Is Multi‑Index S&P Inclusion Altering The Investment Case For First Advantage (FA)?

- On 11 June 2026, First Advantage Corporation (NasdaqGS: FA) was added to the S&P 600, S&P 1000, S&P Composite 1500, and the S&P 600 Industrials sector index, broadening its representation across key U.S. equity benchmarks.

- This multi-index inclusion increases the company’s visibility with institutional investors and index-tracking funds, potentially deepening liquidity and reinforcing its profile within the professional services and industrials universe.

- We’ll now examine how First Advantage’s fresh inclusion in several S&P indices may influence its existing investment narrative and outlook.

Outshine the giants: these 14 early-stage AI stocks could fund your retirement.

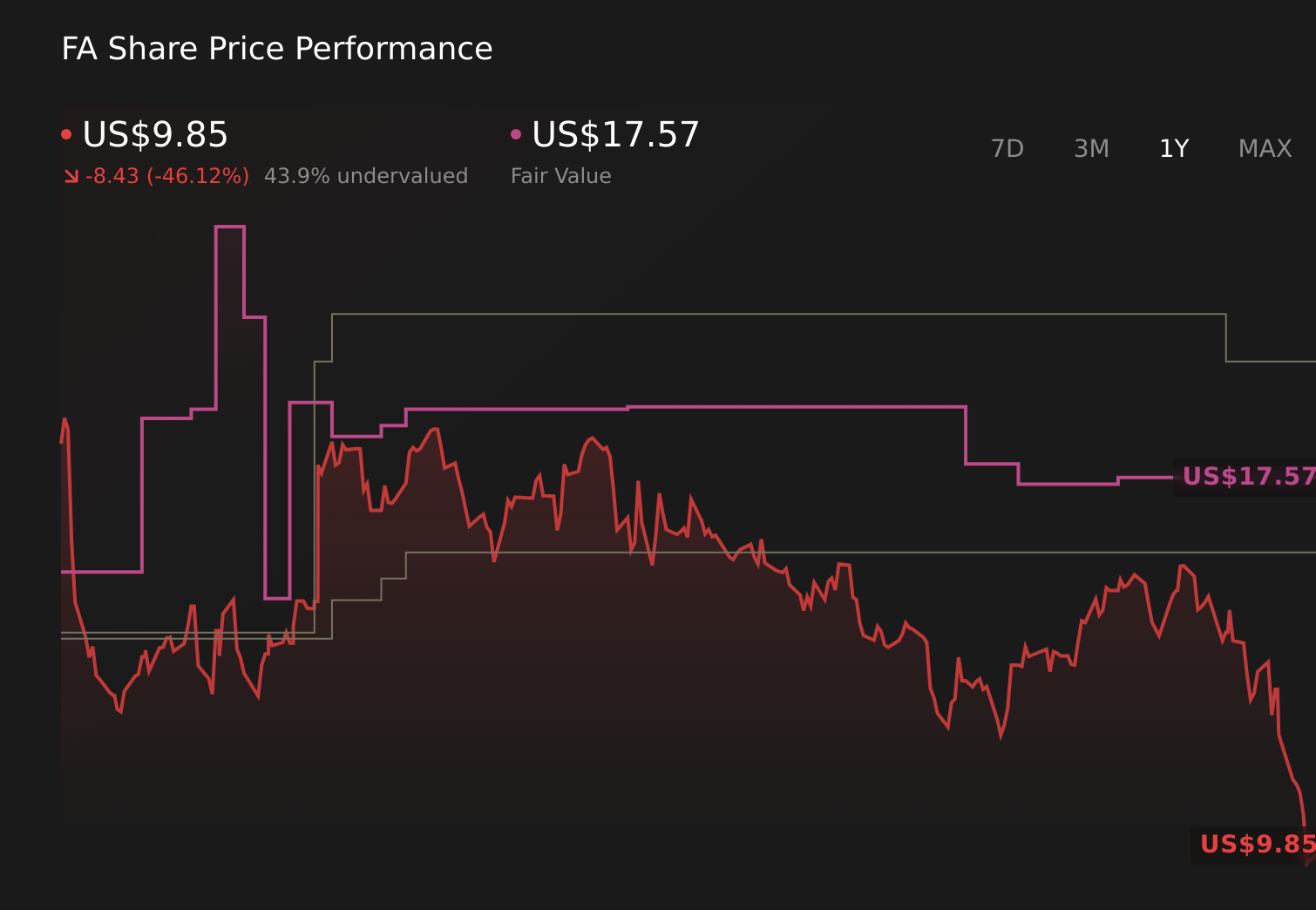

First Advantage Investment Narrative Recap

To own First Advantage, you have to believe that outsourced background screening and identity verification will keep gaining importance and that the Sterling acquisition and FA 5.0 technology push can eventually lift margins despite hiring hesitancy. The new S&P index inclusions may support trading liquidity and awareness, but they do not materially change the near term tug of war between a softer hiring backdrop and execution risk on Sterling integration.

The most relevant recent update alongside the index news is the reaffirmed 2026 revenue guidance of US$1,625 million to US$1,700 million, given after Q1 2026 revenue of US$385.2 million and a return to modest profitability. Paired with the new S&P index memberships and the ongoing US$100 million buyback authorization, this guidance frames how much confidence you place in management’s ability to offset hiring softness with upsell, cross sell, and acquisition synergies.

Yet beneath the index-related optimism, investors still need to be aware of how competitive pressures and a still-immature Digital Identity market could…

Read the full narrative on First Advantage (it’s free!)

First Advantage’s narrative projects $1.9 billion revenue and $210.5 million earnings by 2029. This requires 6.6% yearly revenue growth and about a $202 million earnings increase from $8.5 million today.

Uncover how First Advantage’s forecasts yield a $18.14 fair value, a 13% upside to its current price.

Exploring Other Perspectives

Some of the lowest analysts were already cautious, assuming revenue would climb to about US$2.0 billion by 2029 and earnings to roughly US$178.5 million, while worrying that Sterling’s lower margin mix could cap profitability. With First Advantage now added to several S&P indices, it will be important to see whether these more pessimistic views shift or if concerns about margin pressure and slower growth remain intact.

Explore 2 other fair value estimates on First Advantage – why the stock might be worth over 2x more than the current price!

Decide For Yourself

Don’t just follow the ticker – dig into the data and build a conviction that’s truly your own.

Contemplating Other Strategies?

Our top stock finds are flying under the radar-for now. Get in early:

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

{kind=link}

{kind=link}

{kind=link}

{kind=link}