Summary of key points: –

- The war premium unwinds in currency markets – what’s next?

- Fed member composition changing, however remains uncertain

If there was ever proof that most of the reaction by financial, investment and energy markets to the Iranian war over the last six weeks was largely speculative in nature and force, it is the price action over the last week where the war premium has been completely reversed out. The ceasefire in Lebanon and the reopening of the Strait of Hormuz to shipping has stimulated a massive unwinding of speculative positions in not only the oil market, but also in bond, equity, and currency markets: –

- West Texas Index crude oil prices started the week at US$104.50/barrel and have since crashed 20% to end the week at US$83.85/barrel. Further decreases below US$80.00/barrel are likely over coming days. It would not be too surprising at all to see the oil market return prices all the way down to US$65/barrel where they were trading in late February before the wat started, as many more speculative traders unwind their long oil positions. The “oil shock” risk event is largely over – well, that is what the oil price collapse is telling us.

- US 10-year Treasury Bond yields started the week at 4.35% and closed the week at 4.25%. Falling oil prices should see a continuation in the decreases of the bond yield to 4.00% over coming weeks.

- The Dow Jones Index commenced the week at 47,600 and closed at 49,440. After dropping 8.50% through the month of March, US equity markets have fully recovered to the levels prevailing before the Iranian war started in late February.

- The US Dollar Dixy Index was sitting at 97.60 when the war started on 28th February. It quickly appreciated to a high of 100.40 on 13th March on safe haven/speculative USD buying. However, over the last 12 days the long-USD punters have progressively unwound their positions (i.e. became USD sellers) as they concluded that the probability had increased that the war would end sooner rather than later.

The Australian dollar exchange rate against the US dollar was priced at 0.7120 when the war started on 28th February. It bottomed-out at 0.6850 on 30th March, however the AUD has recovered dramatically over the subsequent 18 days to currently trade at a higher 0.7170 level. The NZD/USD exchange rate has not yet fully recovered its war-related sell-off. The Kiwi dollar was trading at 0.6000 on 28th February, depreciated to a low of 0.5680 on 3rd April and has now only partially recovered to 0.5890. There is no clear explanation is to why the NZD has lagged the latest AUD appreciation against the USD. The likely answer is that our 90-day to two-year interest rates remain below those of the US, whereas Australian 90-day to two-year interest rates are 0.75% above US interest rates. In other words, buyers and holders of Aussie dollars are paid the FX forward points to do so, that is not yet the case for the Kiwi dollar.

As is often the case with global geopolitical risk events such as we have witnessed in Iran over the last six weeks, the financial and investment markets rapidly “move on” to the next likely influencing forces and developments. As we have previously stated in this column, these risk events tend to be much more short-lived in intensity and impact than what most imagine when the shock first hits.

Looking ahead, relative economic trends and developments over the balance of this year in both the US and New Zealand are now likely to have the most powerful influences over the NZD/USD exchange rate direction. However, expect volatility this week as progression towards a “peace deal” remains very fragile with many sticking points between the US and Iran still to be resolved.

In comparing our local NZ economic performance over coming months to the that of the US economy, what should be understood is that both central banks, the RBNZ and the Fed, will “look through” the one-off, short-term, and temporary adverse impact on inflation from the spike up in the oil price. Both central banks should have more confidence about this approach to monetary policy management today, than what they would have had just one week ago.

Therefore, discounting out the temporary adverse impact of higher oil prices on inflation and consumer spending (which is the same for both economies), the comparative trends of GDP growth, core inflation, and employment in the two economies are summarised as follows: –

|

|

USA |

New Zealand |

|

GDP growth |

December 2025 quarter GDP growth was originally measured at an annual rate of +1.40%, however it has been subsequently revised down to just +0.50%. March 2026 quarter data is due for release on 30th April, consensus forecasts range from +1.0% to +1.8% annual rate. Record low consumer confidence points to an actual result below such forecasts. Consensus forecasts for the full year 2026 have moderated to +2.00% with enhanced productivity from AI applications supporting the expansion. |

