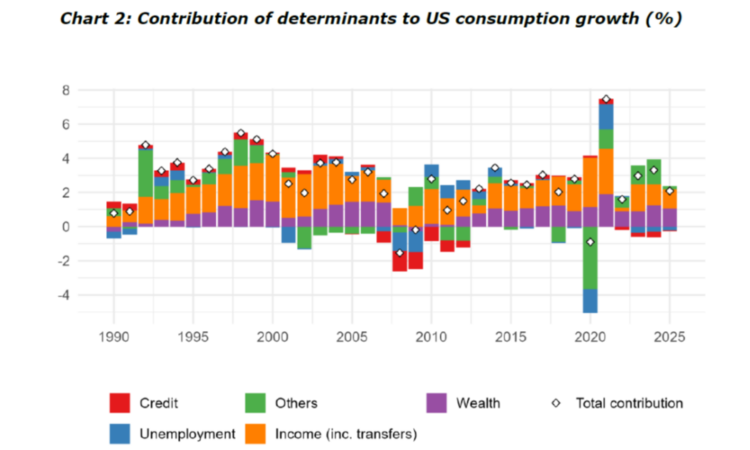

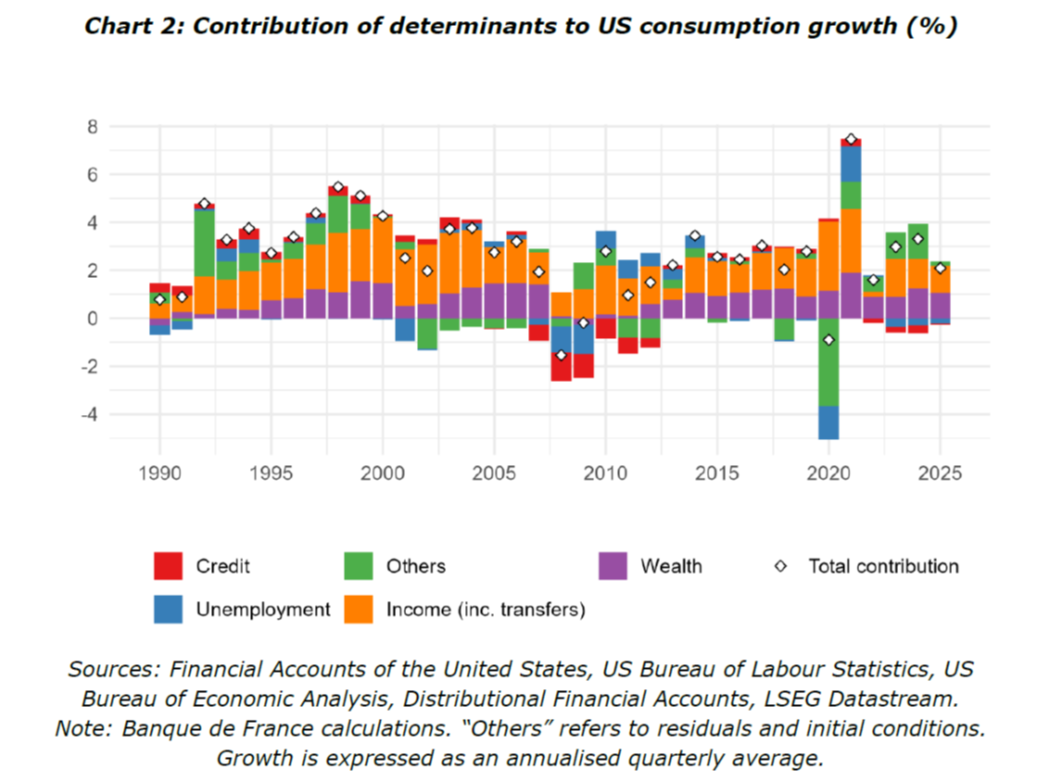

In 2025, about half of observed consumption, according to Bigot and Espic (BdF):

Source: Bigot and Espic (2026).

The estimates rely upon work by Beach, Gamber and Moran (2025) at the Federal Reserve Board, disaggregating by income groups.

Hence, in order to predict consumption, follow wealth — in particular equity wealth.

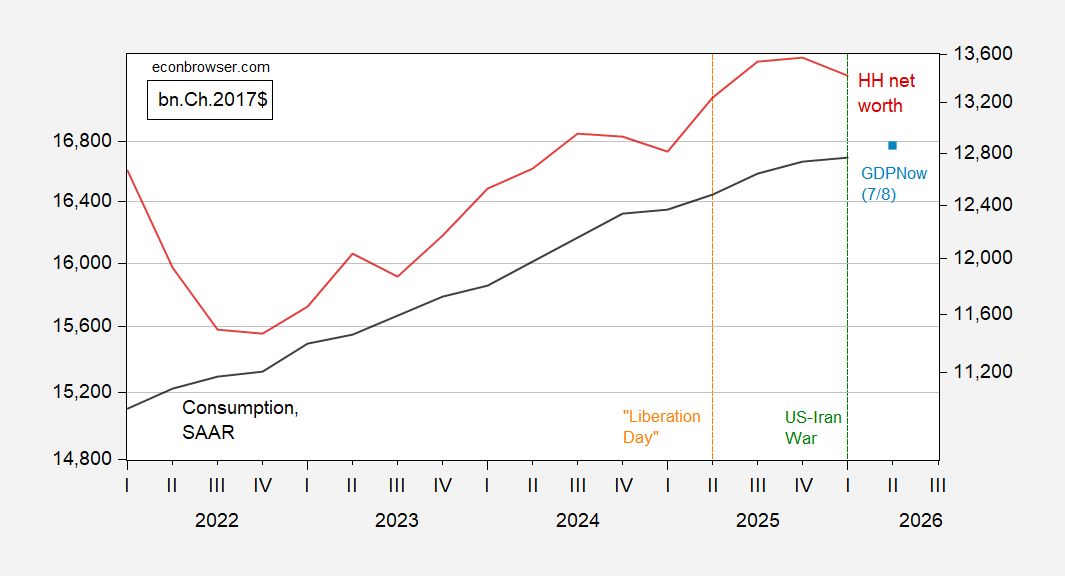

Figure 1: Consumption (bold black, left log scale), GDPNow estimate of 7/8 (light blue square), both in bn.Ch.2017$ SAAR; household net worth in bn.Ch.2017$ (red, right log scale). Both series deflated by PCE deflator. Source: BEA, Atlanta Fed, Federal Reserve Board Flow of Funds, and author’s calculations.

The nowcast indicates 2% q/q AR growth in consumption in Q2; we don’t have net worth in Q2, but based on the rise in the SP500, I’d guess 2.1% growth in net worth. Q1 PCE deflator inflation was around 0.8% , suggesting a 1.3% increase in net worth (q/q not AR).

For now, consumption growth seems intact, albeit slowing.

{kind=link}

{kind=link}

{kind=link}

{kind=link}