Rising Institutional Interest and Brinsupri Focus Might Change The Case For Investing In Insmed (INSM)

- In recent days, Insmed drew attention as Raymond James initiated coverage highlighting the early Brinsupri launch, RBC Capital raised its expectations, and Vanguard Capital Management disclosed a passive 5.34% ownership stake of 11,514,893 shares as of March 31, 2026.

- Together with upcoming healthcare conference presentations, this mix of supportive analyst commentary and increased institutional ownership points to rising market focus on Brinsupri’s commercial rollout and Insmed’s broader inflammatory and pulmonary pipeline.

- Next, we’ll examine how this heightened institutional interest and upbeat Brinsupri commentary may influence Insmed’s existing investment narrative.

Uncover the next big thing with 23 elite penny stocks that balance risk and reward.

Insmed Investment Narrative Recap

To own Insmed, you need to believe Brinsupri can become a durable, high-uptake therapy in bronchiectasis while ARIKAYCE and the broader pipeline support long term growth. The key near term catalyst remains execution on Brinsupri’s commercial rollout, and the biggest current risk is access and reimbursement friction that could slow real world adoption. Recent analyst optimism and Vanguard’s passive stake raise attention on the story but do not fundamentally change these core drivers.

Among the recent announcements, Raymond James’ initiation and RBC’s increased expectations stand out because they focus squarely on Brinsupri’s early launch and prescription trends. For investors watching Q1 2026 results and upcoming conference appearances, this alignment between analyst commentary and the Brinsupri launch narrative highlights how closely near term sentiment is tied to progress on market access, physician uptake, and continuation rates in everyday practice.

Yet behind the upbeat focus on Brinsupri’s rollout, investors should also be aware of the risk that payer pushback on reimbursement criteria could…

Read the full narrative on Insmed (it’s free!)

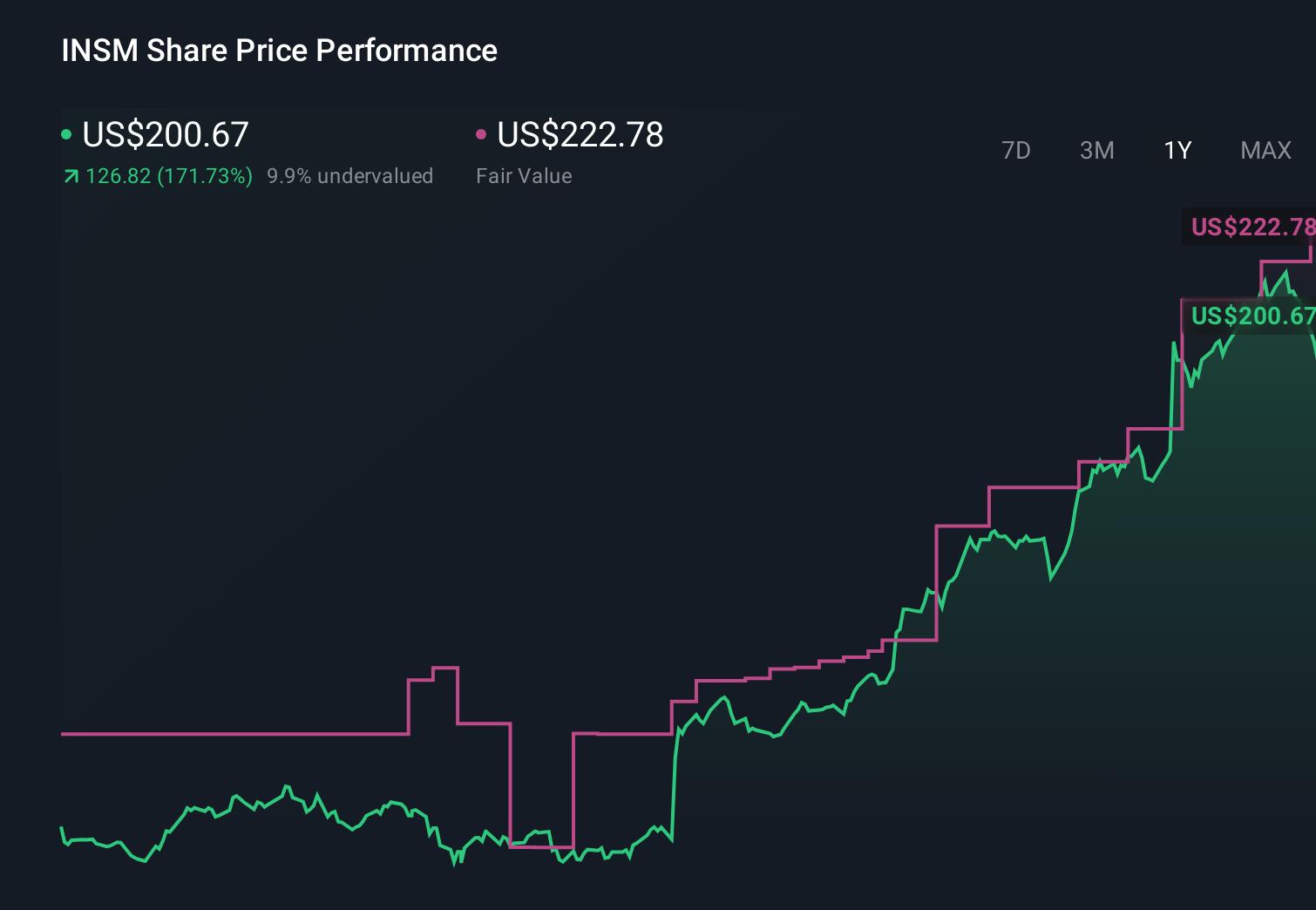

Insmed’s narrative projects $4.0 billion revenue and $979.9 million earnings by 2029.

Uncover how Insmed’s forecasts yield a $212.50 fair value, a 52% upside to its current price.

Exploring Other Perspectives

Four fair value estimates from the Simply Wall St Community span a very wide range, from about US$212 to above US$21,000, showing just how far apart individual views can be. When you set those against the current emphasis on Brinsupri’s launch as the main catalyst and the risk of market access headwinds, it underlines why many readers may want to compare several different viewpoints before forming a view on Insmed’s potential performance.

Explore 4 other fair value estimates on Insmed – why the stock might be a potential multi-bagger!

The Verdict Is Yours

Don’t just follow the ticker – dig into the data and build a conviction that’s truly your own.

Ready To Venture Into Other Investment Styles?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

{kind=link}

{kind=link}

{kind=link}

{kind=link}