December 2025 quarter GDP growth came in at a disappointing +0.20%, following the robust 0.90% expansion in the September 2025 quarter. The annual rate of growth was +1.30%. March 2026 quarter figures are not released until 18th June. In a knee-jerk reaction, several local economic forecasters have sharply lowered their 2026 GDP growth outlook to below 2.00%, due to the Iran war/oil shock. Exports and manufacturing are proving to be resilient, pointing to annual GDP growth rate of +3.00% still being achieved this year. |

|

Core inflation |

The annual core inflation rate (which excludes food and energy) is running at 2.60% to 31st March 2026. Shelter costs continue to decline and higher imported goods prices from tariffs last year are not repeated this year. Weaker consumer demand should see monthly core inflation results remain between 0.00% and +0.20% over the rest of 2026. Fed members should come around to increasing confidence about annual core inflation, reducing to their target of +2.00% over the course of 2026. |

Inflation increased 1.00% in the September 2025 quarter and by +0.60% in the December quarter, lifting the annual rate of inflation to 3.10%. March 2026 quarter inflation numbers are due for release this week on Tuesday 21st April. Forecasts are for a quarterly increase of +0.60% to +0.80%. The annual rate of inflation will ease a tad as the large 0.90% increase in the March 2025 quarter drops out of the annual figures. The RBNZ forecast of the annual inflation rate reducing to 2.30% by December 2026 appears highly unlikely to happen. Post-war rebounding consumer demand and repeated price hikes from non-competitive sectors suggests annual inflation remaining above 3.00% in 2026. |

|

Employment |

Immigration restrictions have led to fewer people looking for work and therefore the unemployment rate has been stable at 4.30%, despite there being almost no increase in new jobs over the last nine months. April Non-Farm Payrolls jobs data on 9th May is likely to be negative, following the large (and likely revised lower) 178,000 increase in jobs in March. |

December 2025 unemployment rate of 5.40% is likely to be the peak of the cycle. March 2026 quarter employment growth is forecast to be +0.30%, which will lower the unemployment rate to 5.30%. The short-term nature of the oil shock over the last six weeks is unlikely to reduce hiring intentions this year. Further reductions in the unemployment rate over 2026 should see the rate fall below 5.00% by the end of the year. |

The weaker employment outlook in the US still points to two or three Fed 0.25% interest rate cuts in the second half of 2026. The full employment side of their dual mandate outweighing any lingering concerns that core inflation may stay higher for longer.

On the other hand, New Zealand’s core inflation rate (excluding food and energy) is likely to trend higher than RBNZ forecasts, forcing an impending rethink as to whether a 2.25% OCR is still appropriate. The RBNZ is unlikely to be as bold as the ANZ view of three x 0.25% pre-emptive OCR interest rates hikes before the general election in November, however two hikes seem likely to return the OCR to somewhere near neutral sooner, rather than later.

What does all this mean for the NZD/USD exchange rate?

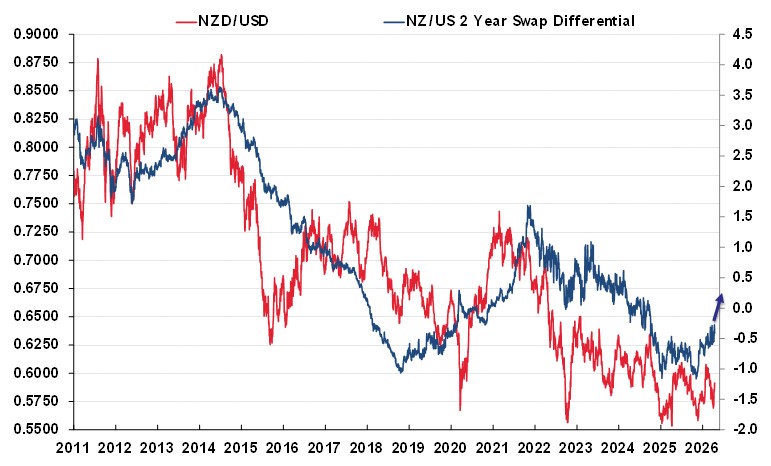

Collapsing oil prices put US two-year swap interest rates on the cusp of dropping from the current 3.80% to somewhere closer to 3.25% over coming weeks/months. The price change reflecting more market participants expecting the Fed to cut at least twice this year. New Zealand two-year swap interest rates have lifted from 2.50% in November 2025 to 3.40% currently. Given the NZ economic and inflation outlook, post the oil price shock that has come and gone, our two-year swap interest rates is not going to suddenly decrease and could even increase further.

