House prices in the south of England are extending their decline, while the fastest growing local authority areas continue to be in the north, analysis by the deVere Group shows.

It paints an uneven picture of the UK property market, which has gone into reverse, with the traditionally more expensive south slipping, while many areas once considered “left behind” are appreciating.

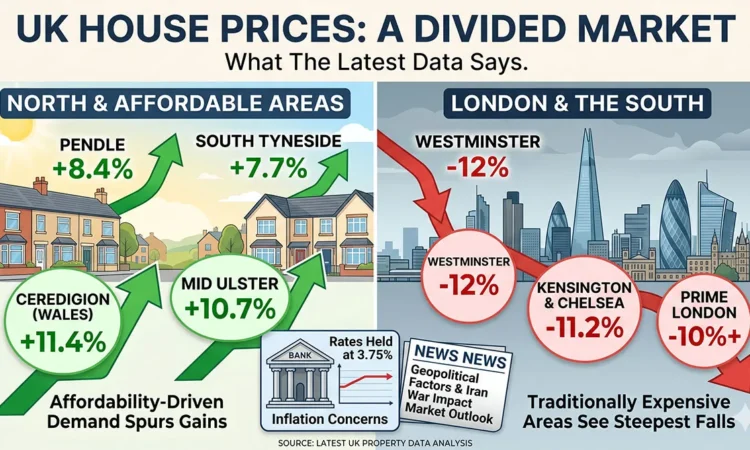

While UK house prices have fallen every month since November 2025, the fall has been felt most acutely in the south, with the latest data showing prime London properties down more than 10 per cent year on year.

Conversely, traditionally affordable areas are seeing the largest gains, as a result of affordability-driven demand, making the north-south divide the defining story of the UK property market right now.

Where Are House Prices Falling?

The average house price in England has fallen every month since November 2025, ONS data shows, but the market has been dragged down by London and the south, where prices have cratered.

The worst hit areas include Westminster, down 12 per cent, Kensington & Chelsea, down 11.2 per cent and the City of London, down 11.2 per cent on this time last year.

Analysis by deVere shows that one third of local authority areas saw property depreciation over the past year, while two thirds stood still or rose in price.

The most pronounced property price increases came in areas where houses are less than £225,000 on average, including in Pendle, where prices are up 8.4 per cent, and South Tyneside, where prices rose by 7.7 per cent.

However, just as Kensington & Chelsea remains the most expensive local authority area for housing, despite the fall in prices, areas like Burnley and Hartlepool remain amongst the cheapest, despite their recent gains.

The Best Performing Areas for Property in the UK

For years, it has been London property that has boomed, but the capital appears to be taking a step back, while more remote and some underserved locations become the standout stories.

In the 12 months to February, house prices gained 11.4 per cent in the remote Welsh country of Ceredigion. The region, which sits off the cost of the Irish sea, continues to beat the national, and local trend, to defy some of the headwinds impacting the market and draw demand.

Properties in many areas of Northern Ireland continue to appreciate, with properties in Mid Ulster up 10.7 per cent, and Newry Mourne and Downe up 12.4 per cent, just two of numerous local authority areas which saw double digit gains on average house prices.

It’s a sharp reversal after an extended London property price boom, which appears to have let up for now, while often overlooked areas of the UK come into view as more affordable alternatives.

Why The London Property Market Could Bounce Back

While London property prices are under pressure right now, and the worst may not yet be behind the market, there are reasons to remain optimistic in the medium to long term.

In recent years, tens of thousands of high-net-worth Brits are thought to have emigrated, with many choosing to relocate to the Gulf.

This has necessarily been felt by the London property market, particularly on the high end, where there appear to be a shortage of buyers.

An estimated 240,000 British nationals now live in the UAE alone – but the British government is hoping to woo them back.

A reported one in eight Brits have already departed from the region since the start of the US Iran war, and the Treasury is hoping more will follow.

The Chancellor, Rachel Reeves, recently made a direct appeal to expats, encouraging them to return to the “safe harbour” of Britain, amid the dangers of the war.

The potential influx of Brits from abroad, combined with a return to office working and a fall in London property prices, could prove to be catalysts for a bounce back.

But any upside will, at least for now, struggle against the prevailing headwinds. A favourable interest rate outlook has been dashed by the Iran war, and inflation is on the up.

Traders have scaled back their expectations for interest rate cuts, weighing on borrowers and as a result, the housing market.

Economists at the Bank of England have hinted an April 30 cut is all but ruled out, having abandoned their 2 per cent target by spring 2026, noting the Iran war will mean “inflation will be higher than we expected, at least in the short term.”

However, when the smoke clears, and inflation returns to normal – assuming the Iran war doesn’t spiral out of control, there are some signs of a revival on the horizon.

Where Are the Cheapest Houses in the UK?

The cheapest average house prices can be found in Wales, with the cheapest 21 local authority areas all found in the country.

The cheapest local authority area for housing is Blaenau Gwent, where houses are on average £137,891.

The area also saw among the largest gains over the past 12 months, with prices up 5 per cent. Similarly, Rhondda Cynon Taf, the fourth cheapest area, saw properties gain in value by 7.1 per cent in the same period.

West Dunbartonshire, where prices rose 7.4 per cent, is the second cheapest area in Scotland, and Mid and East Antrim remains the cheapest area in Northern Ireland, but saw an 8.1 per cent rise in average house prices.

It’s the same story in England, with the cheapest areas seeing the biggest rises. The lowest cost, on average, for a house can be found in Burnley, up 4.7 per cent, and in Pendle, up 8.4 per cent.

What’s Next For UK House Prices According to the Experts

The outlook for the UK housing market was bullish at the beginning of 2026, but the Iran war and the fallout resulting from it has had a material and deleterious impact.

When US and Israeli forces struck Iran on 28 February, swap rates, the mechanism through which global events translate into mortgage costs, surged to multi-month highs within days.

Banks and building societies withdrew over 1,500 mortgage products in under a fortnight, and two-year fixed rates climbed from around 4.8 per cent to about 5.5 per cent on the news.

Commenting on the change of circumstances, Tarrant Parsons, of the Royal Institute for Chartered Surveyors, said:

“What had been a cautiously improving picture for activity has been knocked off course by the wider macro fallout from the Middle East conflict.

“With average fixed rates climbing back above 5 per cent, it is unsurprising that buyer demand has softened.”

It comes as new buyer enquiries fell to a net balance of -39% in March, the weakest reading since August 2023.

The Bank of England, which had been widely expected to cut in March, held at 3.75 per cent. Its next meeting falls on 30 April, and if the conflict is still running by then, economists believe the Bank may raise rates this year rather than cut them.

However, while London and the south east suffer, their loss is the gain of many underserved and overlooked areas across the UK. Northern Ireland was the best performing area in Q1 2026, with prices up 9.5 per cent year-on-year, while the outer South East saw a drop of 0.7 per cent.

That creates potential opportunities in the market, with high borrowing costs and a wealth exodus weighing on expensive London homes, we are seeing rising demand and prices in some of the cheapest areas of the country.

However, don’t count London and the south out yet – events in the Gulf may prove to be a catalyst for the repatriation of British nationals, inflation could still surprise to the upside, and the BoE may yet cut rates this year.

But even if things don’t go London’s way, it remains, in the long-term, a prized destination, a key hub of finance, and in international terms, a safe city, which will continue to attract families and professionals for years to come.

{kind=link}

{kind=link}

{kind=link}

{kind=link}