Sandisk Is the Best-Performing S&P 500 Stock During the First Half of 2026. Here’s What Stock I Think Will Dominate the Second Half (Hint: It’s Not SpaceX)

The S&P 500 as a whole has had a solid 2026 so far, rising nearly 10%. If it continues this trend throughout the rest of 2026, the index would return a decent amount ahead of the 10% annual returns investors normally pencil in for the S&P 500. However, individual components within the S&P 500 have had far different experiences in 2026.

The best stock in the S&P 500, Sandisk (SNDK 14.00%), is up around 800%. The worst stock, Intuit, is down around 60%. That’s quite a delta in performance, but how will these stocks fare in the second half?

Let’s take a look at why Sandisk rose to the top and which stock could be the best-performing stock in the second half of 2026.

Image source: Getty Images.

Sandisk is thriving from a memory chip shortage

Unless you’ve been living under a rock, you’ve likely noticed that one of the biggest overarching themes in the stock market is the artificial intelligence (AI) data center build-out. This is creating a ton of activity in the chip space, as well as in the construction industry. However, it’s stretching some industries thin.

The biggest shortage right now in the data center space isn’t energy capacity, land, or labor; it’s memory chips. The memory chip industry just isn’t built for this kind of demand wave, and when demand is high and supply is low, prices skyrocket. Sandisk has benefited from these economic mechanisms, and it’s the reason why the stock is soaring.

Today’s Change

(-14.00%) $-284.60

Current Price

$1747.62

Key Data Points

Market Cap

$258B

Day’s Range

$1693.79 – $2052.00

52wk Range

$40.10 – $2354.39

Volume

550K

Avg Vol

13.6M

Gross Margin

56.04%

Many in the industry predict that this memory chip shortage won’t be alleviated in 2026 or in 2027, so there is still a lot of room for Sandisk to run. So, just because Sandisk had a strong start to 2026, it doesn’t mean that it won’t finish among the top companies. However, I think there is another candidate that could be an excellent investment, and it may surprise you.

Nvidia could arise from its slumber

Although Intuit is the worst performer in the S&P 500 so far, I highly doubt it will rise to become the best performer in the second half. Instead, I’m betting on Nvidia (NVDA 1.39%). This may sound odd, as Nvidia is the world’s largest company by market cap. But I think it could have an incredible second half of 2026, and investors need to buckle their seatbelts for the returns it’s about to deliver.

The investment thesis behind Nvidia’s stock is simple: The AI buildout is going to boom through the rest of 2026, into 2027, and beyond. As a result, it’s not uncommon to see future growth get priced in, but there is none of that in Nvidia’s stock beyond the end of 2026. This primes the stock for huge gains in the second half of 2026, especially as investors realize there will be more spending in 2027.

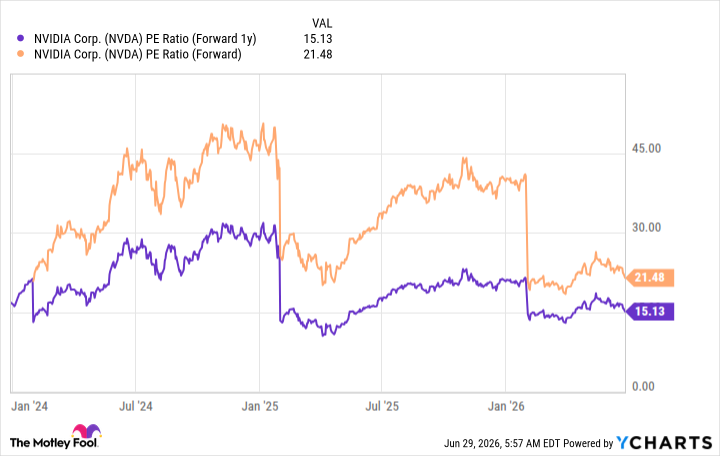

Nvidia’s stock is up only 5% so far in 2026, but I think it could post gains of nearly 100% by the end of 2026 if historical trends persist. Right now, Nvidia trades for 21.5 times forward earnings — the same as the S&P 500.

NVDA PE Ratio (Forward 1y) data by YCharts

However, in each of the past two years, Nvidia has ended the year trading at 40 times forward earnings or greater. If Nvidia can rise to that level again, we could see the stock double in value. Even if it doesn’t, Nvidia is priced at 15 times next year’s earnings, which is a very low price to pay for a stock growing as quickly as Nvidia is.

Even if Nvidia isn’t the best-performing stock in the second half of 2026, I still think it will rank among the top performers and be a great one to hold onto from now through the end of 2026. If you’ve got some spare investment dollars sitting around, Nvidia may be a great place to deploy them to.

{kind=link}

{kind=link}

{kind=link}

{kind=link}