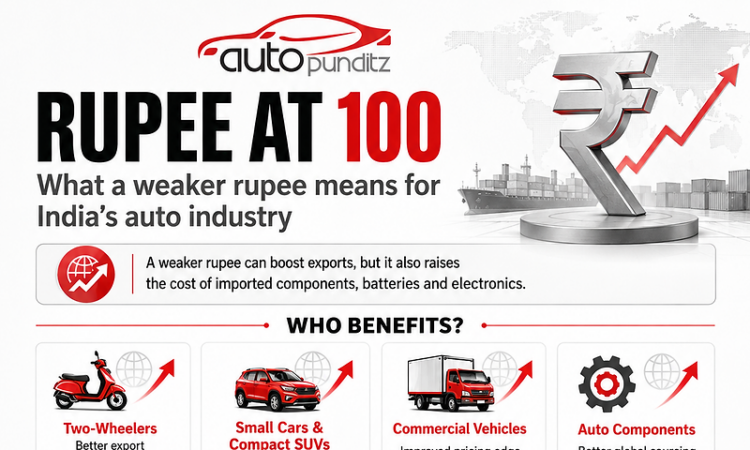

The biggest beneficiaries of a weaker rupee are likely to be segments where India already has strong domestic manufacturing depth and export credibility.

1. Two-wheelers

India is one of the world’s strongest two-wheeler manufacturing hubs. Companies such as Bajaj Auto, TVS Motor, Hero MotoCorp and Royal Enfield have spent years building export markets across Latin America, Africa, South Asia, ASEAN and parts of Europe. Two-wheelers have relatively high local content compared to many new-age EV products. India has scale, supplier depth and engineering familiarity in motorcycles and scooters. This gives Indian two-wheeler exporters a natural advantage when the rupee weakens.

A cheaper rupee can improve their competitiveness in price-sensitive export markets, especially where Chinese and Japanese brands are strong. It can also help Indian brands hold margins despite freight, finance and market-development costs.

2. Small cars and compact SUVs

India has historically been a strong base for small car exports. Maruti Suzuki, Hyundai, Kia, Nissan, Renault, Honda and Toyota have used Indian factories to serve global markets. The opportunity is now expanding from hatchbacks and sedans to compact SUVs and crossover-style products.

Global demand is shifting toward affordable SUVs, and India is well placed to supply such vehicles because the domestic market already has a huge compact SUV ecosystem. If Indian-made SUVs can meet safety, emission and feature expectations in export markets, a weaker rupee can make them more attractive. This is particularly important as India tries to move from being a low-cost assembly base to a design-and-engineering-led export hub.

3. Commercial vehicles

Commercial vehicle exports are highly sensitive to price, financing, service support and operating cost. Indian CV makers such as Tata Motors, Ashok Leyland, Mahindra and Eicher have a long presence in South Asia, Africa and the Middle East.

A weaker rupee can support Indian CV exports in markets where fleet operators compare upfront cost very closely. Buses, trucks and light commercial vehicles from India can become more competitive against Chinese, Japanese and used-import alternatives. However, CV exports also depend heavily on economic stability in destination countries. Currency benefit alone cannot offset weak demand, political instability or financing constraints in export markets.

4. Auto components

Auto components may be one of the most important opportunities in the rupee depreciation story. India’s component industry has gradually moved from being a low-cost supplier to a quality-driven global sourcing base.

Engine parts, transmission components, forgings, castings, suspension parts, wiring harnesses, tyres, lighting systems, precision components and aftermarket parts all have export potential. A weaker rupee improves price competitiveness for Indian component makers supplying global OEMs and Tier-1 companies.

This is also where India can benefit from global supply-chain diversification. Many automakers and component majors are looking beyond China for resilient sourcing. India can use the currency advantage, but only if it can match global quality, delivery discipline and technology standards.

The catch: India still imports too much of the future vehicle

The positive export story has a major limitation. A weaker rupee also makes imports costlier. This matters because modern vehicles are increasingly dependent on imported content.

Today’s cars and two-wheelers are not just steel, glass, rubber and engines. They are becoming electronic, software-defined and battery-heavy products. The future vehicle depends on several import-intensive items:

Semiconductors, sensors, ADAS hardware, display units, electronic control modules, lithium-ion cells, battery management systems, magnets, power electronics, specialised steel, aluminium, chemicals and certain precision tooling are still heavily dependent on global supply chains.

This means an automaker exporting vehicles from India may benefit from a weaker rupee on the revenue side, but lose part of that benefit if imported inputs become expensive. The same applies to EVs even more sharply. For internal-combustion vehicles, India has built significant localisation over decades. For EVs, localisation is still evolving. Battery cells, rare-earth magnets and power electronics remain key pressure points. So, a weaker rupee helps only when the domestic value addition is high.

Why localisation becomes the real currency shield

The rupee at 100 debate should not be seen only as a forex issue. It should be seen as a localisation issue.

If India wants to benefit from a weaker currency, it needs deeper domestic manufacturing in critical areas. The country cannot rely only on final assembly. It needs stronger local ecosystems for batteries, electronics, semiconductors, electric motors, magnets, tooling, software integration and advanced materials.

For automakers, this means the next phase of competitiveness will come from three levers:

-

First, higher local content. The more parts made in India, the more the company benefits from a weaker rupee.

-

Second, stronger export product planning. Vehicles must be designed for multiple markets from day one, not adapted later as an afterthought.

-

Third, supplier capability. Indian vendors must move up the value chain from cost-led parts to technology-led modules.