The current US:NZ two-year interest rate differential of -0.40% (NZ rates 0.40% below US rates) is about to reverse to +0.25% as US interest rates decrease to below those of New Zealand (refer chart below). The correlation of the NZD/USD exchange rate to the two-year swap differential is plain to see. The probability of the NZD/USD rate following the Aussie dollar’s example (of positively responding to the changed interest rate differential position over recent months) is certainly increasing.

Fed member composition changing, however remains uncertain

Just how far the US dollar may depreciate this year depends heavily on the timing and extent of Fed interest rate cuts. Fed decision making to cut rates is in turn dependent upon the composition of the 12-voting members of the FOMC committee. The predisposition of those members to how interest rates should be adjusted to future expected employment and inflation conditions really determines the Fed’s decisions and messaging to the markets. Financial and investment market pundits run “cheat-sheets” as to which voting members are at the “dovish” end of the spectrum on the economy and interest rates and which members sit at the “hawkish” end of the spectrum and will not vote for interest rate cuts. A number sit in the middle and can swing either way.

The 2026 voting members currently line up on the dovish/hawkish spectrum as follows: –

- Doves = Miran, Walker, Bowman, Jefferson, Paulson, Cook, Powell and Willams (8)

- Fence-sitters = Barr and Kashkari (2)

- Hawks = Logan and Hammack (2)

If you read of speeches by the other seven non-voting members of the Fed on the timing and extent of interest rate changes, it pays not to take too much notice as they have no vote (namely, Daly, Venable, Goolsbee, Barkin, Collins, Musalem and Schmid). All 19 members submit their individual “dot-plot” interest rate forecasts, however only 12 members vote on interest rate decisions.

The current voting member composition is heavily weighted in favour of interest rate cuts (doves), however they will need to be convinced that tariffs and temporary high oil prices have not materially lifted longer-term inflationary expectations. On the expectation that oil prices return to pre-war levels, it may still take several months before the Fed can observe these inflationary expectations surveys stabilising. In the meantime, all the other economic data will influence interest rate market pricing on the timing and extent of cuts. Best case, in out view, would be the first cut at the 17th June meeting where the full economic projections are considered.

The US Senate Banking Committee is set for a hearing this Tuesday 21st April to approve the nomination of Kevin Warsh as the new Federal Reserve Chairman. Jerome Powell’s term as Chair ends on 15th May, however he is entitled to stay on as an ordinary member as his term for that role does not expire until 31 January 2028. Jerome Powell has not yet indicated whether he will stay on, or not. President Trump could still fire him as a member if Powell decides to stay, replacing him with another Trump plant that favours lower interest rates.

The confirmation of Kevin Warsh as the new Chair on 15th May is an unholy mess. Republican Senator, Thom Tillis on the Senate Banking Committee is stating that he will hold out from approving Mr Warsh until President Trump and the Department of Justice resolves the criminal investigation into Chair Powell in respect to the Fed’s building renovation cost overruns. To date, that has not been resolved. Unless Senator Tillis changes his stance, the installation of Kevin Warsh as the new Fed Chair will be delayed beyond 15th May.

When Kevin Warsh does eventually move into the Chair and Jerome Powell resigns or his sacked, there will be two new Fed voting members who are Trump appointees favouring lower interest rates.

Select chart tabs

*Roger J Kerr is Executive Chairman of Barrington Treasury Services NZ Limited. He has written commentaries on the NZ dollar since 1981.

{kind=link}

{kind=link}

{kind=link}

{kind=link}