As stock prices continue to soar, fears of an AI bubble are increasing. The tech bubble of the 1990s was driven by fear of missing out (FOMO). This time, fabulous earnings momentum (FEMO) is driving tech stock prices higher. An earnings-led meltup like this should be more sustainable than a P/E-led meltup fueled by irrational exuberance. That’s especially true of FEMO meltups, like this one, that have been climbing a wall of worry.

Consider the following:

(1) Stock prices. The S&P 500 closed at a record 7,580.06 on Friday, 11.0% above its 200-day moving average (chart). The equal-weight index closed at 8,442.40, 7.2% above its 200-dma. Both are elevated and may pull back.

On May 10, we raised our year-end target for the S&P 500 from 7,700 to 8,250. We are sticking with it.

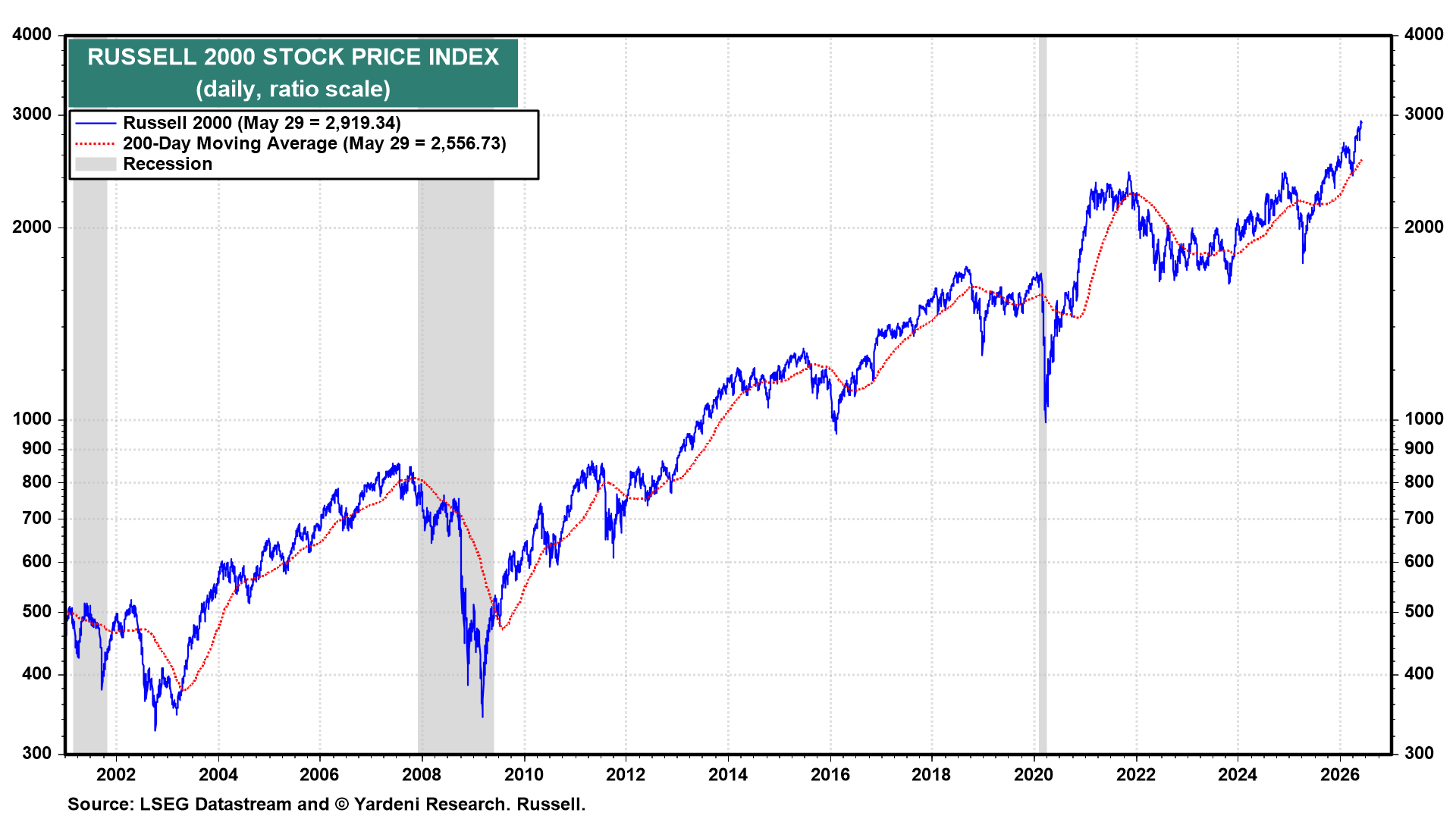

On Friday, the Russell 2000 closed at a record 2,919.34, 14.2% above its 200-dma (chart). We expect that the stock market’s breadth will continue to broaden once the Gulf War ends.

(2) S&P 500/400/600 earnings. S&P 500 forward earnings is at a record high. The latest analysts’ consensus has S&P 500 operating EPS at $339.24 for 2026 and $394.52 for 2027 (chart). When we raised our year-end S&P 500 target to 8,250, we raised our comparable earnings forecasts to $330 and $375. The analysts are even more bullish than we are. We might have to follow their lead again.

{kind=link}

{kind=link}

{kind=link}

{kind=link}