-

This is where the rupee can act as a catalyst. It can reward companies that localised early and expose those that remain import-dependent.

What it means for carmakers in India

For passenger vehicle makers, a weaker rupee creates both opportunity and pressure.

Export-heavy manufacturers can gain. Maruti Suzuki, Hyundai, Kia, Nissan, Volkswagen-Skoda, Honda and Toyota have all used India as an export base at different levels. A weaker rupee improves the export business case for made-in-India models.

However, domestic market pricing can become challenging. If imported components become costlier, companies may either absorb the hit or pass it on to customers through price hikes. This can affect affordability, especially in entry-level segments where demand is already price-sensitive.

Luxury carmakers may face more pressure because many models are imported as CBUs or assembled from CKD kits. A weaker rupee can increase landed costs and make premium vehicles more expensive. This may not stop demand at the top end, but it can affect pricing and variant strategy.

EV makers may also face margin pressure if battery and electronics imports remain high. Unless battery localisation improves, rupee depreciation can make EV cost structures more difficult.

What it means for two-wheeler makers

Two-wheeler makers may be better placed than carmakers because the segment has deeper localisation and strong export experience.

Bajaj Auto and TVS Motor are among the clearest examples of companies that can benefit from export tailwinds. Royal Enfield, with its premium motorcycle positioning, can also gain as global revenues translate into higher rupee realisation.

Hero MotoCorp, while more domestic-focused historically, has also been trying to strengthen its global presence. A weaker rupee can make export expansion more attractive for such players.

However, two-wheeler makers are not fully insulated. Premium motorcycles use more electronics, fuel-injection systems, ABS modules, sensors and imported technology inputs. Electric two-wheelers are even more exposed to battery and electronics costs.

So, the advantage is strongest in high-localisation ICE two-wheelers and export-ready models.

What it means for auto component makers

Auto component manufacturers may be among the biggest strategic beneficiaries. India’s component industry is already supplying global OEMs and aftermarket networks. A weaker rupee can help them offer competitive pricing without sacrificing margins.

But the sector must avoid becoming only a low-cost supplier. The real long-term opportunity is in high-value components, EV parts, electronics, precision manufacturing and global platform supplies. If Indian component companies use the rupee advantage to invest in technology, quality systems and capacity, they can capture a larger share of global sourcing. If they only compete on price, the benefit may be temporary.

Consumer impact: imported inflation can reach the showroom

For customers, the rupee weakening is unlikely to feel positive. Even if exports gain, domestic buyers may face price increases.

Automakers may raise prices to offset costlier imported parts, freight, commodities and currency hedging costs. This is especially true for vehicles with high electronics content, EVs, hybrids and premium models. Spare parts may also become costlier where import content is high. Insurance, maintenance and replacement costs can rise over time. Tyres, batteries, lubricants and electronic modules may see indirect pressure if input costs increase. Therefore, while manufacturers may benefit from export competitiveness, consumers may face higher vehicle ownership costs.

Policy angle: currency alone cannot build manufacturing strength

A weaker rupee can support exports, but it cannot replace industrial policy, infrastructure, technology depth and scale. Countries do not become manufacturing powers simply by weakening their currencies.

India needs stable logistics, faster ports, reliable power, lower compliance burden, better supplier financing, skilled labour, R&D support and predictable trade policy. It also needs better integration with global value chains.

The biggest risk is assuming that rupee depreciation automatically creates an export boom. It does not. Export growth requires product-market fit, quality consistency, global certification, aftersales support, brand trust and long-term customer relationships. For the auto sector, this means India must build products that global customers want — not just products that become cheaper because of currency movement.

The China comparison

China did not become a manufacturing superpower only because of currency management. It built scale, supplier clusters, port infrastructure, technology absorption, aggressive exports and deep domestic manufacturing networks.

India’s auto industry has some of these ingredients, but the ecosystem is uneven. ICE vehicle manufacturing is mature. Two-wheelers are globally competitive. Auto components are gaining ground. But EV batteries, semiconductors, rare-earth magnets and advanced electronics remain weak spots.

This is why the rupee at 100 could be useful for India only if it is accompanied by deeper localisation and supply-chain strengthening.

Who wins and who loses?

The winners are likely to be export-heavy companies with high local content. These include two-wheeler exporters, component makers, small car exporters and commercial vehicle makers with strong overseas networks.

The companies under pressure are likely to be those dependent on imported parts, imported kits, dollar-denominated technology payments or imported batteries. Domestic consumers may not benefit directly. In fact, they may see higher prices if input costs rise.

The government may see improved export competitiveness, but it will also need to manage inflation, oil import costs and currency stability.

Auto Punditz view

A rupee near 100 against the US dollar would be a major psychological moment for India. But for the auto industry, the more important question is not whether the rupee is weak or strong. The real question is whether India’s automotive ecosystem is localised enough to benefit from a weak currency.

For companies that manufacture deeply in India and export aggressively, the weaker rupee can be a tailwind. For companies that depend heavily on imported electronics, batteries, kits and technology, it can become a margin problem.

The Indian auto industry is standing at an important point. It has the scale, engineering base and cost advantage to become a bigger global export hub. But the next leap will require more than currency support. It will require localisation of future technologies, stronger supplier ecosystems and products designed for global markets.

In short, a weaker rupee may improve India’s export math. But only stronger manufacturing depth can improve India’s export destiny.

{kind=link}

{kind=link}

{kind=link}

{kind=link}