Thank you for subscribing to my posts. If you’re not yet a paying subscriber, please consider becoming one. That’ll allow you to DM me with questions and comments. I plan to move my posts behind a paywall in coming months. Subscribing now locks you in at a low rate. Thank you so much for your support and feedback!

France recently used the G7 leaders summit to put “global imbalances” back on the agenda of the world’s leading policy makers. There’s a lot that gets lumped into this term these days, including predatory industrial policy via things like export subsidies and control over critical minerals. But the origin of the global imbalances discussion goes all the way back to the early 2000s, when – following the Asian financial crisis – many countries in the region had an obsessive focus on building their official foreign exchange (FX) reserves, so they’d never again have to go “cap in hand” to the IMF.

In theory, persistent current account surpluses – which is basically when exports exceed imports – shouldn’t exist. That’s because a surplus – via the payment flows it generates – should cause the surplus country’s currency to rise in value, making its exports more expensive, which – over time – should make the current account surplus disappear. That’s not what we observe in reality and this is – at the most basic level – what the debate over global imbalances has been about for the past 20 years.

So how can a current account surplus persist indefinitely? When a country like China runs a surplus, foreign buyers need to get their hands on Yuan to pay for all the goods they’re importing. Ordinarily, this would bid up the value of the Yuan, making China’s exports more expensive, which would weigh on its current account surplus. However, if the central bank prints Yuan to satisfy foreign demand, China’s currency won’t rise in value and the current account surplus will persist. China’s official FX reserves will rise as a side-product of this, because the central bank is using the Yuan it prints to buy up all the foreign currency that’s being offered to pay for Chinese goods.

Over the past decade, China has stopped using its central bank for this, because of a growing outcry that this constituted currency manipulation. But the current account surplus is bigger than ever and the Yuan hasn’t appreciated, so obviously someone in China is still supplying printed Yuan and hoovering up foreign currency. The obvious candidate for this is China’s state banks, who’ve taken over as currency manipulators from the central bank in what I call China’s FX Laundromat. That’s how you end up with a chronically undervalued currency – the Yuan is at least 20 percent undervalued – and current account surpluses that seem to persist indefinitely. Taiwan and South Korea are similar. Both use quasi-government entities to intervene and keep their currencies artificially low.

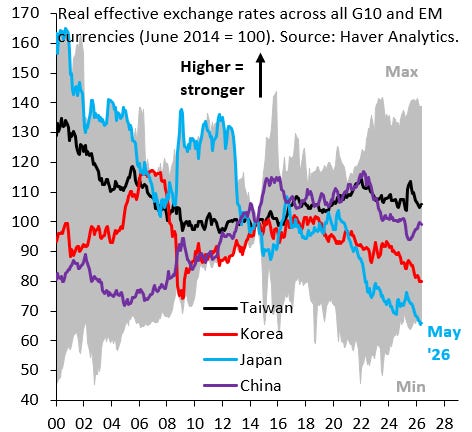

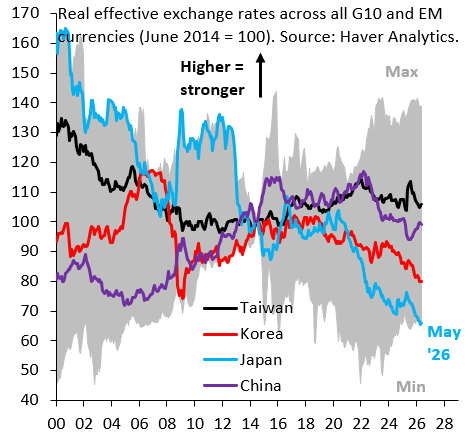

The chart above shows the real effective exchange rates for Taiwan (black), Korea (red), Japan (blue) and China (purple). The nominal exchange rate is what we all see on global FX markets. The real exchange rate layers onto that how price levels evolve in different countries. If a country devalues, for example, that’ll push up inflation, which will push up the domestic price level. That undoes some of the competitiveness gains from devaluation, so the real exchange rate is the most comprehensive way to look at how strong or weak a currency is. The Yen is by far the weakest currency in Asia, but that’s about Japan being a fiscal basket case. As I’ve flagged in many posts, the weak Yen is the inevitable result of the Bank of Japan keeping government bond yields artificially low. It’s China, Korea and Taiwan that are currency manipulators.

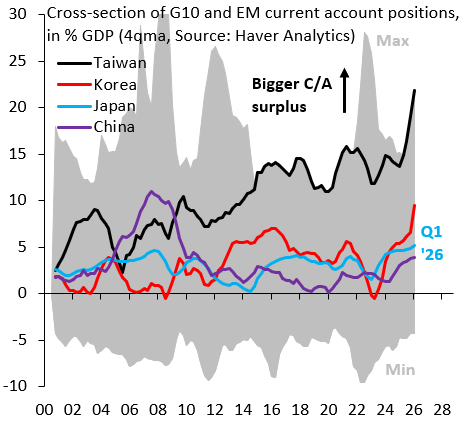

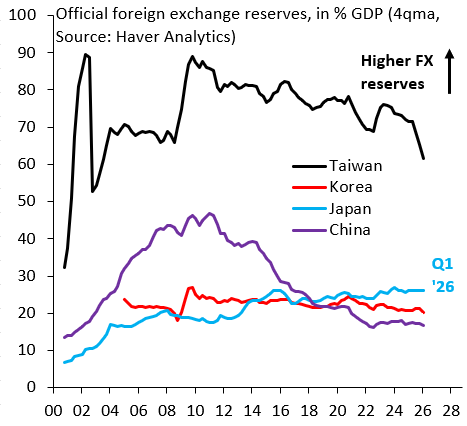

The chart above shows the insanity of what’s going on with these countries’ current accounts. On a four-quarter-rolling-average (4qma) basis, Taiwan’s surplus (black) is above 20 percent, while that of Korea (red) is above ten percent. China is recording its biggest surplus since before the global financial crisis. The chart below shows official FX reserves in percent of GDP. Ordinarily, you’d expect to see FX reserves to be rising sharply because the currencies of these countries aren’t appreciating and the current account surpluses are going through the roof. The fact that this isn’t happening says that – like for China – intervention is being hidden. Korea and Taiwan are operating FX laundromats of their own. I’ll quantify in a future piece exactly how undervalued Korea and Taiwan are, but they’ll be similar to China, i.e. around 20 percent.

{kind=link}

{kind=link}

{kind=link}

{kind=link}