Is Record Demand And Mexico Setback Altering The Investment Case For Royal Caribbean (RCL)?

- Earlier in 2026, Royal Caribbean Cruises reported a strong first quarter, with US$4.50 billion in revenue, 11% year-over-year growth, and earnings per share ahead of guidance amid record WAVE season bookings.

- At the same time, the company faced an environmental permitting setback for its planned Perfect Day Mexico destination, highlighting how regulatory reviews can complicate expansion even when demand and financial performance are robust.

- Next, we’ll examine how this combination of record demand and environmental permitting challenges may influence Royal Caribbean’s investment narrative.

Capitalize on the AI infrastructure supercycle with our selection of the 46 best ‘picks and shovels’ of the AI gold rush converting record-breaking demand into massive cash flow.

Royal Caribbean Cruises Investment Narrative Recap

To own Royal Caribbean Cruises, you need to believe that demand for cruising and its newer ships and destinations can support resilient earnings despite economic and regulatory uncertainty. The Q1 2026 beat and record WAVE season reinforce that demand remains strong, while the Perfect Day Mexico permitting denial underscores regulatory and environmental risk. For now, this setback appears more about timing and project execution than about the core near term catalyst of ship led yield growth.

The most relevant recent announcement is management’s outlook for roughly 10% revenue growth in 2026, issued alongside the strong Q1 results. That guidance frames how investors might think about the impact of Perfect Day Mexico delays, since it underpins expectations for earnings and cash flows that support ship orders, dividends, and destination investments. How well Royal Caribbean balances that growth ambition with tighter environmental scrutiny could shape how durable that outlook really is.

Yet behind the strong quarter, rising regulatory and environmental scrutiny could become a bigger issue that investors should be aware of…

Read the full narrative on Royal Caribbean Cruises (it’s free!)

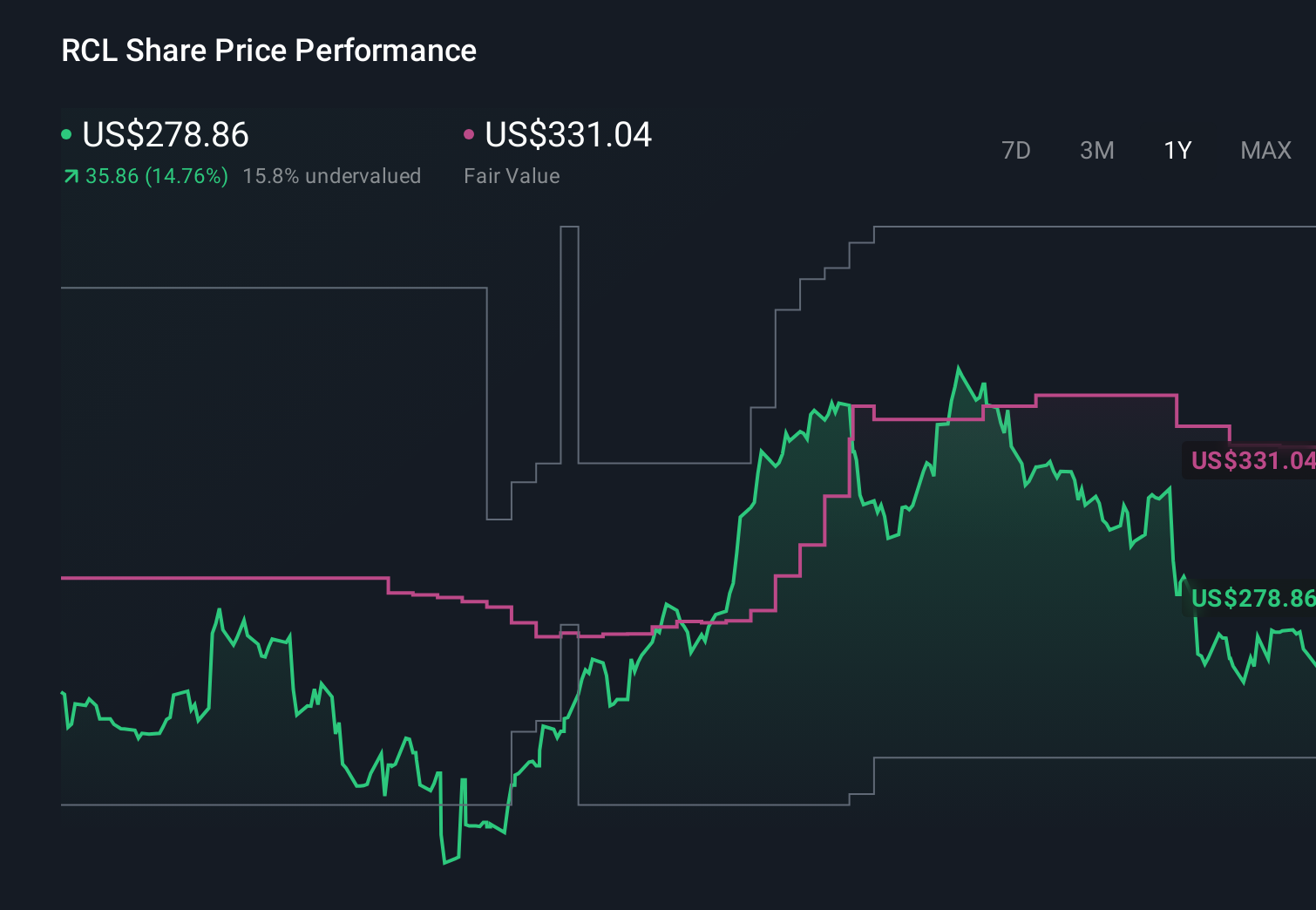

Royal Caribbean Cruises’ narrative projects $23.0 billion revenue and $6.1 billion earnings by 2029.

Uncover how Royal Caribbean Cruises’ forecasts yield a $348.46 fair value, a 36% upside to its current price.

Exploring Other Perspectives

Some analysts were far more optimistic before this news, assuming revenue could grow about 10.5% a year and earnings reach roughly US$6.9 billion, so you may find their more aggressive views on regulatory and cost risks either reassuring or concerning, depending on how you see Royal Caribbean’s path from here.

Explore 6 other fair value estimates on Royal Caribbean Cruises – why the stock might be worth just $268.88!

Reach Your Own Conclusion

Don’t just follow the ticker – dig into the data and build a conviction that’s truly your own.

Seeking Other Investments?

Right now could be the best entry point. These picks are fresh from our daily scans. Don’t delay:

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

{kind=link}

{kind=link}

{kind=link}

{kind=link}